I guess you're mostly right. From a 2014 point-of-view. Seed funding in 2014 was abnormally high. Amateur hour levels of high. 2015 didn't pulled back much from that. I think that the market is showing some prudence given that we could well see the apocalypse of the unicorns any day now.

The various data sources I have access to (CB Insights, et al), tell me that it's down, but not gone. The fact of this article (AngelList's rainy day fund) means that people are starting to prepare for stormy weather. A storm that has not hit yet - but people are skitterish.

Tactically, on the ground, I haven't seen much pull back, but I'm not in CA or NY. And I prefer to get cash-flow positive ASAP, so I might be a little less sensitive to it than others.

Thanks for your response: you raise interesting points (esp. your linked EU funding scene thread - that was interesting) and digging into this will provide some necessary weekend diversion.

I was not making a year-over-year relative statement. 2014 levels also were next to zero. (Every year is next to zero.) I am making a much wider statement.

I asked you to sum up all seed funding in existence: what number did you get? (This is the number that I call next to zero.) It doesn't matter what year you pick.

Since the rise of of on-demand data centers and software eating the world, Series A is the new Series B, and they expect some commercializable prototype (MVP) and customer traction before they'll talk to you.

So, even though Series A used to be called "Early stage" financing, I'm not sure it's fair to include it in what we used to call early stage any more.

So, to your question: sticking with angel/fund/corp seed, I don't know - maybe $10B or so in the US? You're right - that's pretty tiny. VC as an entire asset class is pretty tiny in the grand scheme of things (certainly very tiny for the amount of press it generates).

I'll take a look into the data this weekend, but I would guess that I'm in the ballpark of a binary order of magnitude with that guesstimate. Close enough to zero to make scrounging for it painful, I agree.

>Series A is the new Series B, and they expect some commercializable prototype (MVP) and customer traction before they'll talk to you

No, that's not even good enough. Even if you have a product in the market, with traction, if it's not millions of MAU/DAU then welp you're SOL. Doesn't matter what technology you built or how good your team is.

The only caveat to that is if you, as a founder, are already a known entity to the venture funds with a previous exit or in the right social network.

Well, my point was that while, yes, it's easier (cheaper, faster) to build and market a product than it was 20 years ago, the criteria for an investment has moved right along with it. I mean - gosh - Sun was funded based on a napkin drawing. (It was already developed paid-for Stanford-developed technology, though, so declaring it to have been funded simply off just a napkin is unfair)

Currently I have a thing that is kinda/sorta like a B2B SaaS play, with bottom-up engagement directly with the employees of the target enterprise -- and I've had to shut the doors to (unnecessary) investor interest w/ only about 3K active users.

But, underneath it all the distracting details, I agree. I think the general consensus in this thread is: it's hard.

So I would agree that $10B in seed funding is next to zero, and yes, that is my point, however I think you are overestimating it by a (decimal) order of magnitude, and that is worldwide. I think worldwide there was less than $1B in seed funding in any year. That should be easier to falsify if you can do so! I would be interested in your data sources or methodology if you succeed in showing this.

I will go see what I can see. As for a starting point, I'll probably dig around CB insights, pitchbook, angellist, and the Center for Venture Research at UNH (New Hampshire). Then go from there.

If you are right, that's a very very interesting result.

all right! Definitely please don't include series A but personally I'm not sure whether I should consider kickstarter and co to be seed rounds - maybe? I am very curious about what you find in the sources you've already mentioned (without including series A rounds), though, and hope you will give an update!

I hadn't even thought of including kickstarter-and-friends, partly because the companies aren't selling equity. I'm not including any sort of corporate spin-out either.

The lines have gotten so blurry compared to 20 years ago (entrepreneural creativity in action?), so sorting out the wheat and chaff is harder. More data - less definition.

The thread is deep (as you say in this comment's sibling), so I will email the longer commentary...

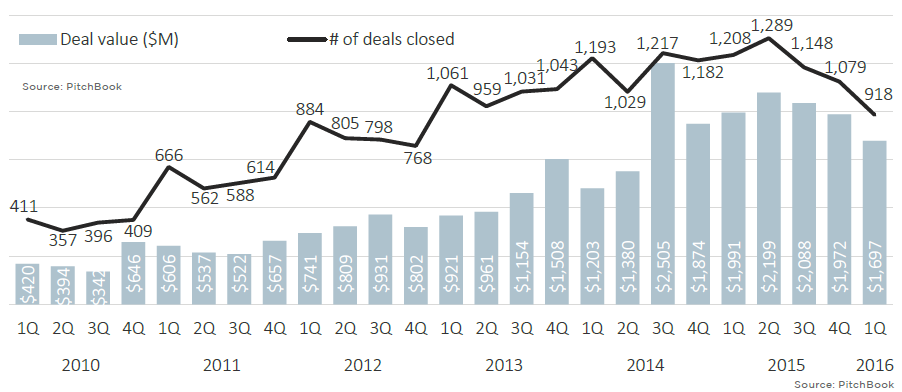

Briefly, most of the published analysis is top-down and less is bottom-up. People seem to bundle Seed+Series-A in most places. There's a lot of talk about medians without a deal-count. There are counts for numbers of deals with a size exceeding some threshold, but that doesn't give us what we're looking for.

{kind=link}

The various data sources I have access to (CB Insights, et al), tell me that it's down, but not gone. The fact of this article (AngelList's rainy day fund) means that people are starting to prepare for stormy weather. A storm that has not hit yet - but people are skitterish.

Tactically, on the ground, I haven't seen much pull back, but I'm not in CA or NY. And I prefer to get cash-flow positive ASAP, so I might be a little less sensitive to it than others.

Thanks for your response: you raise interesting points (esp. your linked EU funding scene thread - that was interesting) and digging into this will provide some necessary weekend diversion.