> Investors can buy a share of the fund, called the Access Fund, for $100,000 or more.

This is really interesting to me, but I wish it were at a $10k level. That would be a no-brainer shift for me to move some money going into Vanguard into this, but I'm in that weird spot where I'm not rich enough to have $100k to toss around but am maxing out a Roth IRA and looking for more upside.

Agreed; we do this for regulatory reasons. We've got a limit on how many investors we can have per fund, and we can't sidestep that requirement by spinning up duplicate funds.

The high minimum investment is our equivalent of surge pricing.

No issues with that on our end. Plenty of investors using funds or LLCs with multiple members to invest.

You'll want to work with a lawyer to structure the vehicle, and have a full understanding of legal, compliance and tax considerations associated with it.

Edit: the entity investing must be accredited. Here's an overview of the criteria:

Accredited investors only? If so, even lowering the floor to $10k might not help the OP (geared toward helping swanson with the details rather than any kind of suggestion).

How are you guys assessing the lookthrough in that case? If an entity is formed for the sole purpose of investing in your fund, I believe those investors count towards your limit.

Are you seeing any regulatory openings here? We (www.agfunder.com) think that indexing is a much better approach for individual investors looking to get some exposure to an asset class like venture.

Be careful to examine what's actually in the fund as your underlying. This isn't like buying the S&P500 where the sector exposure is well defined. One "startup index fund" can perform very disparately from another "startup index fund".

edit: If there's data that shows the performance of a basket of random 100 company samples being equivalent to any number of other random 100 company samples, then I am happy to admit that I am mistaken in this regard.

Yep -- I understand what I'm buying (well, not buying yet...). Something like this would be a great for a Taleb-esque 90/10 barbell I think -- 90% in target-date vanguard funds and 10% in startup investments by proxy.

Didn't Taleb advocate cash holdings (90%) and high risk investing (10%). I always though that 90% cash was a pretty whacky idea and personally just stick to portfolio theory.

I think your plan (substitution index funds for cash) is already a lot better than what Taleb suggested.

The Central Limit Theorem needs the prerequisite that your distribution has a finite variance. It's not at all clear that this holds for the return of startup investments. In more practical terms, when the variance is very high or there are outsized impacts from small portions of your population, it can take arbitrarily many samples before your average starts to converge. So it's entirely possible that sampling 100 companies isn't enough.

Statistically the central limit theorem is assuming sampling from the same population, there is no guarantee that two startup indexes are actually sampling from the same population

Lots of conditions that may not be satisfied. Independence is a very hard one. results may be well correlated even if they look like they should be independent

It is. All a backdoor Roth does is it gets around the income limits for Roth IRAs. If you make more than ~$130K per year, you aren't allowed to contribute.

With a backdoor Roth, you contribute to a normal, post tax IRA, then convert to Roth. However, if you have a rollover IRA, then you can't do it without taking a tax hit.

However, I have heard of people putting more than $5500 per year in a Roth. Search for it on the Bogleheads forum. I can't remember the details, but your employer needs to be on board as you contribute to a 401k, then do some conversion.

The fund invests in a subset of syndicated deals. About half of them historically. The investment team consists of experienced investors including Naval (my co-founder). Details here https://angel.co/access-fund

That's a nice advantage you have going -- normally access to the best deals is hard to come by, but by providing the tools by which stand out individuals can achieve leverage in their own deal making through syndication (you're both a technology provider and a channel marketing partner to them), you get their deal flow in return.

The best funds and GPs seem to consistently talk down their unrealized gains as paper gains that need to be steeply discounted. They cast doubt onto themselves willingly, preaching instead to look at cash on cash returns.

The boom/bust assumption undergirding this Bloomberg article is belied by what AL is itself doing –– creating instruments that allow the private tech capital market to expand and contract in a fashion that is smoother and less stepwise.

Hey, I got an HN Replies email before you changed it from $500 to $200... :)

Just kidding. Ok, let's do this. $200 it is, but you have to pick your charity now, and the timeframe for a return has to be sufficiently short such that $200 can still at least buy a mosquito net or something.

My charity choice is the US Treasury.

Also, HN is fine (my real name / twitter / github are in my profile).

P.S. You didn't ask why I thought it wouldn't return a profit. It's not because I disbelieve in your company (you guys have more startup data than just about anyone).

this is absolutely ridiculous. there is next to no seed funding in existence. Let me tell you how the seed market for startups is: imagine you had a orchard, right, but instead of apples it grew dollar bills, and you just had to water them or they wouldn't grow. Under this scenario a guy with acres of dollar-tree bills could not get funding to water them with some kind of farm equipment. That's the state of the startup world.

You read all those PG essays about not dying? About bootstrapping? Well because it turns out the only way to capitalize a typical startup is to stand in front of your dollar-bill tree and urinate. Or organize some kind of free sporting event with the side effect of making people go piss on your trees. Then 97% of your trees die except the 5 you pissed on, but you can take them to the bank and next season repeat. That's how bad startup seed funding is.

You could not literally fund money growing out of thin air.

I sometimes think that the government should step in and fund these things (after all, even Tesla got gov't grants.) Because the private market sure as #@$% isn't.

EDIT:

This is already at -2 but I am keeping it without altering a word, because the downvoters are wrong and uninformed (or don't understand the analogy), and I am right and well-informed, also it's a good analogy. It's not even close. Here is an example of someone in Europe describing this precisely:

Notice the words "With a product like that, the second thing that we didn't expect was that we tripped the "too good to be true" sensor everywhere, raising doubts." (you might have to click parent from the comment I linked.)

It's not as bad in silicon valley as it is in Europe. But it's not that far-off either. There is next to no seed funding in existence. This is a fact. Downvoting me won't change it. Now at -3 after posting this update. Still right. Still not changing a word.

Your claim is ... what exactly? I'm not disagreeing - I'm just not following. That revenue is hard to come by for startups? That seed money for revenue-less company is getting more difficult for startups to raise? If so, where? In the US? In California? In Europe?

I've never dealt with any structured seed funds, but high net worth individuals that like to kick-start startups still appear to be active in the US...

>Your claim is ... what exactly?... That seed money for revenue-less company is getting more difficult for startups to raise?

That there is next to no seed money in existence, for companies, regardless of whether they are making money, and anywhere in the world (including California which by a large margin has the best funding climate for seed rounds.) That if you sum up the total amount of seed money it is next to nothing.

As an exercise you could try to add up the sum total yourself, and you will see it is next to nothing.

I guess you're mostly right. From a 2014 point-of-view. Seed funding in 2014 was abnormally high. Amateur hour levels of high. 2015 didn't pulled back much from that. I think that the market is showing some prudence given that we could well see the apocalypse of the unicorns any day now.

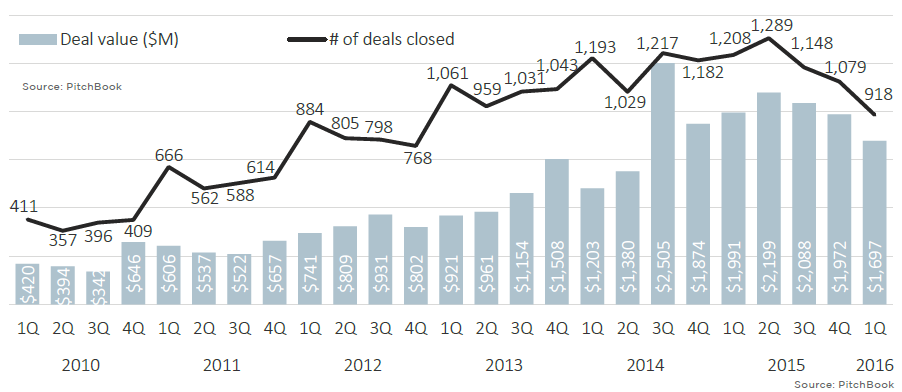

The various data sources I have access to (CB Insights, et al), tell me that it's down, but not gone. The fact of this article (AngelList's rainy day fund) means that people are starting to prepare for stormy weather. A storm that has not hit yet - but people are skitterish.

Tactically, on the ground, I haven't seen much pull back, but I'm not in CA or NY. And I prefer to get cash-flow positive ASAP, so I might be a little less sensitive to it than others.

Thanks for your response: you raise interesting points (esp. your linked EU funding scene thread - that was interesting) and digging into this will provide some necessary weekend diversion.

I was not making a year-over-year relative statement. 2014 levels also were next to zero. (Every year is next to zero.) I am making a much wider statement.

I asked you to sum up all seed funding in existence: what number did you get? (This is the number that I call next to zero.) It doesn't matter what year you pick.

Since the rise of of on-demand data centers and software eating the world, Series A is the new Series B, and they expect some commercializable prototype (MVP) and customer traction before they'll talk to you.

So, even though Series A used to be called "Early stage" financing, I'm not sure it's fair to include it in what we used to call early stage any more.

So, to your question: sticking with angel/fund/corp seed, I don't know - maybe $10B or so in the US? You're right - that's pretty tiny. VC as an entire asset class is pretty tiny in the grand scheme of things (certainly very tiny for the amount of press it generates).

I'll take a look into the data this weekend, but I would guess that I'm in the ballpark of a binary order of magnitude with that guesstimate. Close enough to zero to make scrounging for it painful, I agree.

>Series A is the new Series B, and they expect some commercializable prototype (MVP) and customer traction before they'll talk to you

No, that's not even good enough. Even if you have a product in the market, with traction, if it's not millions of MAU/DAU then welp you're SOL. Doesn't matter what technology you built or how good your team is.

The only caveat to that is if you, as a founder, are already a known entity to the venture funds with a previous exit or in the right social network.

Well, my point was that while, yes, it's easier (cheaper, faster) to build and market a product than it was 20 years ago, the criteria for an investment has moved right along with it. I mean - gosh - Sun was funded based on a napkin drawing. (It was already developed paid-for Stanford-developed technology, though, so declaring it to have been funded simply off just a napkin is unfair)

Currently I have a thing that is kinda/sorta like a B2B SaaS play, with bottom-up engagement directly with the employees of the target enterprise -- and I've had to shut the doors to (unnecessary) investor interest w/ only about 3K active users.

But, underneath it all the distracting details, I agree. I think the general consensus in this thread is: it's hard.

So I would agree that $10B in seed funding is next to zero, and yes, that is my point, however I think you are overestimating it by a (decimal) order of magnitude, and that is worldwide. I think worldwide there was less than $1B in seed funding in any year. That should be easier to falsify if you can do so! I would be interested in your data sources or methodology if you succeed in showing this.

I will go see what I can see. As for a starting point, I'll probably dig around CB insights, pitchbook, angellist, and the Center for Venture Research at UNH (New Hampshire). Then go from there.

If you are right, that's a very very interesting result.

all right! Definitely please don't include series A but personally I'm not sure whether I should consider kickstarter and co to be seed rounds - maybe? I am very curious about what you find in the sources you've already mentioned (without including series A rounds), though, and hope you will give an update!

I hadn't even thought of including kickstarter-and-friends, partly because the companies aren't selling equity. I'm not including any sort of corporate spin-out either.

The lines have gotten so blurry compared to 20 years ago (entrepreneural creativity in action?), so sorting out the wheat and chaff is harder. More data - less definition.

The thread is deep (as you say in this comment's sibling), so I will email the longer commentary...

Briefly, most of the published analysis is top-down and less is bottom-up. People seem to bundle Seed+Series-A in most places. There's a lot of talk about medians without a deal-count. There are counts for numbers of deals with a size exceeding some threshold, but that doesn't give us what we're looking for.

You're not entitled to seed funding. However the government does offer SBIR grants of ~225k, from all branches of the government, DOJ, NIH, NSF etc. Odds of getting the grant range from 1/5 to 1/12 depending on the year. With solicitations twice a year.

so if you total the value of all of those grants combined (regardless of the "odds" of getting them) it's next to nothing in existence. it's really, really small when compared with the value under my analogy of the money-sprouting trees that those founders ('farmers') are asking to water (which obviously is the value of the resulting companies when successful). if you do know the sum of all of those grants combined it would be interesting to know that number.

I feel like AngelList is a specialized social network with maximum utility ~10 years ago and for people who already know each other or are clearly in the same network, who basically use it as a less-spammy LinkedIn. I've had zero luck communicating with people over it and have frankly given up in favor of raising domestically here in China.

"less-spammy" is not how I would describe AngelList. Unfortunately, if you, as a user, allow it to access your email addressbook, it then starts regularly (days apart) spamming each address.

I'm currently working on a company that could just as easily start in China as the US: anything you can share regarding where and how to find investors? No "Chinese AngelList"?

There are many local networks. We are currently in touch with a few, and may even start one as an adjunct to the current round's raising process. I've sent you an email.

> Meanwhile, AngelList is adding new ways for people to get into private-company investing. With some 600 startups expected to raise money through the website next year, AngelList said it’s creating a sort of index fund for young companies that will hold shares in 100 to 200 startups. Investors can buy a share of the fund, called the Access Fund, for $100,000 or more.

This could be interesting. I wonder if it will be restricted to accredited investors or offered to the layman?

As always, of course there are no guarantees in startup returns, but spread over that many companies... well, I'm not sure what to expect. I guess it all depends on the returns and how they decide to pick companies. It could be a cool new take on index investing. Then again, I became wary of most things "cool" and "new" in investing.

You'd need to register the securities with the SEC if your're oing after non-accredited investors. I wonder if Angellist is going to go through that trouble.

One big advantage of only having accredited investors is that it allows you to not have to make such regulatory filings.

I have a startup and want to raise money. It just feels like listing on Angellist won't do anything, and I'm better off doing "offline" (emails) traditional way of raising. It just feels like good deals are done through emails and meetings not through a portal. At least for now

Angel List the site is fine, but they really need some sort of verification or moderation. When I was looking for an internship there were a bunch of sketchy non-companies willing to pay me... $0. After I graduated it was easier to find real companies, but then it's just the same as other job sites with companies that get back to you months after applying. The design and look of the site comes off as more professional or trustable than other places, but it's not curated. At least force people to be honest about a lack of pay.

With of all that said... two of the three jobs I've held were found there.

Welcome to the world of software development, where you get wonderful 'offers' like:

1.) I have an idea to build the $hot_startup of $sketchy_vertical. Just sign this NDA, build the whole thing for me and I'll give you 0.01%. It will be huge!!

2.) I have an idea and I'm this close to raising a sees round from $famous_investor. I just need you to build a simple (fully functional) proof of concept. I'll give you a great job after I raise the cash.

3.) Can't you just build this? It should be easy for you...

Nope. Like I said, I was actually successful with Angel List—you just have to have a good profile and either write good introductions or contact the company directly. It could just use a cleanup and moderation.

I guess you're right. The internship search was bad, but the job search was okay. The two jobs I found replied quickly, were professional, and provided good offers. You're probably right in that I got used to companies not replying for months, so I'll keep a recruiting agency open as an option next time.

{kind=link}

This is really interesting to me, but I wish it were at a $10k level. That would be a no-brainer shift for me to move some money going into Vanguard into this, but I'm in that weird spot where I'm not rich enough to have $100k to toss around but am maxing out a Roth IRA and looking for more upside.