I bought $300 worth of silver last night, and I plan to buy more while I can. The government is injecting a massively gigantic amount of cash into the economy to counter the decreased velocity of money, but within a year and a half or so, the velocity of money will sharply increase, possibly higher than before. That will cause such a high rate of inflation that I'm afraid of what could happen. I bought physical coins because I don't know if the financial institutions will waver, crumple, or at very least become inaccessible for a while. I've stashed some cash too in case there's a run on the banks, but I don't know if they will be worth as much.

Basically I'm preparing for a global depression. This sudden shock to the economy is unprecedented in any modern time, and we have no idea what could happen.

I'm currently taking the "Economics of Money and Banking" course on coursera [0] and, as far as my understanding has developed, the Fed injecting cash is not an irreversible thing.

When the liquidity crunch is over, the Fed will start gradually increasing the rate. That will make rolling over existing overnight loans taken from the Fed less attractive and a lot of money will flow back to the Fed.

I hope people more familiar with the subject will correct me if I'm wrong.

Currently the issue is that the fed has removed the overnight liquidity requirements. This opens up the threat of a bank run. All of this is due to years of aggressively propping up the economy for political means, in reality we should have had a market decline a few years ago, but the government massively mismanaged their responsibilities and pushed us into more than one bubble, while hamstringing their ability to respond.

Yes, and in 1Q2017, the fund held $84.9E9. Meanwhile, in the US, gross private savings total $4.64 trillion, while personal savings total $1.06 trillion.(Sep 11, 2019)

What happens when a major bank goes under and completely depletes the FDIC fund? (e.g. Bank of America)

Another key aspect of monetary metals is lack of counter party risk. When you deposit money with BoA, it is no longer yours; you become an unsecured creditor of the bank. BoA's derivatives counter parties are senior to you, so they will get paid first if say interest rate swaps go against BoA, and they need to post more collateral to that counter party.

Also, the problem with rates 'normalizing' is the magnitude of outstanding Treasury debt, and the fraction of GDP that the interest payments represent. 5% would be devastating, even though historically, that is a typical rate.

If you're not transacting for physical cash, isn't your money going directly into an account at another bank?

Unless people are withdrawing mass amounts of cash, I'm relatively certain you can't have bank runs against the banking system as a whole, you can only have runs against a particular bank.

The Fed and other central banks have almost total control over nominal inflation because they control the printing presses. They can create money by buying bonds and destroy it by selling them. They have bugger all control over real inflation but that’s a matter for the fiscal authorities to try and deal with by demand management.

“Inflation is always and everywhere a monetary phenomenon.” Milton Friedman

Edited to fix elementary mistake as pointed out by forkerenok

We've never had hyperinflation in the US. We've had high inflation, but never hyperinflation. And we've had very low inflation since the 80s, including during the decade-plus period of practically-zero interest rates.

Hyperinflation is a completely different issue from inflation, and it's kind of odd for it to become the monetarist bugaboo. When the US has a massive war debt payable immediately, or a complete economic collapse that the government decides to cope with by price controls, then you'll see hyperinflation. But then, hyperinflation will be the least of your problems.

Not technically the US, but the Confederacy did experience hyperinflation during the war. They ran the printing presses at full-tilt without anything tangible to back them up. And obviously once the tide of the war shifted things got real bad.

Also not technically the U.S, but during the Revolutionary War the continental dollar underwent hyperinflation, leading to the phrase "not worth a continental". By the end of the war they were worth less than 1% of face value and had ceased to circulate as money.

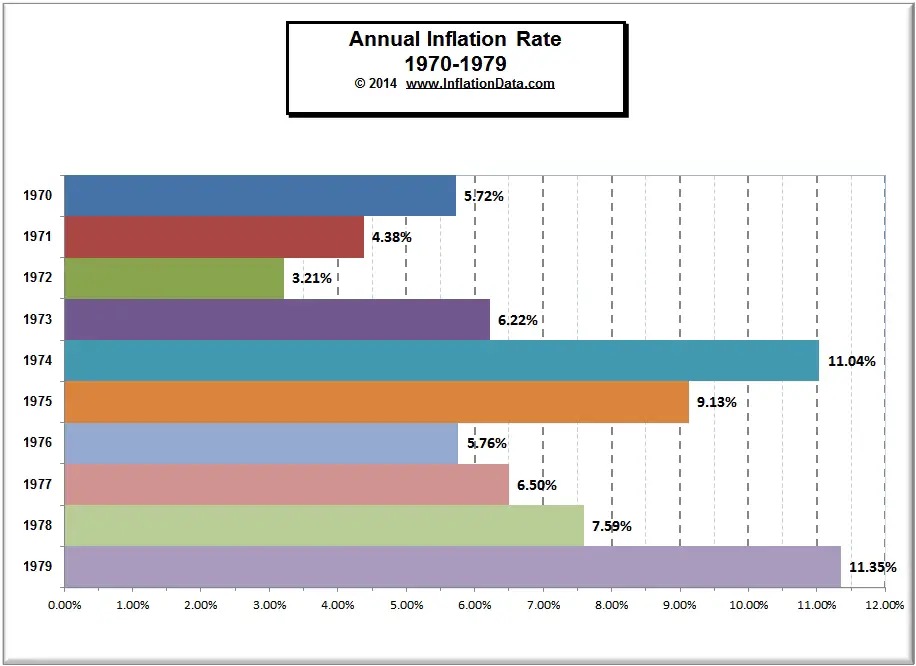

Well... the 1970s weren't a hyperinflation, but we were trending there. Inflation was not only high, it was increasing. Would we have wound up at hyperinflation if Volcker hadn't clamped down at the Fed? I don't know; that's alternate history. But it felt like we were headed there.

I'm sorry, but this is just wrong: inflation was high but fluctuated a lot and by no way you can say it was “increasing”. You're rewriting history in favor of your political bias.

I'm sorry, are you psychic? I didn't say anything about a political bias, nor anything to even hint at one. You're making up stuff that you think you know about me, with no basis.

To the data: I agree that there are fluctuations there. But average inflation for the decade of the 1960s was 2.45%. For the 1950s, it was 1.82%. The inflation rate even for 1972 was above the average rate for the 1950s and 1960s. 1976, the bottom of the next trough, was higher than 1972. And then you look at 1974 and 1979, in the context of the 1950s and 1960s, and yes, it sure does look like inflation is increasing. Yes, there are decreases (business cycle), but each cycle is higher than the last one.

First of all, inflation and hyperinflation are two really different things. The first one being common in history while the second one is rare but catastrophic.

Then, In Friedman's book inflation is related to the amount of money in circulation, yet since the 80s the amount of money and inflation have almost zero correlation in the US. Some of Friedman's concepts were useful to reach that point, but still: we now have been living for 40 years in a world where Friedman's model is unable to explain anything.

That's mostly true (except as another comment says, the "sell" and "buy" are backwards).

Certainly the central bank can create as much inflation as it wants, by simply printing and distributing more money (which usually takes the form of the central bank buying assets such as bonds with the new money). There's no limit to the ability of the central bank to make the currency valueless.

In the other direction, they can usually increase the value of money (ie, create deflation) by reducing the money supply, but it is possible that at some point the public might simply stop regarding the government's money as being worth anything. The only thing that might stop that is that people would still need government money to pay taxes.

Did you actually mean it the other way around as in they can create money by buying govt bonds/treasury bills/etc and retire them by selling them back to the market.

> The Fed and other central banks have almost total control over nominal inflation because they control the printing presses.

Not quite true. Every bank can print money (well, the modern day equivalent of increasing a digital number somewhere), and does so when they make loans.

I hope you realize that you think you have figured out something that markets don't. Markets see decades of low inflation.

Central banks know how to stop inflation, that's not a problem for them at all.

The problem for the next 10 years will be low inflation, not large inflation.

Yes, this is a risk and it makes sense. During the great depression, there were significant decreases in inflation[1]. But what am I risking? I might lose 50% of the few thousand dollars I put into silver, but it protects me against unexpected movements or a dollar crash during an unparalleled period of time in modern history. It ensures I'll have money to eat.

By all means keep little silver or gold in the case the whole society collapses or for emotional reasons. You don't have to defend it. You have to defend the argumentation you arrived into it.

The problem I had your comment was the rationalization for what you did.

When US was trying to hold to gold standard, population growth was high and the country was barely industrialized, you could expect inflation. None of the reasons that applied then apply today.

(Gold standard is similar to debt in denominated in foreign currency. It can cause out of control inflation and even hyperinflation.)

I understand there may be flaws in my logic, but what flaws were there? You basically said I was wrong and the market believes otherwise, but you didn't explain how my beliefs on the varying velocity of money wouldn't or couldn't create inflation in the next year or so.

That chart kind of proves my point though. People are moving from stocks to bonds as risk in stocks increases, yet the long-term outlook of the economy(10+ years) is largely unchanged. Despite this, the government is injecting tons of money during a time of a global quarantine that will eventually be lifted. When that lifts, people will buy a surge of supplies that they are depleting during this time, leading to a spike in demand in most things. Am I seeing this wrong?

That spike in demand will pass, and we will (we hope) settle down to a steady state. That steady state is (in the market's opinion) not much different from the steady state that we would have had without the pandemic. That's why the market is still predicting the 10-years-out state as being the same as it predicted before this crisis.

Right now they're terrified of deflation. A lockdown is going to cause a massive drop in consumption and a massive drop in wages, making a vicious circle of falling prices that could continue well past the end of quarantine. They'll be happy just to keep prices stable.

Deflation wouldn't be so bad. everyone says it is because they think people will stop buying stuff. really? will people check the CPI figures before they go to the grocery store, everytime? stop buying bread because the inflation figures say it'll be cheaper by 25c next year? will factories stop because they won't buy parts, so they can save 1% on parts? i don't think so.

people and govt's are addicted to debt, that's why they want inflation.

There may well be serious real problems, which the central bank can't magically solve. But if you're just worried that there might not be "enough" inflation, the central bank has unlimited ability to create that, if it wishes to. (Of course, whether such inflation would be a good idea is debatable, and could depend on the circumstances.)

No, Japan has not really tried to create inflation. If they had, they would have succeeded.

If the government prints lots of cash, and then mails a bunch of cash to every person in the country, then there will be inflation. Lots of inflation, if the amount of cash is high enough. And there's no limit to how high the amount can be.

To doubt that, you have to believe that someone of previously modest means who now has a million dollars of cash in hand will just horde it, rather than go out and buy the $40,000 car they've been wishing they had, or the nice $500,000 house they now could live in, or the nifty $10,000 camera and lens set that would be really fun to play with, or the...

Actually, you don't have to just believe that someone will horde immense amounts of cash rather than buy real, useful stuff with it, you have to believe that almost everyone will horde the cash.

If I remember correctly from my econ classes, deflation has a nasty spiraling effect where any currency introduced into the system is subsequently hoarded, which decreases economic activity which makes money even more valuable which increases hoarding ...

There are many tools in the toolbox for handling inflation. For deflation, not so much.

The central bank can create unlimited inflation in financial assets. In, say, food, or cars, not so much. (I mean, I guess they could buy a bunch of food and cars, but that's pretty far out there, even for the current expansive definitions of what the central banks can do.)

I disagree. The sudden jump in equity prices that happened over the last few years looks to me like a classic case of the markets pricing in high future inflation.

I think it's kind of the reverse. Stocks should sell at risk-adjusted rate-of-return parity with bonds. If inflation is 1% (and is expected to stay there), then what's $1 of corporate profit worth? $100 (same as $1 of bond interest would cost). So the stock market has soared because interest rates have fallen. Money has moved into the stock market, seeking rates of return, and has continued to do so until the rate of return of stocks was not higher than the rate of return of bonds.

Huge amounts of cash has been printed and used to buy bonds over the last ten years, I don't think the bond market is a useful means of price discovery as a result.

They see decades of low inflation until they don't. The post-WWII US had a couple decades of low inflation in the 50s/60s, followed by a couple decades of high inflation in the 70s/80s. Central banks do know how to stop inflation, but there can be pressure not to in some situations.

I don't think this is correct. Because as you can see the spot price of silver has gone down, the price for silver coins has gone up by more than double the amount the spot price has declined. Meaning, people are buying silver out of fear.

My guess is that this is the product of silver prices being driven by industry much more than gold prices are. We're looking at a supply side decline here which means a decline in demand for the things that go into making other things.

> I don't think this is correct. Because as you can see the spot price of silver has gone down, the price for silver coins has gone up by more than double the amount the spot price has declined. Meaning, people are buying silver out of fear.

> My guess is that this is the product of silver prices being driven by industry much more than gold prices are. We're looking at a supply side decline here which means a decline in demand for the things that go into making other things.

> Gold is far less useful industrially than silver.

For whatever reason, there is a common misconception regarding the usefulness of gold. Commonly on any of the popular investment shows and websites, you will see various people stating "gold has no use" without any measure of a qualifying statement.

My perception is that these people likely mean "gold has no use [as an asset]." The degree to which this is correct is not what I'm trying to address, but rather the literal interpretation of the statement that could be read as "gold has [absolutely] no use."

Here is the intro from the article on gold at geology.com[1], which doesn't have a dog in this fight:

> What is Gold?

> Native gold is an element and a mineral. It is highly prized by people because of its attractive color, its rarity, resistance to tarnish, and its many special properties - some of which are unique to gold. No other element has more uses than gold. All of these factors help support a price of gold that is higher than all but a few other metals.

The argument being made is about industrial use. Outside of electronics which have such little gold that it's not even worth the chemicals to extract it back out, Gold really doesn't have much use industrially. It's use as a currency and jewelry is quite obvious, but that's another human fiction like fiat currency. It has no other inherent value. We can't eat it. We can't even really wipe our butts with it. Gold is shiny, and remains shiny for a long time. End of story.

> The argument being made is about industrial use. Outside of electronics which have such little gold that it's not even worth the chemicals to extract it back out, Gold really doesn't have much use industrially. It's use as a currency and jewelry is quite obvious, but that's another human fiction like fiat currency. It has no other inherent value. We can't eat it. We can't even really wipe our butts with it. Gold is shiny, and remains shiny for a long time. End of story.

Sounds like a very scientific position you've laid out here against the editors ate geology.com. Why don't you send that to them and post there response here?

Geology.com isn't scientific literature. It's a SEO spam site.

You can tell because (a) the way the page is covered in ads, (b) the simple language used to improve search engine traffic and (c) the lack of references.

> Geology.com isn't scientific literature. It's a SEO spam site.

> You can tell because (a) the way the page is covered in ads, (b) the simple language used to improve search engine traffic and (c) the lack of references.

If the information provided is so poor, you should easily be able to disprove the claims.

> You appealed to authority, it's pretty legitimate to point out that it isn't actually an authority on the subject.

> If the information provided is so poor, you should easily be able to disprove the claims.

> As previously pointed out, only 10% of gold is used in industry.

I'm guessing you are referring to an appeal to false authority, because the acquisition of all knowledge presumably originates from an authority. If you are claiming that geology.com has presented false information, then you need to demonstrate this. Stating that it makes money from ads is not a claim against the provided information. You have inserted an arbitrarily derived claim.

Your statement of percent of gold makes no sense. From the World Gold Council[1]:

Further, if we take the total amount of above ground stocks and multiply it by the current gold price of around $1500, we find that the current markets value the total gold at over $10 trillion. If 90% of gold mined isn't in use, why is it valued at $9 trillion? And if the remaining 10% of gold has such little usefulness, why choose such an expensive mineral?

And all of this supports my original point that gold has uses.

Silver is unproductive and speculative. It is just as volatile as any single investment, and there is even less guarantee of it remaining stable as with gold.

To actually hedge against the breakdown of societies, cigarettes are probably more attractive.

I'm very long caffeine in that scenario actually, fewer smokers than the last time we had massive currency devaluation. It's annoyingly tough to store unfortunately.

Buy .22LR, some chickens, and a goat. You can use the chickens for egg and meat, the goat for milk and meat, and the .22LR for varmint hunting and trading.

Better hurry up, though; ammo prices are skyrocketing, though .22LR has been fairly stable at a touch over $0.03/round.

One could bet on people not being aware of that after the economy collapses. It's going to go back to bartering then, and initially the value of gold and silver will be pretty much random.

The problem with silver is the much larger supply compared to gold and the market cap is comparatively tiny (even less than the cryptocurrency market!). It's if course possible, but I find it quite unlikely.

Gold price is not fixed by the free market as people think but by few powerful banks/company that for sure can build covered trusts and control it to their bests needs.

See https://en.wikipedia.org/wiki/Gold_fixing

On the contrary - that article seems to show that the London fix is a free market process. If an individual bank wants to increase the price of gold they must commit to buying gold at great volumes to cause that market movement. OTOH if all the banks conspire to move gold in some direction, any one of them can betray and profit at the expense of all the others knowing the movement is artificial.

You can’t fix prices unless you’re either willing to sell enough or buy enough to fix it. If you can’t do that then eventually the peg breaks. See the collapse of the dollar gold peg in the 1970s when France wanted gold from the US, or the collapse of the UK’s peg to the DM on Black Monday.

If that happens, then the government will take money out of circulation. Right now the Fed is printing money to buy assets. When they need to reverse it, they sell the assets, and then remove the money they make from circulation.

The Fed has $4 trillion of assets on their balance sheets right now. They'll find something to sell.

Anyway, they're not buying subprime auto loans or overinflated stocks. They're buying long term risk-free debt, and are going to start buying commercial paper (which has some risk, but not much).

They really did buy lots of different stuff during the financial crisis, and yet they never lost control of inflation.

> Anyway, they're not buying subprime auto loans or overinflated stocks. They're buying long term risk-free debt, and are going to start buying commercial paper (which has some risk, but not much).

Eligible Collateral•Collateral eligible for pledge under the PDCF includes all collateral eligible for pledge in open market operations (OMO); plus investment grade corporate debt securities, international agency securities, commercial paper, municipal securities, mortgage-backed securities, and asset-backed securities; plus equity securities. Foreign currency-denominated securities are not eligible for pledge under the PDCF at this time.

--

equity securities == stocks. I admit I was exaggerating about the subprime auto loans, but they also state that: Additional collateral may become eligible at a later date upon further analysis., so who knows?

I agree with you they have plenty of stuff old stuff to sell from QE 1-4, but this certainly is a new class of assets from them, and is almost certain to lose money.

If you expect depression plus inflation, wouldn't buying TIPS make more sense? Silver might have higher volatility in a depression, but TIPS probably won't, and they hedge against inflation as well as silver.

The inflation has been in speculative assets. This happened because the expansion of the money supply did not go to the people. In addition, there is debate about how accurate the inflation figures are. Some alternative measures are far higher.

From what I recall, all the 'inflation hawks' that were complaining about the Fed's QE were talking about the CPI and turning into Zimbabwe (or wherever):

> The planned asset purchases risk currency debasement and inflation, and we do not think they will achieve the Fed's objective of promoting employment.

> Thus when Bloomberg tried, four years later, to track down economists who signed the infamous open letter to Ben Bernanke insisting that quantitative easing would “debase the dollar,” it couldn’t find a single person to admit that the original warning was wrong.

> In addition, there is debate about how accurate the inflation figures are.

There are different inflation figures, and they each focus on slightly different things, and there is some debate as to what best measure what "real people" experience in day-to-day life. There are also "perma-too-low" types who say that the books are being cooked, but I think it's been shown that the official numbers are fairly accurate:

If he's trying to protect against inflation in speculative asset prices for some reason then he should invest in some of those assets, not silver, which is uncorrelated.

Exactly. The Fed and government have been trying for over a decade to generate some inflation and decrease the value of the dollar. It's proven nigh impossible, because the American economy is, relatively, too strong, and the demand for USD too great.

What is going to change that? The US may be printing money, but so is every other country on the planet.

The demand for USD being too great is not because the American economy is strong, but rather because there is $12 Trillion in dollar denominated debt owed by the rest of the world. At 2% interest this is $240 Billion worth of USD that has to be paid out every year.

And now because of the world economy shutting down, those dollars aren't being fed back into the markets outside of the US, meaning that no one can generate the cash to repay their loans.

This is why cash is so high priced right now, even while the Fed is desperately trying to lower it. It's also why gold and silver are taking a beating. In order to raise cash not to default, foreign corporations and governments have no choice but to sell everything they own, including gold and silver (as well as cryptocurrencies).

>The demand for USD being too great is not because the American economy is strong, but rather because there is $12 Trillion in dollar denominated debt owed by the rest of the world.

Why does the rest of the world deal in dollars, and not Yuan or Rubles? Hint: not because the US is a weak, unstable economy.

"Inflation is a quantitative measure of the rate at which the average price level of a basket of selected goods and services in an economy increases over a period of time. It is the constant rise in the general level of prices where a unit of currency buys less than it did in prior periods"

And if the OP is trying to protect (?) against rising asset prices, then they should invest in the assets that are appreciating not in silver which isn't really correlated with asset prices.

If you look at the money supply graphs, there is a tremendous amount of money that has been making its way through the world in the last decade. You can probably redefine inflation until you get something that hasn't increased in the last decade but you have to at least say what that is.

The "standard" definition preferred by political economists (for the obvious reasons) is useless for making accurate predictions. The economic effects of inflation are all due to the changes in the money supply; the changes in prices are an side effect of this and many other factors, not a cause.

You can't just look at the money supply. Let's say that we hold the money supply perfectly constant. Then one dollar becomes worth, not a fixed amount, but a fixed fraction of the economy (assuming velocity remains constant).

For example, let's say that there are 1000 dollars in circulation, and the velocity is 2 - on average, each dollar changes hands twice in a year. So the GDP is $2000.

Ten years pass. We learn to be more efficient. The economy produces 20% more than it did ten years ago. But the GDP is still $2000, because that's how much money there is.

That seems unreasonable to me. If I saved a dollar, why does that dollar give me a claim, not just to what the dollar would have bought when I saved it, but also a claim on a part of all the growth since I saved it?

> The economy produces 20% more than it did ten years ago. But the GDP is still $2000, because that's how much money there is.

More or less, yes. The improved efficiency is reflected in the fact that prices are now 20% lower, so the same GDP buys more goods. I'm not saying that prices shouldn't be considered. Prices are an important economic metric—which is exactly why it's a bad idea to conflate natural price signals with the noise caused by artificial changes in the money supply.

> If I saved a dollar, why does that dollar give me a claim, not just to what the dollar would have bought when I saved it, but also a claim on a part of all the growth since I saved it?

Because the improved efficiency and growth are in part due to the fact you chose to save that dollar, meaning that during that time there were $1 worth of extra goods and services available for other people to invest or consume. You created a surplus and essentially loaned it to everyone else by choosing to consume $1 less than you produced. The drop in prices is the interest on that loan.

Of course, it could go the other way too. If people choose to consume capital rather than invest in the future then the economy could shrink, resulting in rising prices. The general rate of return represented by deflation or inflation (in the absence of interference with the money supply) represents the baseline level of return a venture needs to offer in order to be worth investing in, not just for the individual—who would be looking for the best rate of return in any case—but for the economy as a whole. If you can't find anything better to invest in than the real-valued return you would get from stuffing your money in a mattress and waiting, we're all better off if you do just that and avoid taking resources away from actually beneficial investments. An inflationary economy incentivises people to invest more, but if the inflation is artificial then the result is a lot of malinvestment from people simply looking for a safe haven for their money, even if it's still losing real value over time.

> Because the improved efficiency and growth are in part due to the fact you chose to save that dollar, meaning that during that time there were $1 worth of extra goods and services available for other people to invest or consume. You created a surplus and essentially loaned it to everyone else by choosing to consume $1 less than you produced. The drop in prices is the interest on that loan.

Well, no, the "interest on that loan" is the return on the investment. I lent the money to company A, they bought some tools to improve productivity, and they paid me back part of the increased value they produced. That's my reward for consuming less - I got my $1 back, plus some.

But at the same time, company B borrowed some money from somebody else, and used it to increase productivity. So did companies C through Z. Why should I get rewarded for my loan to A by the gains in productivity made by B through Z?

> Well, no, the "interest on that loan" is the return on the investment.

Exactly as I said. The "return on the investment", for saving money in a deflationary economy, is the increase in the amount of stuff you can buy with that money. Which is exactly what I referred to earlier as the "interest on that loan".

> I lent the money to company A, they bought some tools to improve productivity, and they paid me back part of the increased value they produced. That's my reward for consuming less - I got my $1 back, plus some.

Except you didn't literally loan the money to company A, you (in effect) loaned the value of the money to everyone—including companies B through Z in your example—by temporarily taking it out of circulation. You could have bought $1 worth of stuff for yourself with that money but chose not to, so that stuff was available for others to buy, and their prices were a bit lower since you weren't bidding against them.

Money is just a stand-in for other goods. It's not a consumable end product, an intermediate material, or a capital good which can be used to produce other goods more efficiently. If it helps, think of that $1 in savings as one share of ownership in the entire economy—a claim to a little bit of everything being produced. Or an extremely broad index fund. As the amount of goods being produced changes, the value of your share also changes, the same as any other equity investment. When you eventually trade your share in the economy for an equivalent fraction of the available goods, if your investment in the economy helped it to grow (along with others' investments, of course) then one share's worth of goods will be a bit more than it would have been before you invested.

Do you have an issue with the idea that a person can buy shares of IPO stock in a company, funding the company's growth, and then be rewarded later by selling those shares a higher price? If so, I probably can't help you; otherwise, this is essentially the same thing but for the entire economy rather than one company.

I can sort of twist my mind far enough to see what you're saying about not using the resources leaves those resources available to everyone else. But...

I could have it both ways. I could lend the dollar to A, and get paid back a decade later with interest. Now I have (more than) a dollar after the decade. But that dollar is still worth 1/2000 of the year's output, so I also got paid for everyone else's gains, even when I didn't leave them the resources (because A had the resources, because I lent the dollar to A).

Even within your perspective, I have a hard time seeing how that would be considered just.

> I could have it both ways. I could lend the dollar to A, and get paid back a decade later with interest. Now I have (more than) a dollar after the decade. But that dollar is still worth 1/2000 of the year's output, so I also got paid for everyone else's gains, even when I didn't leave them the resources...

So company A paid you back your original nominal investment, which is already worth more than it was at the start, plus interest, which means that whatever they did produced a better-than-average return for them to be able to afford to repay the loan. You did something even better than just hold your money and wait without interfering—you contributed to raising the average rate of return. Resources (others' savings, as well as your own funds) were put to better use due to your wise choice of investment. Ergo, you get a higher reward than those who just passively waited for the economy to improve.

This whole discussion is missing a major point in my eyes.

Inflationary expectations is a major driver of inflation of prices. If people expect the prices to increase, they will buy earlier. That leads to producers having pricing power, so they tend to increase prices, which leads to... higher prices, and confirms the consumer expectations.

This is also why you can't really use money supply as a measure of inflation. As you note "money is just a stand-in for other goods" - which of course leads to the standard definition of inflation. If money is a stand-in for other goods, then we measure how much of these good money can buy. That's exactly what the standard definition of inflation captures.

> If money is a stand-in for other goods, then we measure how much of these good money can buy. That's exactly what the standard definition of inflation captures.

Which is completely useless if you don't take into account how much money people have to buy things with. What you want is a metric of prices vs. wages, which neither version of inflation takes into account. Money supply inflation would be a better predictor of prices vs. wages, however, since when the money supply is inflated prices tend to rise faster than wages (and vice-versa). Price inflation is a lagging indicator which incorporates a bunch of noise along with the delayed signal, especially when the supply is deliberately manipulated to achieve specific CPI targets.

For an even better predictor, look at money supply vs. actual economic output. If the economy's producing 20% more actual stuff, and the money supply grew 20%, that's not inflation. That's stability.

The standard definition of inflation is a standard for a good reason: it's what effects consumers!

It's been that definition all through the 1970s when inflation was a real problem, so your implications it is that for political reasons is incorrect.

You can keep trying to argue for a different definition, but the OP was clearly trying to hedge against consumer price inflation - otherwise he'd hedge for investment asset inflation by investing in the assets subject to that increases, not a metal like silver which isn't correlated with those increases.

> The standard definition of inflation is a standard for a good reason: it's what effects consumers!

No, what affects consumers is how consumer prices have changed relative to wages. The CPI doesn't tell you that, or really anything else of value. Hypothetically, let's say the CPI indicates that prices are double what they were ten years ago. Is the median consumer better or worse off? Who knows! Maybe wages are the same as they were ten years ago, and everything takes twice as much work to acquire. Maybe wages have tripled in that time and goods seem cheap. Without a fixed money supply, all it really tells you is that someone set a CPI target that resulted in doubling the prices over ten years. In other words, a tautology. Which is a shame, really, since the fluctuations in general price levels would otherwise tell us useful things about how much investment is needed and what the minimum return should be for a venture to be considered worthwhile.

Inflation (as measured by the CPI) measures price changes. Wage indexes measure wage changes.

You want to measure both separately so you can do exactly the kinds of comparisons you want to do above ("Hypothetically, let's say the CPI indicates that prices are double what they were ten years ago. Is the median consumer better or worse off? Who knows! Maybe wages are the same as they were ten years ago, and everything takes twice as much work to acquire. Maybe wages have tripled in that time and goods seem cheap.")

Money supply is measured separately since it affects lots of other things too (eg, the relationship between interest rates and money supply). You have to measure all these things separately because that lets you tease apart the relationships.

Again, if the OP is talking about increases in money supply (which I agree can lead to increases in the speculative assets) then you need to explain how buying silver would protect against those increases (since the silver price is uncorrelated with those speculative increases).

There's certainly nothing wrong with being prepared.

However, the idea that our institutions crumple but your hard currency coins are safe is naive at best. In such a scenario, if the metal has any value, either the government will confiscate it or your neighbour with the gun will take it.

>The government is injecting a massively gigantic amount of cash into the economy

What is "massive"? Right now they are talking about $2 trillion, which is about 10% of GDP. Spending 10% of 1 year of income on "maintenance" isn't scary to me.

> What is "massive"? Right now they are talking about $2 trillion, which is about 10% of GDP. Spending 10% of 1 year of income on "maintenance" isn't scary to me.

The Quantitative Easing program from 2008-2014 (6 years duration) injected about $4T into the economy. Today, a similar amount is being injected in just 1 month, albeit by purchasing different assets.

You will obviously be a very rich person by allocating your portfolio to take advantage of this massive inflation. Just like all of the people who called for massive inflation starting in 2009..

You have to ask where those 10% are taken from so we can spend them on maintenance. The smartest move would be to immediately slash military budget in half if not more.

But it will likely be taken from education, infrastructure or healthcare/social services.

The dollar is the worlds reserve currency. American printing presses have more life in them than other countries.

Look at the countries that have opposed that since the beginning of the millennium: Libya and Iraq saw, ahem, “kinetic interventions”, and Iran and Venezuela are still being crushed by sanctions for daring to price their oil in Euros and/or RMB.

Take 2008, for instance. The Fed injected $4 trillion. Why? Because $4 Trillion evaporated in the crash. The result was that we didn't have a deflationary meltdown, but it didn't result in inflation.

Most loans are against tangible, reposseable assets, or against future income streams. A bank that just handed out loans without commensurate interest rates to avoid the risk of default would quickly go out of business.

{kind=link}

Basically I'm preparing for a global depression. This sudden shock to the economy is unprecedented in any modern time, and we have no idea what could happen.