This is only true for a federally backed mortgage. Yes, down payment levels, in the context of whether someone needs mortgage insurance, is set by regulation. But down payments can be much less significant if you’re ok with mortgage insurance. Down payments required by banks were typically higher before regulation.

Before regulation it really depended on the buyer. Some people where putting down 5% without insurance, others had much stricter requirements.

We’ve settled on a really arbitrary system where for example the Federal Housing Administration requires huge upfront FHA insurance payments without regard for down payment size if it’s less than 20%. If you’ve saved up say a 8% down payment you really should be a significantly lower risk than someone putting down 3.5%.

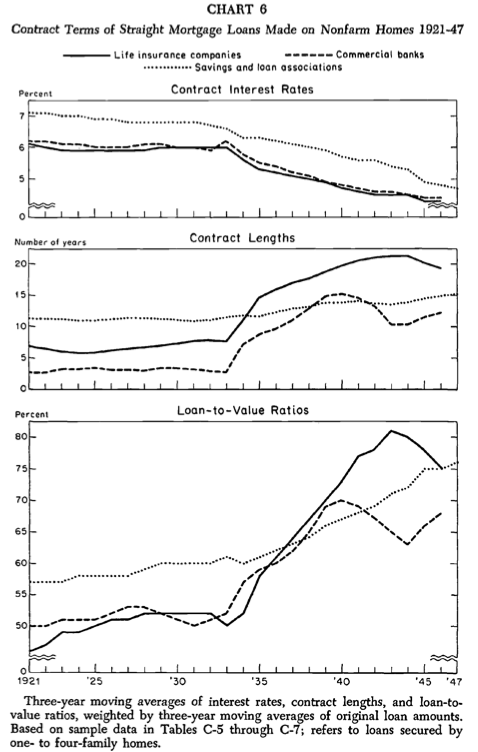

The buyer wasnt the decider. The bank was because they were the one taking the risk. The down payment required by banks before regulation was often 30% or more. That’s partly why home ownership was much lower prior to WW2.

I suspect we’re looking at this through different temporal lenses. When I talk about regulation, I mean the last 100 years in its entirety, not just since the financial crisis of 2008. I agree with some of your point regarding how thresholds are set arbitrarily, though.

> The down payment required by banks before regulation was often 30% or more.

I am talking about lending before regulation. High down payments were not universally applied, so yes sometimes a loan might require 40% but other borrowers might offer nothing. My point is you can’t simply say the required amounts were excessively high some of the time because they weren’t universal and selected based on a perception of risk.

{kind=link}