I'm currently taking the "Economics of Money and Banking" course on coursera [0] and, as far as my understanding has developed, the Fed injecting cash is not an irreversible thing.

When the liquidity crunch is over, the Fed will start gradually increasing the rate. That will make rolling over existing overnight loans taken from the Fed less attractive and a lot of money will flow back to the Fed.

I hope people more familiar with the subject will correct me if I'm wrong.

Currently the issue is that the fed has removed the overnight liquidity requirements. This opens up the threat of a bank run. All of this is due to years of aggressively propping up the economy for political means, in reality we should have had a market decline a few years ago, but the government massively mismanaged their responsibilities and pushed us into more than one bubble, while hamstringing their ability to respond.

Yes, and in 1Q2017, the fund held $84.9E9. Meanwhile, in the US, gross private savings total $4.64 trillion, while personal savings total $1.06 trillion.(Sep 11, 2019)

What happens when a major bank goes under and completely depletes the FDIC fund? (e.g. Bank of America)

Another key aspect of monetary metals is lack of counter party risk. When you deposit money with BoA, it is no longer yours; you become an unsecured creditor of the bank. BoA's derivatives counter parties are senior to you, so they will get paid first if say interest rate swaps go against BoA, and they need to post more collateral to that counter party.

Also, the problem with rates 'normalizing' is the magnitude of outstanding Treasury debt, and the fraction of GDP that the interest payments represent. 5% would be devastating, even though historically, that is a typical rate.

If you're not transacting for physical cash, isn't your money going directly into an account at another bank?

Unless people are withdrawing mass amounts of cash, I'm relatively certain you can't have bank runs against the banking system as a whole, you can only have runs against a particular bank.

The Fed and other central banks have almost total control over nominal inflation because they control the printing presses. They can create money by buying bonds and destroy it by selling them. They have bugger all control over real inflation but that’s a matter for the fiscal authorities to try and deal with by demand management.

“Inflation is always and everywhere a monetary phenomenon.” Milton Friedman

Edited to fix elementary mistake as pointed out by forkerenok

We've never had hyperinflation in the US. We've had high inflation, but never hyperinflation. And we've had very low inflation since the 80s, including during the decade-plus period of practically-zero interest rates.

Hyperinflation is a completely different issue from inflation, and it's kind of odd for it to become the monetarist bugaboo. When the US has a massive war debt payable immediately, or a complete economic collapse that the government decides to cope with by price controls, then you'll see hyperinflation. But then, hyperinflation will be the least of your problems.

Not technically the US, but the Confederacy did experience hyperinflation during the war. They ran the printing presses at full-tilt without anything tangible to back them up. And obviously once the tide of the war shifted things got real bad.

Also not technically the U.S, but during the Revolutionary War the continental dollar underwent hyperinflation, leading to the phrase "not worth a continental". By the end of the war they were worth less than 1% of face value and had ceased to circulate as money.

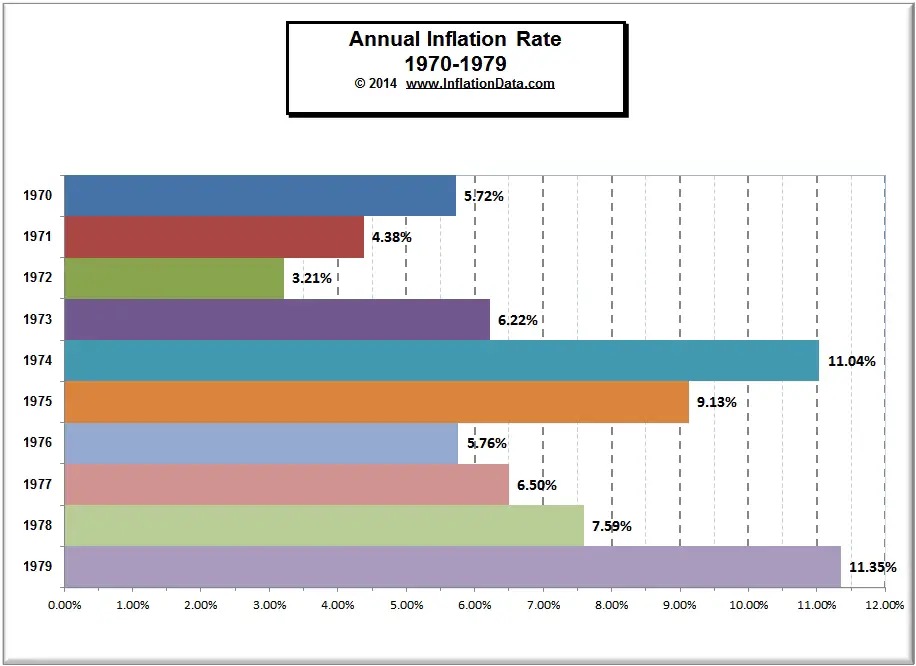

Well... the 1970s weren't a hyperinflation, but we were trending there. Inflation was not only high, it was increasing. Would we have wound up at hyperinflation if Volcker hadn't clamped down at the Fed? I don't know; that's alternate history. But it felt like we were headed there.

I'm sorry, but this is just wrong: inflation was high but fluctuated a lot and by no way you can say it was “increasing”. You're rewriting history in favor of your political bias.

I'm sorry, are you psychic? I didn't say anything about a political bias, nor anything to even hint at one. You're making up stuff that you think you know about me, with no basis.

To the data: I agree that there are fluctuations there. But average inflation for the decade of the 1960s was 2.45%. For the 1950s, it was 1.82%. The inflation rate even for 1972 was above the average rate for the 1950s and 1960s. 1976, the bottom of the next trough, was higher than 1972. And then you look at 1974 and 1979, in the context of the 1950s and 1960s, and yes, it sure does look like inflation is increasing. Yes, there are decreases (business cycle), but each cycle is higher than the last one.

First of all, inflation and hyperinflation are two really different things. The first one being common in history while the second one is rare but catastrophic.

Then, In Friedman's book inflation is related to the amount of money in circulation, yet since the 80s the amount of money and inflation have almost zero correlation in the US. Some of Friedman's concepts were useful to reach that point, but still: we now have been living for 40 years in a world where Friedman's model is unable to explain anything.

That's mostly true (except as another comment says, the "sell" and "buy" are backwards).

Certainly the central bank can create as much inflation as it wants, by simply printing and distributing more money (which usually takes the form of the central bank buying assets such as bonds with the new money). There's no limit to the ability of the central bank to make the currency valueless.

In the other direction, they can usually increase the value of money (ie, create deflation) by reducing the money supply, but it is possible that at some point the public might simply stop regarding the government's money as being worth anything. The only thing that might stop that is that people would still need government money to pay taxes.

Did you actually mean it the other way around as in they can create money by buying govt bonds/treasury bills/etc and retire them by selling them back to the market.

> The Fed and other central banks have almost total control over nominal inflation because they control the printing presses.

Not quite true. Every bank can print money (well, the modern day equivalent of increasing a digital number somewhere), and does so when they make loans.

{kind=link}

When the liquidity crunch is over, the Fed will start gradually increasing the rate. That will make rolling over existing overnight loans taken from the Fed less attractive and a lot of money will flow back to the Fed.

I hope people more familiar with the subject will correct me if I'm wrong.

[0]: https://www.coursera.org/learn/money-banking