A lot of people in this thread are missing the main problem that people have. Yes, cash can be inconvenient, but by eliminating cash entirely you are putting 100% of all wealth into the power of banks. Those without a bank account will be left behind and FORCED to open one.

This gives banks and governments immense control and power over literally all the money you own. Given said power, they will abuse it for their own profit. It's not a question of "IF they abuse it" it is a GUARANTEED. They WILL abuse this power. If you deny this fact, you are living in a fantasy. Give people power, and it will be used, 100% of the time, and not to your benefit.

See, for a recent example in a supposedly free first world country, Canada. Even people who donated to the truckers before the crackdown got targeted in the bank account freezes.

Just like with any bulk data collection and surveillance technology, it is only a question of how soon it will be abused.

Because once you donate money, you have given it away, and it's gone. If you're expecting something in return you are trying to make a purchase, not a donation.

Punishment would involve having something further taken away. If they jailed people for donating, that would be punishment.

> Because once you donate money, you have given it away, and it's gone.

Presumably to the entity you intended to donate to, no? I would argue that determining where your money goes is a right.. If I intercepted all of your future charitable donations for my own purposes you would be understandably upset.

Ha ha, so easy to refute. Is it unethical for the government to stop me from say, donating to a terrorist organisation? It's still "charity", right? ;)

donation are purchases -- you are buying capital for the fund of your choice.

if it turned out a charity you donated to was funneling money somewhere, they would be effectively stealing from you, as the thing you were purchasing was never given.

> On February 17, Deputy Prime Minister Chrystia Freeland said in a press conference that financial institutions have started freezing accounts and canceling credit cards in accordance with the Emergencies Act, which Prime Minister Justin Trudeau invoked earlier this week.

> The powers granted by the act would allow banks to target the accounts of people who have donated to crowdfunding platforms, like the fundraising campaigns on GoFundMe and GiveSendGo, that have fueled the ongoing protests, but Freeland said she would not give "specifics of whose accounts are being frozen."

They can lock anything for any amount and not give any details. Supposedly they have unlocked some, but there's no way of knowing who and why not for others. Typical petrostate behavior.

I'm sure if this happened to people who'd just sent a donation at least one of them would have come forward by now and we'd have some evidence instead of the handwaving "what if" in this article and your comment.

>“Just to be clear, a financial contribution either through a crowdsourced platform or directly, could result in their bank account being frozen?” Lawrence asked.

You're wrong TomSwirly, they did, and unless you're Canadian familiar with the situation (I assume you're not), you should really be more careful about untruths. In your case I assume it comes from a place of ignorance, not malice, but it's tough to be certain.

>Seriously?! How did they justify donating to the truckers as something to be punished? That sounds almost like a police state to me.

So imagine Trudeau's point of view. The Canadian media smeared the protest as nazis, racists, white supremacists, who were going to Ottawa to overthrow the government. Indie and international media clearly disproved this, but Trudeau never saw this. Joel Lightbound, one of Trudeau's top allies saw this.

So imagine you are Trudeau. You believe that a bunch of nazis are looking to overthrow the government. You absolutely declare a national emergency and send the police to arrest them. You also seize the bank accounts of those who are involved in the military occupation of the capital.

The problem? The canadian media was lying quite extensively. This was a legitimate protest of regular canadians who are good people.

CBC is literally state-funded media, and Trudea literally lives in Ottawa. In no world does he have an excuse to be blind, and even in some sliver of hope where he honestly didn't know, why didn't he make a public apology?

I don't think you can excuse this by blaming the media - shouldn't it be the government's responsibility to make sure they have the correct information before making use of emergency powers?

>I don't think you can excuse this by blaming the media - shouldn't it be the government's responsibility to make sure they have the correct information before making use of emergency powers?

I never intended to excuse anything. The media is bought and paid for by the government. This is the state propaganda who called the protest a bunch of nazis.

Worse yet... Joel Lightbound is a liberal quebec MP. He made the huge mistake of going to the protest and talk to them and he was astounded by how misrepresented the protest was by Canadian media. Over a week before the emergency was declared he said exactly what should happen. Stop the inflammatory messaging calling them all nazis, they are not nazis. Give us a roadmap to when our rights will be restored.

That would have solved the entire problem long before anything went down. Today, not only did everything that the protest was protesting still remains without a roadmap, they have added new restrictions to our rights.

absolute FUD and lies. They wanted policy change. Telling your government to use its powers is not revolution. They wanted to "overthrow" the government in the same sense that protestors to legalize gay marriage want to overthrow the government.

You misunderstand the Canadian political system. A senator or MP is free to act according to their own desire; they are political actors elected or appointed expressly for that.

The Governor General is Canada's representative of the Queen. They are not a politician. Literal centuries of British and Canadian jurisprudence have defined the Governor General to have no ability to act without the advice of their Prime Minister. As an unelected representative of the Monarch, if they act without the advice of the Prime Minister, that's a tyrant overthrowing the elected government. England cut off the head of the last monarch to act against the will of the House.

I will openly admit that I have limited knowledgeable of the role of the Governor General in Canadian constitution and legal history.

I still think that characterizing the memorandum of understanding as treason is a misunderstanding of both what a MoU is and the contents of this specific MoU.

First, a MoU is a declaration of intent and a commitment to take an action - Not a legislative bill.

This MoU was addressed to both the Senate and the Governor General.

It doesn't specify how the parties will achieve their their commitment. It is up to the parties to determine if there is a lawful way to meet their commitments before making them.

Senators in Canada have the ability to introduce bills, which can be approved via the traditional pathway.

It also doesn't say anything about removal of the PM.

I fail to see the distinctions drawn. What makes it UN democratic to ask your government to make change through lawful process? It's not like the policies were put in place by public referendum.

How can something be a terrorist plot to overthrow the government, but not treason?

I dont know this website. Article written March 10th well after the fact and just hosts a very clearly one sided view of this. Jody thomas? I dont know wtf this is about.

Let me explain in much better detail about what you're trying to get at.

There was a website named 'canada unity' who put together a MOU in which called on the governor general to inform Trudeau that he has to return our charter rights. In a way you can read it as saying the governor general is overthrowing the government by effectively dissolving Trudeau's government.

This poorly put together was run by JAMES BAUDER and his wife. They were never even for a second one of the protest leaders.

Yet the canadian media portrayed this website as THE protest leaders. Used this MOU as justification of calling on the governor general to overthrow the government's sovereignty. This is how they are claiming the protest was overthrowing the government.

Tamara Lich was the key organizer. Involvement in several previous protests. She represented the protest in negotiations with the mayor of ottawa. She represented the protest in court over the honking situation.

Chris Barber had Jordan Peterson's audience.

Pat King is an actor on the otherhand. His acting played the canadian media's bias against themselves so badly.

What exactly was the crime the protest was committing. Parking violations really.

The only problem that anyone can explain about this peaceful protest is ParKing violations.

Yet here we are, everyone is a nazis, confederates, racists. Pat King offered the canadian media every prejudice, every biased hate thing he could think of. He got into the limelight because they ate up everything he said. He gave them everything they ever wanted on a golden platter.

For multiple elections conservatives have run on the plan to defund these lying canadian media. They got played big time.

Flipside, we're now a month later and pat king is still in jail. Original charge was just 'counseling mischief' but the new charges are 'counseling a felony that wasnt committed."

Absurd vague fake charges to crush a peaceful protest.

We were not discussing whether the protest was peaceful or not; we are discussing whether or not self-evident leaders of the movement wanted a coup.

You can personnally cry and cry that they were not leaders of the movement, but never has Tamara Lich publically denounced James Bauder, or denied her desire to overthrow the government. She never went on record denouncing his involvement in any leadership position. Letting someone in a protest you supposedely organize run around and demand the overthrow of the government is a thing that happens all the time; it's common. Whenever that person has the limelight on them, you vigorously denounce them and deny any sort of leadership on their part. Failure to do so means you agree.

Ultimately, this whole convoy was dangerously inept. That's a thing. You can be so clueless, so reckless that you're a danger to others.

>We were not discussing whether the protest was peaceful or not;

Excellent, you cede that they were peaceful and therefore their charter rights were violated.

>we are discussing whether or not self-evident leaders of the movement wanted a coup.

They didn't. The Media doesnt get to pick who the leaders are neither.

>You can personnally cry and cry that they were not leaders of the movement, but never has Tamara Lich publically denounced James Bauder, or denied her desire to overthrow the government.

I provided CBC who clearly never listed James Bauder as a protest leader. Never did Tamara Lich ever call for overthrow of the government. You want to think the media gets to choose some random protester, say he is leader and then use them?

> She never went on record denouncing his involvement in any leadership position.

She doesnt need to. That's a ridiculous requirement.

>Letting someone in a protest you supposedely organize run around and demand the overthrow of the government is a thing that happens all the time; it's common.

Perfect! In future... the media gets to pick who the leader of all protests are. Not the protest itself. Did you meet John Smith the ecoterrorist who wishes to destroy Canada? Every future protest = illegal now.

>Whenever that person has the limelight on them, you vigorously denounce them and deny any sort of leadership on their part. Failure to do so means you agree.

Great, going forward all left-wing protests will have John Smith the ecoterrorist speaking for them.

>Ultimately, this whole convoy was dangerously inept. That's a thing. You can be so clueless, so reckless that you're a danger to others.

How dare they so recklessly exercise their right to protest!

Your whole house of cards rest on the idea that I have to agree that James Bauder was never a leader of the movement. When James Bauder said he was a leader of the movement. When many news outlet identified him as a leader of the movement. When many protesters identified him as a leader of the movement. And Tamara Lich never denounced him or any of his formal requests to the Governor General.

Reality doesn't care about your feelings about James Bauder.

>Your whole house of cards rest on the idea that I have to agree that James Bauder was never a leader of the movement.

Does it matter if you agree or disagree with this? I provided a cbc link that listed the leaders. Bauder was not among them. Why do you think the CBC didn't even list bauder?

In fact, im just doing a search right now... there's no articles on cbc at all listing bauder as anything at all. Which is in fact impossible because I recall reading about bauder, the mou, and how they plan to overthrow the government on the cbc amongst others. It would seem the CBC quietly deleted those articles.

>When James Bauder said he was a leader of the movement.

Did you know I am the leader of BLM?

>hen many news outlet identified him as a leader of the movement. When many protesters identified him as a leader of the movement. And Tamara Lich never denounced him or any of his formal requests to the Governor General.

Why indeed has BLM never denounced me, John Smith the ecoterrorist. Is it by chance Bauder and I were just never a leader. That media smears were ignored by the real leadership?

Politically unaligned media don't get to pick the leaders of a protest.

>Reality doesn't care about your feelings about James Bauder.

I know why you cling to Bauder so much when clearly he's not a real entity. Without this tremendously weak point... you literally have nothing else to say the protest were 'overthrowing the government'. Without this tenuous at best point, how do you ever justify a national emergency.

Ultimately it doesnt even matter. They were parked outfront parliament for weeks and never quite got around to insurrection. The entire narrative that they were trying to overthrow the government is without merit. Reality is on my side.

Financing terrorists - and these "truckers" were nothing else, which led to the declaration of the emergency state, a legally defined mechanism! - will lead to issues no matter if it's al-quaeda or y'all-quaeda.

The donors should be happy all they got was a temporary freeze on their bank accounts. Had it been Islamist terror they had donated to, the accounts would have been terminated and criminal charges levied.

I am curious if you generally feel comfortable with the government being able to retroactively define something as "terrorism" when it does not conform with your general political views. Personally I think this is a terrible idea whether or not I agree with the people being targeted.

>I am curious if you generally feel comfortable with the government being able to retroactively define something as "terrorism" when it does not conform with your general political views. Personally I think this is a terrible idea whether or not I agree with the people being targeted.

There's a hilarious video from our parliament.

Andrew Scheer(former conservative leader, former opposition leader) was talking.

Elizabeth May(former green party leader) got up and started accusing him of 'dogwhistles to nazis' blah blah.

Andrew Scheer stands up with the biggest smile.

He points out Elizabeth May has been arrested and convicted of an illegal blockade while being green party leader. That the precedent set will mean that the green party donaters will have their bank accounts seized as well as her own.

The irony, it's only matter of time that conservatives take government back and very well can do this now.

On twitter a ton of greenpeace and antifa people freaked out at this new precedent.

"What if I donate to greenpeace. Some point later they have a protest that goes sideways. My bank account gets seized?"

It sounds the argument being made here is that this was a dangerous precedent being made that can be abused by political parties against their political opponents. This seems to be presented by you with apparent glee as a conservative vs green party/greenpeace/"antifa" or liberal issue. What you'll actually find is that broader society is just intolerant of the economic duress and disruptions caused by such protests.

Up to a quarter of Canadian-US trade was going through that area, and real people were suffering due to the trucker blockade. These economic disruptions had secondary effects that impact the lingering impacts of the pandemic and exacerbated supply chain issues.

There is not a whit of moral equivalency between climate change protests and some truckers afraid of a needle.

>It sounds the argument being made here is that this was a dangerous precedent being made that can be abused by political parties against their political opponents.

Because it was the current government abusing the act to use against their political opponents. Do you agree or disagee with this?

>This seems to be presented by you with apparent glee as a conservative vs green party/greenpeace/"antifa" or liberal issue.

If Canada is a free country and we do have fair and free elections. Inevitably the conservatives form government again. Andrew Scheer almost was prime minister.

I guess the glee comes from the above question. If you disagree and that the current government did not abuse the act to crush a peaceful protest. I will immediately agree with you and accept the precedent that this future conservative government gets to crush all dissenting political protests.

The glee you detect isn't glee. I very much disagree with this precedent. The government should NEVER be able to stop a peaceful protest. The glee is how absolutely tyrannical Trudeau acted.

>What you'll actually find is that broader society is just intolerant of the economic duress and disruptions caused by such protests.

Well first of all, this 'broader society' needs citation. The only people who suggest the majority of canadians agree with the use of the emergency act are the same media who called the protests a bunch of nazis. I dont accept state propaganda as facts sorry.

Also what economic duress and disruption? By the government's own admission in their required justification of the emergency act there was no blockades. The emergency act was used entirely and solely as part of the Ottawa protest. Blocking a few blocks in front of parliament. There is no economic duress here at all.

>Up to a quarter of Canadian-US trade was going through that area, and real people were suffering due to the trucker blockade. These economic disruptions had secondary effects that impact the lingering impacts of the pandemic and exacerbated supply chain issues.

1/4 of usa trade goes through downtown ottawa for no damned reason? Can you prove that in any way please?

Or do you mean the detroit bridge blockade? Not only was there 1 lane open, the detroit tunnel was completely unblockaded. Sarnia's bluewater bridge was not blockaded. Niagara falls, not blockaded. And cherry on top... the ambassador bridge dissolved BEFORE they even mentioned talking about the emergency act.

No, I dont expect you are trying to use a non-existent blockade as justification for national emergency. The only place the emergency act was used was in ottawa. Surely you are arguing 1/4 of usa trades has to drive in front of parliament?

>There is not a whit of moral equivalency between climate change protests and some truckers afraid of a needle.

If you say so. I do believe I get to decide upon my own moral decisions.

Here's really what's happened. Trudeau was misinformed greatly by the canadian media. He crushed the legitimate protest because he misunderstood why the canadian media called for the denazification of the protest. Trudeau absolutely acted tyrannically and has not fixed the situation.

The precedent is set, conservatives do NOT have the right to protest right now. All of the original reasons for the original protest still stand AND they've added new vaccine mandates making the reason for protesting to increase.

Without the right to peaceful protest.. it means other protest will now be required.

If conservatives want to lead an armed insurrection in Canada over "vaccine mandates" (reactionaries are so good at controlling the discourse with the words they force) they should go for it. Something tells me the consequence will be larger than not being able to swipe your plastic at the gas station.

Funny it took white people getting their bank accounts frozen for there to be noise that the government has too much power and wields it against citizens with impunity. Wonder how Trudeau's government treats the First Nations? Oh that's right, running oil pipelines through their land.

Only a certain demographic has had freedom of protest in Canada. Have you ever been water cannoned for defending your home and the groundwater of your community? But sure, conservatives are the new precedent about not being able to protest. No demographic has been harmed in Canada as deeply or egregiously as the conservatives who live underground now and trade in scrip

>If conservatives want to lead an armed insurrection in Canada over "vaccine mandates" (reactionaries are so good at controlling the discourse with the words they force) they should go for it. Something tells me the consequence will be larger than not being able to swipe your plastic at the gas station.

If you analyze protests lately like the 'mostly peaceful' burning riots of BLM etc. Which as a quick aside, BLM is fully justified in their protest.Police brutality and clear systemic racism is objectively true.

Compare that to the over the top peaceful protest in Ottawa. Which was intentionally that way. The protest policed itself to not give the media this. The media has been smearing conservatives for so long.

But more importantly, and clearly you went right to armed insurrection. Who said this was an insurrection. Notice also how January 6 went from insurrection to less than a riot. It's not even a riot, it's just an 'attack' now. Trudeau urgently wanted it to turn into an insurrection... the false allegation and propaganda was that the protest was looking to overthrow the government. Which isn't true at all. They sat outside in -20c on the road and NEVER insurrected or even tried to overthrow anything.

This just goes to prove how wrong all of this still is. Conservatives still do not have the right to protest.

>Funny it took white people getting their bank accounts frozen for there to be noise that the government has too much power and wields it against citizens with impunity. Wonder how Trudeau's government treats the First Nations? Oh that's right, running oil pipelines through their land.

>Only a certain demographic has had freedom of protest in Canada.

Why do you think Trudeau hates racial minorities so much? Vaccine mandates disproportionately harm racial minorities especially black and indigenous canadians.

>Have you ever been water cannoned for defending your home and the groundwater of your community? But sure, conservatives are the new precedent about not being able to protest. No demographic has been harmed in Canada as deeply or egregiously as the conservatives who live underground now and trade in scrip

It almost reads like you read conservative = white people. How very incorrect.

> “I would be remiss if I didn’t start by recognising the news coming from India about the protest by farmers. The situation is concerning. We are all very worried about family and friends. We know that’s a reality for many of you. Let me remind you, Canada will always be there to defend the rights of peaceful protesters. We believe in the process of dialogue. We’ve reached out through multiple means to the Indian authorities to highlight our concerns. This is a moment for all of us to pull together,” Trudeau had said in November 2021.

Those were in fact not peaceful

> 1 journalist killed. One person lynched for alleged desecration. Over 1,500 telecom tower sites damaged by protestors (as of 28 Dec). Government buses and 30 police vehicles damaged on Republic Day.

Race plays a role in vaccination. Black and Indigenous Canadians are only around 50% vaccinated. Indian/Punjabis are somewhere around 70%. An awful lot of truckers are Indian. Especially from Quebec.

One of the original key issues that sparked this protest is the action by Trudeau to ban unvaccinated truckers and put them out of a job. This disproportionately harmed racial minorities including Indians.

The comparison or hypocrisy is that he supported the indian farmers but called the punjabi truckers a bunch of racists. It blows my mind.

Canadian truckers were > 90% vaccinated at the time of the "Trucker" Tantrum. There were very few Southeast Asians in evidence among the tantrum throwers.

They were majority white (mostly because the Southeast Asian truckers in Canada are mostly vaccinated and were quite busy because the people throwing the tantrum weren’t actually working because they refused to get vaccinated).

This is whataboutery. At the very least the truckers were an extremely unpleasant and potentially dangerous nuisance for everyone in the vicinity.

At worst were literally attempting regime change. They were also largely funded by the US far right, which has obvious links to Russia. In fact Russian propoganda was encouraging similar actions in the US and the EU.

So of course they were defunded.

It's always amusing to see libertarians complaining that a government shoots first - financially in this case, and only after a long delay - and asks questions later, when they're typically the people claiming loudly that far more extreme forms of violence are always legitimate in personal self-defence.

Just as with Jan 6, most of these people should have been jailed and those from the US should have been banned from entering Canada again.

Never mind the political angle, the nuisance and intimidation were more than enough to justify that.

I agree that the truckers were super disruptive. I’m glad some punitive action was taken.

But freezing the bank accounts of people who donated to them without due process is beyond the pail. Given that cash is mostly dead as a result of covid, banking needs to be considered a basic right. It shouldn’t be able to be revoked simply because the government doesn’t like what you do with your money.

Claim made not in evidence. Legally frozen were the recipient accounts. Yes, contributors could have had their accounts frozen, but no evidence that the government ordered such an action on any donor.

You sound severely self-centric and antisocial. Protests are a movement, and the noise they make are the extended arm that you are to grab and hop onto.

>It's always amusing to see libertarians complaining that a government shoots first - financially in this case, and only after a long delay - and asks questions later, when they're typically the people claiming loudly that far more extreme forms of violence are always legitimate in personal self-defence.

do you regularly see libertarians advocating for shooting the friends & family of an attacker, in your own words, "after a long delay"? this is a very poor comparison.

> Even people who donated to the truckers before the crackdown got targeted in the bank account freezes.

[citation needed]

The Emergencies Act,[1] explicitly written to be compatible with the Charter, does not allow for retroactive actions [2]. There was a lot of initial confusion, and so whatever story you may have heard (and is stuck in your head), you may wish to go back and double-check to see if there were any corrections.

I see you are a throwaway account and unlikely to respond.

One cannot deny that the emergency act was used this way. The RCMP confirmed(https://blockade.rcmp.ca/news-nouvelles/ncr-rcn211130-s-d-en...) that this happened and denied being the ones who did it. Implying either the government went around them OR the banks took this action upon themselves with gigantic liability issues.

>The Emergencies Act,[1] explicitly written to be compatible with the Charter, does not allow for retroactive actions [2].

That's a very good point, but incorrect. The emergency act is EXPECTED to trample on charter rights. In an actual emergency it's entirely expected that police will go over the line.

What exactly was the emergency act used for? Not a single blockade existed. It was used entirely for the protest in Ottawa. Their goal is to remove the illegally parked semi trucks.

If this was used in such a way that charter rights were not trampled on. The police would have gone in, towed the trucks and left the protesters who were lawfully protesting.

That's not at all what happened. They came in and removed the entire lawful protest, not just some illegally parked trucks. The emergency act was used to crush a legitimate protest.

So what happens next? Section 46 of the emergency act is next. The people damaged by the protest, be it having gotten pepper sprayed or your right to protest being removed. You get compensation. The crown is about to pay huge $ to these protesters.

> I see you are a throwaway account and unlikely to respond.

Created on January 1 (01/01), 2017. It's kind of become less throwaway over time. :)

Also: your username is in green, which means (IIRC) it is less than two weeks old. One of us has a higher probability of being a throwaway.

> One cannot deny that the emergency act was used this way.

Your link says nothing to confirm that it was an ex post facto action.

> That's a very good point, but incorrect. The emergency act is EXPECTED to trample on charter rights. In an actual emergency it's entirely expected that police will go over the line.

The Emergencies Act itself says it is subject to the Charter:

> AND WHEREAS the Governor in Council, in taking such special temporary measures, would be subject to the Canadian Charter of Rights and Freedoms and the Canadian Bill of Rights and must have regard to the International Covenant on Civil and Political Rights, particularly with respect to those fundamental rights that are not to be limited or abridged even in a national emergency;

> That's not at all what happened. They came in and removed the entire lawful protest, not just some illegally parked trucks. The emergency act was used to crush a legitimate protest.

It was not a blockade or protest that got removed: once they started living there it became an occupation.

Further, threats of use of violence are not part of legal protests:

> (a) the continuing blockades by both persons and motor vehicles that is occurring at various locations throughout Canada and the continuing threats to oppose measures to remove the blockades, including by force, which blockades are being carried on in conjunction with activities that are directed toward or in support of the threat or use of acts of serious violence against persons or property, including critical infrastructure, for the purpose of achieving a political or ideological objective within Canada,

To safely remove the trucks from the street, nobody needs to be around the workers doing the towing. It's basic health and safety. Police repeatedly asked people to leave. Many refused, many complied. Would you have prefered the police run over the protesters with their own trucks?

Police have an additional power to asking politely. They can arrest people. It is the appropriate response if someone continues to break a law but is non-violent.

Why should anyone be denied access to banking? In our modern world, banking is about as essential as food. Would you deny someone food because of their political beliefs?

I might personally deny them food, but I do not think the government should have the power to stop another consenting person to give or sell food to some based on their political belief.

The charter also allows itself to be overridden so that's a bit disingenuous. If the charter says that you can ignore it in a lot of cases if needed, then it's very easy for any law to be compatible with it

Not knowing anything about the Vision Times, a quick search:

> Vision Times is one of the news organizations that Falun Gong's founder Li Hongzhi refers to as "our media".[1] The newspaper's president is the spokesperson for the Falun Dafa Association in New York, and is chair of another Falun Gong group called Quit the CCP.[1] In 2021, The Atlantic called Vision Times a "doppelgänger site" of The Epoch Times.[5]

I saw this reported here in the UK. I believe it was also mentioned in a recent Unherd article about the dangerous implications of this misuse of powers, but I’m sure you are capable of using a search engine.

I was asking because American right wing news has frequently lied about what was happening here in Canada. To my knowledge there hasn’t been a single report of a frozen bank account over a donation except for some debunked tweet by a Canadian conservative politician.

The canadian government declared an emergency under the emergencies act. The act enables the government to make any orders or regulations, so there is no need to go through the court.

If you're claiming that a government is abusing its power because it froze some funds, and it turns out it was done according to law, then the accusation is unsubstantiated. Maybe it was abusing its power, but we haven't been shown any evidence. And the burden of proof is on you to show that it was an abuse of power.

The government used emergency powers designed to be used in case of war for dealing with peaceful protesters. The previous act was only used during WW1, WW2, and during the October Crisis by Trudeau's alleged father, which is also the reason the powers were watered down.

> Freeland said she would not give "specifics of whose accounts are being frozen."

Freeland did say that they would be freezing the donators as well in the original videos.

The more egregious comment was by David Lamenti. He's a lawyer and law professor. He knows the law. His comments are not a gaffe and not out of context or anything. This is not him pulling the wrong insult out of his bag. He spoke clearly and he meant every little bit of the comment.

That is a pretty high bar for abuse you have there. Emergency acts are typically meant for governments to react quickly to unprecedented situations where not all eventualities can be forseen and covered by laws. This means that they are grant very broad powers that considered unacceptable under normal conditions and thus any use of those powers is potential abuse. What is abuse and what dis not allowed are two entirely different things.

>If you're claiming that a government is abusing its power because it froze some funds, and it turns out it was done according to law, then the accusation is unsubstantiated. Maybe it was abusing its power, but we haven't been shown any evidence. And the burden of proof is on you to show that it was an abuse of power.

This is kind of the argument that Gerald Butts made. That technically parliament approved this misuse of power. In a way you are right. Here's the problem.

The Canadian media represented the protest as a bunch of nazis and maga military occupying ottawa and loooking to over throw the government.

The NYTimes thought it was the best story ever. They put boots on the ground and said... wait we don't really agree with the goal of the protest but it's a legitimate protest. That using force to end the protest would be wrong. That in a democracy protests are going to be annoying but these must be left to exist.

They are right. There can never be an exception to the charter right of peaceful protest. Right now, what the conservatives in Canada have been told is that they do not have the right to protest. They will simply declare another national emergency, seize bank accounts, and arrest them on 'mischief' charges.

So now what happens? The conservatives cant peacefully protest... media is smearing them to propaganda levels.

You can still do roaming protests where you keep moving making stopping the protest difficult to do. I suspect these kinds of protests will get tiresome.

Eventually you just say, ok, peaceful isn't allowed. Other than peaceful is our new option.

Yes, it's perfectly legal and done according to law.

There are some oversights. Under the Emergencies Act, the Parliament and the Senate get to confirm the use of the act. What surprised people were the fact that the action of voting down the use of the act will trigger an election, and parties didn't want an election. [1]

>Are you sure this is abuse? My guess is a judge ordered the accounts to be frozen.

That's kind of the problem. No judge was ever involved. The emergency act was deployed by Trudeau, they seized bank accounts and arrested legitimate peaceful protesters. Tyrannically crushing a legitimate protest just because ~70 semi trucks were illegally parked in ottawa.

Shutting down a protest because it completely shut down a major city center and harassed locals for weeks seems like a totally legitimate use of government power to me. They also blocked a major bridge border crossing and attempted to block other border crossings. That makes them less of a protest and more a rebellion. I can’t think of a single country in the world which would allow an absolutely tiny minority to shut down border crossings for extended periods of time. Preventing trade to that extent is arguably a form of violence; using horns in residential areas late at night is definitely violent.

Also “crushing” a protest usually involves lots more violence then was employed. Tiananmen Square was crushed (literally), US civil rights protests were crushed with firehouses and dogs, etc. The actions of the Canadian government seem anodyne to any government I’ve heard described as “crushing” a protest.

>Shutting down a protest because it completely shut down a major city center

It did not do this at all. When I zoom in on Ottawa and ignore gatineau. I would assert the city center is say UofOttwa to the east side, if not all the way to the rideau. Maybe kowloon market, china town, little italy, centretown west is the west side. With a southern spot of maybe the 417 highway?

What did the protest block? You'll have to zoom it significant more. It blocked what wellington and queen for 2 blocks? It did absolutely nothing to 90% of the city centre.

To suggest a protest at parliament hill is 'completely shutting down the major city center' is absurd.

> harassed locals for weeks seems like a totally legitimate use of government power to me.

Ok, fine, so we set the precedent that you agree with. You're fine with future governments crushing legitimate protests under the same misrepresentations as well? Afterall, how much conservative protests are there? Pretty rare. We're going to be crushing left-wing protest for the most part.

>They also blocked a major bridge border crossing and attempted to block other border crossings.

Did they? Which bridge in Ottawa did they block? Or do you mean ambassador bridge which is a related but unconnected protest. This blockade ended before the emergency act was ever implemented. We are talking about Trudeau crushing a legitimate protest in ottawa. The emergency act was used for ONLY ottawa, took them days to even do anything.

>That makes them less of a protest and more a rebellion.

A rebellion! Oh wow. A peaceful protest in front of parliament with bouncy castles and hottub is a rebellion. I guess they just never quite got around to the rebelling part...

I honestly didnt even see the canadian media label them a rebellion. Sure even doug ford called them a military occupation. But rebellion!

>I can’t think of a single country in the world which would allow an absolutely tiny minority to shut down border crossings for extended periods of time.

People linked Trudeau being in favour of the extremely violent hong kong riots and the only marginally violent farmer protests in india. Yet he refused to even talk to them once. Couldnt even send a staffer to go talk to the protest once.

I would hope ANY government would be forced to talk to a protest at least once before declaring national emergency and crushing them with force.

>Preventing trade to that extent is arguably a form of violence; using horns in residential areas late at night is definitely violent.

Oh wow, we are even redefining what violence is. Why are you doing this? There's a clear reason. The protesters have the right to 'peaceful protest'. You are required to redefine 'violence' in order to invalidate their charter rights. I see what you are doing.

You are even redefining what a residential area is. For the record... you have to go about 4 blocks or more away from the protest to get to the first residential building. Where they were parked is not residential at all. Census data is public. The protest was never 'harassing residents'. At most they were 'harassing counter protesters' which is what it is.

>Also “crushing” a protest usually involves lots more violence then was employed.

Now you're redefining crushing?

>The actions of the Canadian government seem anodyne to any government I’ve heard described as “crushing” a protest.

Crushing means 'to subdue completely' or 'oppress grievously'. Well the day before they gave the emergency act back. There was not a single protester in ottawa and parliament hill. They subdued the protest completely. AKA they crushed a peaceful protest.

There's a reason why Bill Maher called Trudeau Hitler right before he crushed a peaceful protest. After he tyrannically crushed the protest and made protesting illegal for conservatives. Bill Maher seems to be saying that Trudeau = Hitler.

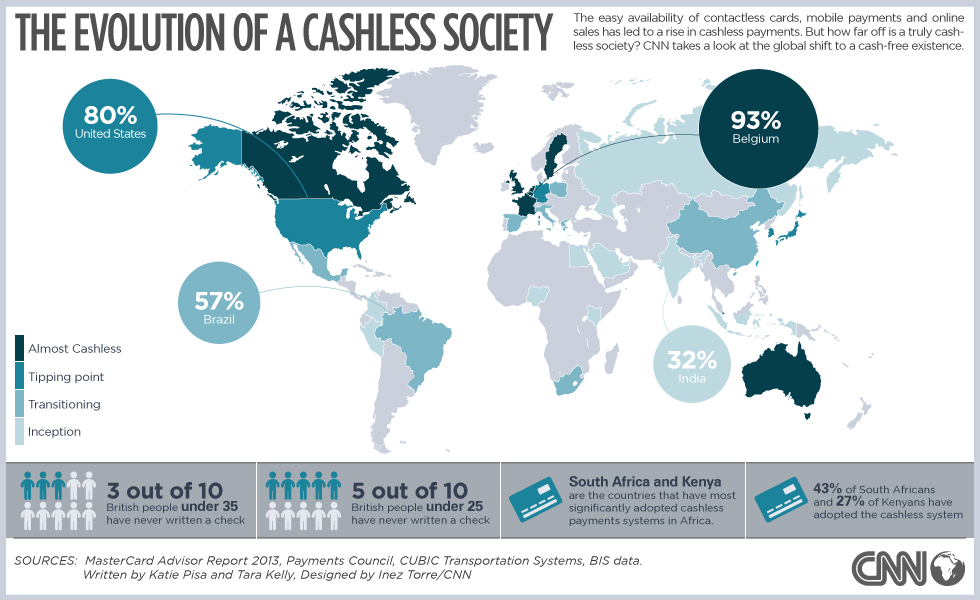

Here in India government has come up with a few policies that helps a lot in this regard. Firstly we have UPI that allows for instant bank account to bank account transfers. Most banks give 20-30 free UPI transactions per month. In addition, government came up with a rule to have 0 transaction fees on low value transactions on cards. In addition to this, government has also been promoting a alternative to visa/mastercard with the rupay network. I think more countries need to look into these.

Here in India cash use is still very popular and mostly used for tax avoidance and to avoid surveillance by the government agencies.

The UK (when part of the EU) limited the fees Visa and MasterCard can charge — 0.2% of the transaction for debit cards and 0.3% for credit cards.

Electronic transfers (made by website, telephone, app, in the branch etc) between bank accounts are also free for consumers, although I don't think there's any rule requiring this.

According to the article, that isn't the main problem that people have:

"Overall, 23 million people said that using cash made them feel more in control of their finances. Two-thirds were concerned about fraud when making payments and 57pc were concerned about privacy."

The rest of the article, if I'm reading it right, makes it clear that "in control" is meant in the sense of "to be on top of it", rather than a distrust of banks or the government.

Here in the Netherlands, the government has been pushing back against cashless for more or less this reason - that it grinds the poor who are most likely to be unbanked.

One of their papers on the subject basically accepted that a lot of the poorest Dutch residents are using cash in the underground economy, and advised that tampering with it would cause a lot of hardship.

It is clearly a problem, although, I am afraid, you've been forced to have a bank account in most western countries for a while now. Removing cash is part of that process but it's not the beginning. That boat a sail a while ago.

What we need is more competition in the banking sectors. And I am not talking about more private for-profits banks. We need:

1. Public own banks. A bank as a public service. Indeed, governments will have more control on it but if you are a citizen of another country, this becomes less of a problem. You could be depositing your money into the Public Bank of Canada for example. A bank as a public service might have nefarious interests too but at least they would be different from a private for-profit bank.

2. We need private non profit banks. Banks run as an NGO. And on this, we could help by providing open source banking software. Rigorously tested and hardened.

>you've been forced to have a bank account in most western countries for a while now.

You have, many haven't. There's plenty of people who pay their rent in cash and work in a business that pays them in cash (strippers, some farm laborers, etc). Surviving in the US with cash only would take away a lot of options for many people but at the same time, it's completely possible.

IMO we need more ways to bypass banks, including the central bank, not more of them.

3. Most of all, we need banks owned by their customers, i.e. banks in whose interest it is not to build huge bureaucracies to skim off maximum rent from transactions, but just enough to keep the business running.

Exactly. I'd like to take this to its logical extreme, and have me be 100% owner of my own bank. I will hold notes printed by the treasury and open something in my pocket to withdraw from my account when it is time to pay.

The risk of being the sole owner of your bank is fairly obvious, though. I'd want multiple owners for central limit theorem reasons. How would you work around extreme variability in demands if you are the sole owner?

Also, how would you earn interest on your money if not by lending it out to others, who would then also be customers of your bank and hence owners?

It sounds to me like what you describe is either

(a) not really a bank in the sense that we mean when we talk about banks, or

(b) not a logical extension of collective ownership but rather that you want a traditional capitalist bank except where you are the owner instead of someone else.

>(b) not a logical extension of collective ownership but rather that you want a traditional capitalist bank except where you are the owner instead of someone else.

Collectivism taken to the most localized extreme is individualism. This is a collective of one.

>(a) not really a bank in the sense that we mean when we talk about banks, or

You can ask these questions about any bank; the mere fact this bank is owned by the sole depositor doesn't change what a bank is.

>I'd want multiple owners for central limit theorem reasons. How would you work around extreme variability in demands if you are the sole owner?

The sole depositor is also the sole owner. It's a collective ownership of depositing customers, not those who owe the bank money.

But in the end I'm just exemplifying what the logic extreme of your suggestion ends in, which actually happens to be a system I approve of. You keep treasury notes in your wallet, lend them if you like, and pull them out whenever you'd like to 'withdraw' them from your demand account. There's no fancy rubber stamp or business license to back it up, but it meets the definition of a bank (which is roughly an institution that accepts demand deposits and possibly loans them out).

I see. I think our difference is that I consider the people who (possibly) loan money also customers of the bank, hence owners, if the bank is collectively owned.

I think of loans as a critical part of the bank business because otherwise it's just a glorified safe.

Banks already massively abuse this power, and in any case the UK and US have laws that allow seizure of cash and other assets in criminal cases.

So do private corporations like Ebay, which have a history of closing private accounts for random reasons.

But for context, this is a scare story without any real substance in the UK's premier far-right paper for rich kooks. The Telegraph is notorious as a non-reputable source, and I would be very surprised if there any serious moves to ban cash in the UK - or the US - any time soon.

As mentionned in the article, some people use cash because they struggle with budgetting. They may get a specified amount of money from the ATM each week in their wallet and get an immediate visual clue of where they at in any moment. Using cash actually make you see the money going out. It is much more tangible than just numbers to a lot of us.

We could probably think of other options, like having rechargeable money card with some kind of visual bar indicator showing the amount of money left but that is not there yet.

Also as much as I like using my cards and phones for payments, they are really bad for privacy. All you payments get stored in a database waiting to be dumped, stolen and leaked. And it is not a matter of if but rather of when.

No, you don't have a lot of choice. UK banks have many restrictions about who can open an account. Just by queuing in a branch I've seen immigrants being rejected because they don't have a job yet.

If you still think about banks re-loaning bank deposits you're living in another century. Fractional reserve banking hasn't been a thing since (at least) the 1960s.

Depositing money isn't giving money to a bank. It's exchanging money for highly liquid debt and receiving interest in return. Giving money to a bank is a relationship where the bank pays you.

Also, the government already forces you to have auto insurance. This doesn't really seem any better or worse.

Merely having a bank account can in some instance trigger FATCA report, depending on where you open it. This opens up further intrusions to your privacy. I do not know if any foreign nations have an analogue of this.

It can also be difficult to open without an address or with certain history, even if you are a citizen or legal resident.

Bank accounts for homeless people can be done, in Britain probably after 'encouragement' from the government (do this your way or we'll force you to do it our way...).

That is true. But has issues with diverging interests. The interests of government bureaucrats who see like a state are not at all necessarily in line with my own.

I think it's in their interest since they're using crypto as an "investment" rather than a means to exchange goods and services. Moreover, it's probably hard to envision as an issue as long as it works to their advantage and concentrated amongst a few in a form of digital currency.

Then again, I rarely hear anyone discuss the benefits of inflation (I didn't say hyperinflation).

"This damn inflation is making my mortgage payments significantly less than my payments from 10 year ago!" said Nobody

I'm far from an economist myself... but there is relevant debt beyond individuals' debt. There is national, foreign, state and city, etc... an argument could be made that some of this debt is even exported abroad.

Inflation, might not make goods and services cheaper, but it can have an effect that can be used to one's advantage.

I've already mentioned mortgages, but it might be the same with many other loans and services. Assuming interest rates are low enough (if not zero), then deferring the whole payment means that you retain money to work for you, as well as take advantage of the effects of inflation on the overall financed amount as long as the period is long enough.

Locking in service rates (grandfathered) can work to your advantage as well, depending on the service agreements of course.

I'd say there are a lot of people with bad debt, but often times that comes as a result of hardship, or just bad financial decisions and life choices.

Those that have no debt are probably not going through financial hardships, but should probably start accruing manageable debt to avail from the effects of inflation, retain more money so that it can work for them, and build credit history to become more debt-worthy.

Saving money is just losing money due to inflation and lost potential. It's a difficult one bc we all know we should keep a certain amount of money just in case, and putting it somewhere where it's working for you but still liquid if needed is quite difficult. If times get hard and you need to liquidate your investments, chances are that you will be losing a lot bc when times are hard, investments are down.

Saving money is really quit discourage, and there are some pretty compelling reasons why this is a good thing. Money that is saved is usually money that is out of circulation. As a result, it's not doing any "work" and fewer goods and services are purchased and economies slow as a result.

While I do not foresee this being adopted in the US I won't put it past lobbyists to try. Maybe they are already trying? I personally would never go for this. Cash in my pocket can't be "disabled" individually. In fact I am seeing a transition to targeted risks in many places. Amazon destroying small local stores facilitating the ability to disable someone's purchasing capabilities or limiting what one person may buy. As a side note, porch pirates are becoming a real nuisance for local authorities. Network connected cars can be remotely tracked, disabled or bricked. Smart homes that can monitor an individual. Smart phones tracking individuals.

I don't think I could fully embrace the Amish way of life but I suspect my local community mostly farmers and ranchers could implement a barter system if we had to. Some of this already exists. We could be self sufficient for things like food, basic repairs, transportation via horses. I am personally not opposed to giving up some luxuries like internet and online shopping if it came to that. I realize some people born into these things perceive them as absolutely mandatory but I did just fine without them for a big part of my life. In the last several months I have not needed to travel more than 16 miles from home. I suppose I could stock up on e-bike parts and solar panels then fall back to horses. Come to think of it, we could build a local warehouse business that stocks up on things not made locally then sell them locally using cash or maybe even implementing a Craigslist-Style barter system over Lo-Rad.

Am I alone on HN in thinking this way? I know I am not alone in my local community, but I am curious how many on HN have thought about this.

>While I do not foresee this being adopted in the US I won't put it past lobbyists to try.

it will. and it would only take a few years of concentrated brainwash from the telescreens for the people who will oppose that to be branded as the enemy.

and unlike the few other principal things powers that be want to take away from us - privacy, freedom of expression, gun ownership, there is no right to bear cash, so they can take it away anytime.

In the US it will be more of an "economic"-oriented change. I already encounter businesses once in a while that don't take cash, and rely entirely on a payment processor like Stripe or even Venmo. It's not a matter of evil vs. not-evil, it's a matter of "this is what was cheapest/easiest for us and why do you care anyway?"

In some U.S. cities, there are local laws requiring acceptance of cash by all businesses.

Outside tech bubbles, people are using more cash, not less. The Federal Reserve reports that U.S. currency in circulation has been steadily rising for decades, including the recent smartphone decade: https://fred.stlouisfed.org/series/CURRCIR

My "why do you care" was rhetorical/sarcastic. It was meant to be analogous to "what do you have to hide?" in the context of privacy discussions. Part of how these things get adopted is that people engage in "outsider-shaming" of the people who resist.

> Bills mandating cash acceptance have faced intensive lobbying from the credit card industry as well as more tech-focused retailers. The passage of the New Jersey legislation exemplifies such forces at work. The bill's sponsor specifically criticized a recent Visa initiative that rewarded 50 businesses with $10,000 each for making their operations cashless.

American cash is hoarded abroad, so I don't think that's very informative.

For the UK [1] (graph on page 2) shows the number of cash transactions made per year. There's a continual decline since 2012: "Since 2017 cash use had been declining by around 15% each year, so 2020 represented an acceleration of this decline ... Nevertheless, cash remained the second most frequently used payment method in the UK in 2020, being used for just under a fifth of the total number of payments made"

"At the same time there were 1.2 million consumers who mainly used cash, choosing this payment method when doing their day-to-day shopping (although the majority still use other payment methods to pay their regular bills). It should be noted that while these people prefer to use cash when paying for things, they are not necessarily unwilling or unable to use other methods of payment. The majority of them have a debit card"

[2] is the same for the USA (page 6). It shows similar cash use as the UK (1 in 5 transactions), plus credit cards used instead of debit cards.

For a much more cashless society, see Denmark [3]. Roughly a third of people don't carry any cash, and half carry less than 100kr ($15).

"There are differences in the use of cash between the youngest and the oldest Danes, but the tendency to move away from cash is seen in all age groups. In particular, senior citizens’ use of cash has declined in recent years: Among the 70 to 79-year-olds, 40 per cent of payments were made in cash in 2017. This figure was almost halved to 22 per cent in 2019.

"By comparison, the share of cash payments in physical trade fell from 9 per cent to 4 per cent among the 15 to 29-year-olds. Young people thus opt out of paying with cash in stores, but it is a change in behaviour among the oldest citizens which has been driving developments since 2017."

(Denmark has a national law requiring staffed businesses to accept cash, with some exceptions.)

> though you wouldn't know it from the ubiquitous swiveling iPads at your local coffee shop, cash is the most frequent method of payment in the US – more frequent than electronic, credit, debit, or check payments.

“A man’s rights rest in three boxes: the ballot box, the jury box, and the cartridge box.” - Frederick Douglass, 1867.

It's still true. Yes, all three are dangerous and open to abuse, but they - with the right protections in place - will provide better outcomes than the alternatives.

If Douglass could've conceived of a world without cash then perhaps he would've mentioned a fourth.

Don’t play the pronoun game, it makes the conversation hard to follow and reply to. Which one of the four things - privacy, freedom of expression, gun ownership, or right to bear cash - are you finding jarring?

In my community the folks here have a ratio of firearms to people of about 20:1. Many of them save their brass/steel and reload their own ammo. Most here carry concealed and are not required to have a permit. Same goes for some neighboring states. Permits are only required if traveling into a state that does not honor permit-less carry based on state ID.

As a funny side note this is only place I have lived where it is normal to see people get out of their vehicle with hunting/assault rifles at the gas station sorting/shifting their gear and nobody bats an eye. My bank has a fundraiser poster on the door for a rifle giveaway prize.

I wouldn't go for it either but this will pushed to the masses as something good and necessary, and most will simply go along with it. For the individual, losing cash and going "digital everything" means losing privacy, autonomy and sovereignty.

So,what happens when the following get ahold of your data:

Health insurance companies start buying your purchasing info and decide to up your premiums due to the amount of alcohol you buy, fast food you purchase, or your grocery shopping habits? Do you eat too much red meat, too many carbs, not enough greens? Is your sugar intake put you at a higher risk for diabetes? How may cigars/cigarettes are you smoking? What about marijuana use, or over the counter drugs?

Home owners insurance:

What if your shopping data shows risky patterns or behaviors - do you or spouse buy too many candles, is your home at a greater risk for fire hazard?

Law Enforcement:

How much ammo do you purchase? Are you frequently buying guns? Are you an active shooter risk? Are you spending too much at strip clubs? Are you spending too much money in high risk neighborhoods?

Obviously these are all just examples, but don't think for a second that they don't already have most of this data, and can brainstorm many other use cases for it, honestly we are just living on borrow time at the moment before it gets unbearable.

Then you vote to ban insurance discrimination on certain kinds of data. In California, for example, employers are forbidden to ask or use data on candidate salaries in their hiring process. In the US, health insurance companies are forbidden from discriminating based on pre-existing conditions.

A huge amount of middle and upper class people already voluntarily use cashless methods to spend & earn money. A huge amount of businesses are basically online-only and don't really support cash payments. Visa & Mastercard etc already engage in data sharing. Cash is just too inconvenient and will slowly recede over time, if you want to avoid discriminatory outcomes then advocate for legislation directly.

It might be inconvenient for some things (e.g., online purchases, buying houses or cars), but buying something at the store has worked very well for centuries; it's quick and easy. People on HN can't figure out cash?

> Whatever is going on, it's not about convenience.

Why not? I’ve worked in jobs in my life where I dealt with cash, had to count a register down to the last coin, check receipts, do cash runs to a bank and give the correct change. I even received cash tips.

I choose not to use cash because it would require me to go out of my way to an ATM and use it, then keep track of the amount of cash I have on me and make subsequent trips to the ATM as necessary. I could, and I used to do that, but it’s not something I did because I enjoyed my trips to the ATM. I did it so I could get a medium of exchange for my daily necessities, and now I don’t do that.

You don't usually have to make an extra "trip to the ATM" to get cash, you can combine it with shopping or other errands. In Germany many supermarket chains now even have a "withdraw cash for free when you pay with your card" service, which is very convenient. And "keeping track of the amount of cash you have" is simply looking into your wallet when buying something and seeing that you only have one or two small-ish bills left in there.

I agree though that cash handling is more of a hassle for the ones accepting cash than for the ones paying with it, and that's probably one of the drivers in getting rid of it...

We have that here too, it’s called cash back, and it doesn’t make cash more appealing.

I pay for almost all of my expenses with a credit card though, which does not give me the option to withdraw cash, so yes I would have to go out of my way still. It does however give me 5% back at the grocery store in points redeemable for cash at the end of the statement period, so for every $100 I’m spending I’m getting $5 back at the end of the month. Neat for things I was going to buy anyway, like food.

This also has the added benefit of never having to give out my debit card # to anyone. I would much rather deal with CC fraud than debit card fraud.

You also have to carry a large wallet capable of carrying cash. The last decade maybe longer I’ve used a small front pocket wallet that only holds cards. It’s more comfortable, and harder to steal.

I quit carrying a wallet several years ago and have never looked back. I just carry my driver's license, debit/credit card, and any cash I have in a pocket. It works well for me.

That works in Germany but not in the US. Euro bills are easy to distinguish by color and size and start at 5. With dollars you have a stack of greenish paper, many of which are $1 bills. Manageable, but definitely more inconvenient than Euros.

These threads on HN always trend the same way unfortunately :( Someone living in a market that has largely lived through the transition from cash to cashless commenting on how much more convenient it is to not have to carry cash around. People who’ve not lived that experience telling them they’re wrong.

I’m with you. Australia had been on this trajectory for a while and it accelerated in the early days of the pandemic. It’s incredibly convenient to _never_ have to plan ahead with how much cash I need to have, how much I need to withdrawal from the bank/while at the supermarket, if I need to make a special trip to either because I’m short for whatever my plans are later. I can leave my house with just my iPhone or Garmin watch and I know I’m covered for whatever my plans are. Even if that ends up being an evening of unexpected plans. It’s been a couple of years since I’ve needed to have cash on me at this point.

People that haven’t experienced it seem unconvinced. Those that have don’t need convincing.

> I’ve worked in jobs in my life where I dealt with cash, had to count a register down to the last coin, check receipts, do cash runs to a bank and give the correct change. I even received cash tips.

I'm talking about customers, not merchants. It's interesting how enthusiastically some on HN push cashlessness, as if they have some vested interest. Why is it so important.

> it would require me to go out of my way to an ATM

Or stop when you pass one for a couple minutes. Which saves some time paying credit card bills and dealing with fraud alerts, etc.

> I'm talking about customers, not merchants. It's interesting how enthusiastically some on HN push cashlessness, as if they have some vested interest. Why is it so important.

It’s not important to me, but I did take exception to your rhetoric:

1. That people on HN can’t figure out cash.

2. That it can’t just be about convenience. (This also just sounds conspiratorial.)

I have no vested interest in telling people not to use cash because I don’t spend my time telling people not to use cash. I no longer work in jobs where I have to handle it either, but what you have up there is an explanation as to why one person out in meatspace would just go cashless, and I don’t think I’m the exception here.

Apple Pay (and it’s related services) is just such a massive QoL improvement for those who choose to adopt it that for most that try it (I know at least one person that doesn’t like it), it does not take much convincing. I recently had the strange experience of my own mother thanking me for setting her phone up to use Apple Pay for her cards when previously she was against it (doesn’t trust new technology, thinks it’s spying on her, probably wouldn’t have the phone if I didn’t buy it and put her on my plan).

My experience mirrors yours. It's interesting to me that the details you give about being very familiar with cash handling seem to just get ignored.

At one point in my life I would regularly have two or three hundred dollars in cash on my person at all times, would pay rent in cash, repeated things like 'cash is king'. Now, I haven't touched cash consistently in years. I tap a card to pay for things. It is much more convenient, no coins, no worries that I've exposed money on my person to some one who will act on that knowledge.

I dunno. Feels like an electric kettle. I didn't forget how to boil water on the stove but pressing a button is more convenient and now I cannot forget to turn a heating element off.

In the last decade in the UK my family have lost their wallets/purses twice and credit card fraud once. I got my credit card fraud taken care off but was out of pocket for the cash in wallet/purse.

Win for cashless. (I’m not anti-cash but I certainly favour using cashless options wherever possible. Safer, plus you get loyalty points and in the UK there is no cash discount price so if you aren’t getting loyalty points on your card you are throwing money away / paying a premium for the privacy of cash)

When I used cash to buy something at the store, I have to take out my wallet, count the appropriate amount of cash, wait for the cashier to give back any change, confirm I got the right amount back.

If I use a credit card, I just insert a piece of plastic into a slot, and we're done. It's more convenient.

Negative side effects of using cash also include having to carry a bulging wallet when I'm constantly trying to minimize the stuff I have to carry.

Side effects of using credit card is that all my transactions are tracked, but the side effect of that side effect is that I know exactly what I'm spending where. And no, I'd rather not do a manual bookkeeping routine, which is what I'd have to do if I used cash.

Yes, there is the side effect that third party entities might also know what my transactions are, but I simply don't care. Maybe there is some far off scenario in the future where it can be used against me, but I view worrying about that remote possibility as premature optimization. I have far greater things to worry about.

I understand the benefits of using cash even if I don't find those benefits valuable for myself personally. But I don't understand how someone can find using cash more convenient than swiping a credit card.

> When I used cash to buy something at the store, I have to take out my wallet, count the appropriate amount of cash, wait for the cashier to give back any change, confirm I got the right amount back.

> If I use a credit card, I just insert a piece of plastic into a slot, and we're done. It's more convenient.

You're comparing the worst-case of cash to best-case of a credit card.

For a single transaction, is it even possible to make a transaction with a credit card when:

- The chip/card reader fails?

- The network connection is down?

- There's a power outage?

It's not just inconvenient; in some cases, the transaction is impossible.

Let's extend this to monthly time lost over a day or a month. Here's what I lose with credit cards strictly from a convenience perspective and with common edge and use cases:

- For daily budgeting, I have to mentally keep of my credit card transactions; or go into an app. That's time wasted.

- I have to review each purchase on a daily and monthly basis, to make sure I'm not hit with fraudulent charges. It's not enough to get notified by SMS or app.

- We have to consolidate our monthly expenses, to make sure we're not going over our monthly budget.

- If there's a fraudulent charge, I now have to contact the credit card and dispute the charges.

- If the credit card helpfully decides to up the limit, I have to cheerfully tell them to decrease it; in order to minimize the damage.

In the case of a stolen wallet with cash, what I lose is what I withdrew. There's a very simple and hard ceiling to the loss.

There is one group for which cashless is far more convenient: Big-company merchants and businesses.

> For a single transaction, is it even possible to make a transaction with a credit card when: - The chip/card reader fails? - The network connection is down? - There's a power outage?

I use cards for 99% of my payments. For me, this simply hasn't been an issue in actual reality. In fact, I've had far more issues getting cash into and out of the handful of ATMs in my area that work with my credit union.

I keep about $100 in each car and $1000 in my house in case I find I desperately need cash. The car money comes in handy sometimes if there's a cash discount for gas or I drive someplace and realize I've forgotten my wallet.

Why would a gas station offer discount for cash for any reason other than to avoid it going through the books and hence avoid obligations like paying tax or their staff a proper wage?

Card payment processors charge the merchant some premium. Usually their contract with the merchant prevents passing the fee along to the customer. A cash discount could be a way to get more customers to pay in cash, which avoids the credit card company's cut. This is probably violating the terms of the merchant/card company contract, but I dunno, hard to resent the merchant here given the power imbalance between them and the card processors.

How would using cash would be an effective way of denying the gas station's staff a proper wage? I suspect most gas station staff is hourly, rather than... I dunno, tipped or commission.

Cash could certainly be a way of avoiding some taxes.

A lot of places do this, whether it is "allowed" or not. But my understanding is that after much push and pull between merchants and processors, most processors do allow it.

The gas stations would have never had any credit card uptake without it and people have to buy gas and are extremely price sensitive so would have continued shopping at cash only gas stations.

Unlike say a clothing store where the convenience of credit overcomes the price sensitivity, you can defer the purchase and the merchant has higher margins.

For a cash transaction is it even possible if the store does not have matching change on hand?

That is actually a common annoyance here in Germany, where bakeries will complain or even refuse a sale if you try to pay with a "too large" bill, e.g. 20 for 4.50.

>For a single transaction, is it even possible to make a transaction with a credit card when: - The chip/card reader fails? - The network connection is down? - There's a power outage?

In the power outage situation, the merchant won't be able to handle any transactions and they may not be able to legally open their doors even if they could. I don't think I've ever encountered the other two scenarios ever. I would imagine that CC payment systems have resiliency for a network failure and most businesses have at least two card/chip reader terminals for transactions.

I've been reading through this thread and trying to figure out what the disconnect between you and everyone else, I think it's probably your poor experience with chip readers. I had the same deal, it was frustrating, and not as convenient as cash. It made me resistant to the tap system because I felt I really did not need more faulty bullshit. Now for whatever reason I have a card that has a chip and the tap, and crucially, most of the places have systems where the tap consistently works (except one that is faulty and uses the chip read and reminds me how little I liked that). It's like always having exact change but faster.

Anyway, not trying to change your mind (pay with checks and bottle caps for all I care), but you seemed suspicious in some of your responses and I thought it might be helpful to share that perspective. I would also be suspicious if it sounded like people were recommending something that I personally knew to be a consistent frustration.

I bought from a computer store during a localized power outage about 15 years ago (not the great blackout of 2003). I paid cash, the clerk hand-wrote a receipt on a pre-printed form, and presumably they kept a second copy of the receipt to input electronically when the power eventually came back.

So I’ve worked retail during a power outage, granted it was roughly 15 years ago, at a Blockbuster. We used a pen and paper list of transactions (literally a cash register) along with necessary info (membership number, movie purchased or rented) and entered them by hand when power came back.

> For a single transaction, is it even possible to make a transaction with a credit card when: - The chip/card reader fails? - The network connection is down? - There's a power outage?

Imprint machines still exist, and maybe half of my cards still have raised numbers. If all else fails, the merchant may be willing to write down name, phone number, and amount and either ask the customer to come by later to make it right (and call if not) or write the card number down to run the charge later and call to confirm, etc. There's ways to get network redundancy and power redundancy, if it's of value to the merchant.

Sometimes the merchant doesn't have the right change for cash (or would prefer not to take a large bill), or may not be able to open the register if power is unavailable (usually there's a key, but it might not be onsite).

You don't need to review charges on a daily basis, monthly is sufficent to keep your rights (at least in the US)

There's also such a thing as offline transactions, for when the internet is down. As I understand it, most POS terminals do support that.

Power outages are indeed an issue, especially when the business is in a small town or rural community with a flakier power grid.

Where I work, when the power is out, we rely on cash or writing down the customer's name and amount they owe, and add that to their account when the power's back.

I already mentioned this in the following if you read the rest:

> In the case of a stolen wallet with cash, what I lose is what I withdrew. There's a very simple and hard ceiling to the loss.

I was responding to the very narrow use-case of already being at the register and starting to pay, in order to keep the objections relevant.