As a curiosity, how many people in this thread are home buyers that sat on the sidelines over the past year or two and are now waiting for prices to drop?

I’m in that camp and I’m starting to suspect there are enough people in that camp that any noticeable drop in prices will be immediately met by strong demand, even at current rates.

Since you cannot predict the future I recommend not waiting “for prices to drop”.

Instead, buy a house when you find one you love and that you can afford. Houses are not widgets- each have pluses and minuses and optimizing for price won’t make you happy.

If somebody bought early this year, they may be trapped in their home with negative equity for a decade, like many were after 2008.

Your advice is mostly sound, but buying in a bubble can have severe and very real ramifications on you, even if you can afford the monthly payment. You may not be able to move without writing the bank a large check, and many won’t have the cash on hand

You seem to be looking at buying a house as an investment. I'd argue otherwise: your first piece of real estate is a necessity, not an investment - you always need a place to live. So, in financial terms, you're closing a short position, not opening a long position.

Of course there is non-negligible friction if you need to move, so you do want to be mindful of not buying right at the peak, but in general I think you're overstating how much you need to worry about prices: you don't profit when prices go up, since you'd also have to pay more for a new place, and as long as you can afford the payments, your home moves in line with the market and don't need to sell, you also don't need to let falling prices affect your sleep. Your position is market neutral, you are mostly giving up flexibility.

While I think you're right in ordinary times, this doesn't work during a bubble. You could be totally blocked from moving if your home is worth a fraction what you owe on it, no matter how necessary the move is (job, school district, family).

Even then there are some mitigants: you could try to rent out your first home and rent or even buy a new one. Tax-wise that would work against you (usually, in most places), but it probably wouldn't bankrupt you.

I agree, of course you don't want to have bought right before a dip. But if you sketch out a few scenarios and look at the overall and your individual situation (eg, Would rental income cover credit payments, even in an adverse scenario? Do you have expenses you could claim in years when you're renting out? Do you have other uses for the property, eg within a family?), you might find that you can manage the risk (or not). It's definitely not risk-free, but there's also significant upside potential if you can make a long-term commitment.

He might be thinking of people in the US who are not in Alaska, Arizona, California, Connecticut, Idaho, Minnesota, North Carolina, North Dakota, Oregon, Texas, Utah or Washington.

In those states first mortgages are "non-recourse" loans. What that means is that if the borrower does not pay off the loan the lender's remedy is limited to whatever they can get foreclosing and then selling the house.

With a non-recourse loan if I find myself owing a lot more on my mortgage than my house is worth I've got the option of just walking away and letting the lender foreclose. I will no longer have a house after that, but my possessions and savings and investments and income will be safe.

In the other states first mortgages might be "recourse" loans. With those if selling the house isn't enough to pay off the loan they can come after you personally for the difference.

With a recourse loan the lender can come after me for the shortfall if the foreclosure sale isn't enough to pay off the loan. They might go after my possessions, saving, investments, and income.

Most people are putting down 20%. Even if you have a non-recourse loan that's a huge loss. Plus the hit to credit record means you probably won't be able to take out a new mortgage for years.

It'd only be a tiny percent of people who found themselves underwater, but with so little equity they didn't care to lose it, and who also didn't care about tanking their credit score for the next decade.

> You seem to be looking at buying a house as an investment. I'd argue otherwise: your first piece of real estate is a necessity, not an investment - you always need a place to live.

You need housing, but you can get that without home ownership.

I wish it was that clear cut. Here in Australia there is an acute shortage of rentals and rents are going through the roof [0]. As with everything, there is always a caveat.

Usually you cannot, but the fed has expressly told us they will be raising interest rates. They could be lying, but I think this is one of the few times you can "predict the future" and expect rising interest rates to influence demand.

But long term treasury yields are now lower than short term treasury yields. This indicates that the market expects inflation and interest rates to drop in the future. As long as this is true, prices for houses will not go down as everyone assumes that a refi will be possible in 1-2 years. Housing market will be stuck while this sorts itself out.

You can’t refi with negative or low equity, as most who bought in the last year are likely to have.

If inflation does come down rapidly, it’s likely to be coupled with a sharp increase in unemployment.

Rates fell significantly from 2005 to 2012, yet housing continued to fall. Whether lower rates or higher unemployment is the stronger force this time remains to be seen.

Given housing is by far at a historical peak in real terms, I suspect a reversion to the mean in real prices is more likely than not

> This indicates that the market expects inflation and interest rates to drop in the future.

It indicates that the market thinks the Fed will be effective. It's also (generally) indicative that a recession is on the horizon. We're starting to see the layoffs in certain sectors (tech especially). Unemployment rising tends to cause more mortgage defaults which will tend to lower home prices.

> As long as this is true, prices for houses will not go down as everyone assumes that a refi will be possible in 1-2 years.

A lot of potential buyers don't qualify at current (and rising) rates. They've been taken out of the market entirely. Wells Fargo saying that applications for new mortgages are down 90%. Assuming that's happening industrywide (no reason to doubt that) it's going to start effecting prices - and already is in some markets.

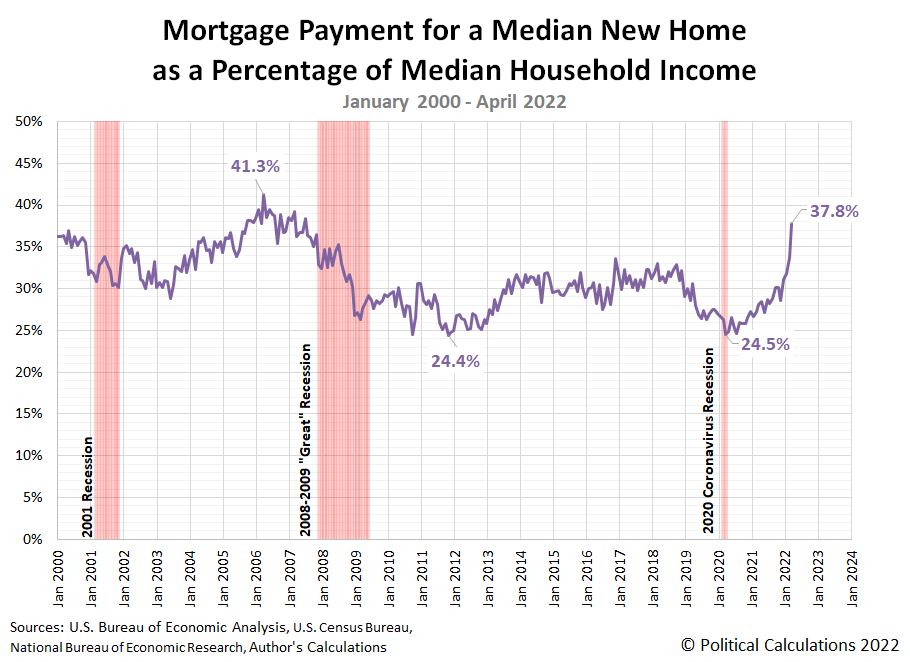

This is the chart I am referring to concerning mortgage payments, which IMO have remained within 10 percentage points of where they've been since 2000:

There is a sharper rise now of higher payments, but historically its not even where it was in 2006 and still is lower than figures not seen in this present chart, like the the 1980s.

In the end home prices don't march up in a vacuum, the money has to come from somewhere. People pay these prices and they can do so because they are skilled workers who are paid such incomes to afford homes in the Bay area or Boston or other high cost of living areas. It's not all private equity. When you add more high income jobs to an area than units of housing for decades, a housing crisis for the working class is the natural result, but for high income earners they will always be paid enough to afford the median mortgage payment or else the median will shift accordingly to meet the market where it is.

> Since you cannot predict the future I recommend not waiting “for prices to drop”.

This is questionable advice, and biased I guess.

It's quite easy to review historical sale data and see if a person is buying at a peak price. No it likely won't be the only or final peak, but it's a useful indicator.

> optimizing for price won’t make you happy.

On the other hand, not optimizing for price can make you significantly unhappy. Being immobilized due to an upside down mortgage, and stretching monthly finances can be really stressful.

The problem for us is the inventory has completely dried up. Our market has a lot of second homes. People who wanted to cash out already have. The people who weren't ready to sell, seem to be willing to "wait it out".

In the long run, it doesn't _really_ matter. We're well within our budget and plan to be in this home for a very, very long time.

The people that aren't selling are still paying upkeep and property taxes. Unless they live in it, they will tire of the financial bleeding eventually and start to understand the "sunk cost fallacy."

Correct. However, second homes are a bit different. They don't get used as often and the financial bleeding is viewed different. They're also in a market where AirBnB/VRBO is extremely lucrative. If you can tolerate a bit of pain from renting it out, there's really no finanicial bleeding.

Anecdotally, Airbnb rentals are a lot less profitable now. An informal and definitely biased survey of friends I know who run 1-4 units: price drops of about 40% are happening, and they have significantly fewer inquiries.

I predict that will continue as potential guests tighten their belts. And as more 2nd homes are a drag on their owners cash flow, there will be more people listing on ABNB to make some cash. That will cause a glut of supply and further drive down prices.

Airbnb was benefitted me many times as a resident when the renter protections in my city made renting difficult. Renting an airbnb allowed my landlord to bypass renter protections which made it very low friction to use airbnb whereas signig a lease was nigh impossible because landlords wanted all kinds of evidence I'd be a good renter as it was so hard to kick a renter out.

By using Airbnb, I was able to continue living and working in the city by ceding away my rental protections in exchange for not needing good credit and other assurances for the landlord. Win-win.

> any noticeable drop in prices will be immediately met by strong demand, even at current rates

As long as people are okay with buying insanely overpriced homes they will not fall.

But careful, you might be fired too. Or lending may be even higher later (forcing lower prices). Or rates will be high be many years. Or you'll go underwater and not be able to refinance. Or your taxes will also go up. Or maybe you need to move/divorce. Or maybe you die and your next-of-kin can't pay the house and be foreclosured. Or maybe you can dump the cash in bonds/stocks and make more money. You may have more kids and need to move to a bigger house and be forced to sell at a loss.

As a curiosity, how many people in this thread are home buyers that sat on the sidelines over the past year or two and are now waiting for prices to drop?

Waiting for a price drop doesn't really work.

Firstly, when prices start to drop people stop selling. You might want a cheaper house but the supply will be severely limited so you probably won't get what you really want.

Secondly, when prices drop it usually comes with other changes in the market. Mortgage lenders are weirdly skittish at the moment, and they stop lending the instant anything looks bad. If you need a high loan-to-value mortgage (eg 90% of the purchase price) you probably won't get it in a downturn.

I bought a place about 18 months ago and got a 5 year fixed interest mortgage because I figured we're going into a period of inflation and maybe recession so interest rates will probably go up. My timing was off a bit but it's going to save me a fortune over the next few years (and then I get a huge shock when the fix rate ends... yay!)

> Firstly, when prices start to drop people stop selling.

Most people who sell their home also buy a new one at the same time. So if those folks remove themselves from the market, it doesn't really change anything as they are decreasing both the supply and demand by an equal amount.

The net balance in supply and demand comes from first time buyers, investors (both buying and selling), immigration vs emigration, and the elderly (moving to care facilities or passing away). Investors have significantly reduced purchases, and as economic conditions deteriorate I expect them to start selling (for example a lot of AirBNB hosts bought at the top of the market and are starting to get nervous as bookings are declining).

Basically, you can have a market with record low inventory and still see significant price decreases if demand is also low. The fact that we have record high employment and inflation and we are still seeing prices either level off or decline is very concerning. If employment starts declining we are certainly going to see a lot more selling pressure.

It won’t. Real estate is on track for at least 20% crash from here. People with 3% rates don’t want to sell and move to 7%. So, they are renting out at loss and therefore renting is becoming amazingly cheaper compared to buying. This further reduces demand and increases supply and it’s a classic recursive cycle that will only accelerate as rates will go up even more for next 6 months. My advice would be to rent house of your dream for next year while housing crashes. The best time for buying would be when interest rate hits below 4%.

Why would renting become cheaper? Most people have told me that there will be less people buying so more are renting, therefore rental prices go up. Right?

The number of households artificially increased as a result of student loan payment deferments and the general COVID free money bonanza. More households = more rental demand = higher rent.

Expect that to revert to the mean (people move back in with their parents, get roommates) if this is a long, deep recession. Less demand = lower prices.

I am in that camp as well. But... my rent is less than half the cost of a mortgage (including taxes and insurance) for a similar place. And this doesn't even account for maintenance costs. My landlord prefers long term tenants, so has shown no interest in raising our rent, and even if they did we are under rent control which will limit the damage. And while we are definitely paying under market rent, it is not by that much. So I feel fairly confident we can find something similar on short notice, and with more time could probably find a really good deal.

So after years of holding our down payment money in low interest savings accounts, I am now moving it into CDs and bonds that have nice returns which will result in a nice chunk of change. And if prices don't come down anytime soon, I am more than happy to keep renting. I think prices would need to drop by almost 40% before I would really consider buying at this point.

For context, I am in the Bay Area so it might be a somewhat unique situation to our market. But in the four years that I have been renting at this particular location, rents have not really moved much while house prices are up 50%.

I think I'd do what your landlord is doing if I were in that position.

Having a long term reliable renter, which I'm sure you are, give them a rent that is a good deal (slightly below market), and they'll stay. Even if your rent doesn't cover mortgage and expenses, eventually you or other renters are going to buy the property for your landlord, and that's worth a lot.

Especially if home prices are up 50% - keeping your rent stable and you there paying it means your landlord is getting a spectacular deal.

Agreed. It is worth mentioning that in CA my landlord is benefiting greatly from Prop 13. They bought the house a long time ago, it is almost certainly paid off by now. And due to prop 13 they have locked in absurdly low property taxes. This is a big quirk to the CA rental market. Anyone buying a property now in order to rent it out is going to see significant negative cash flow. I think AirBNB renters can squeak out a positive cashflow, but they better hope bookings don't dry up.

Unfortunately CDs and bonds rates are way below inflation, so you are going to lose money if you don't buy assets. I am in similar situation and don't know what to do.

Inflation is trending down and there are plenty of long term CDs and bonds with decent rates that will almost certainly mature long after this current inflationary period comes to pass. The Fed has given strong signals that they intend to tackle inflation regardless of the cost. So locking a 10+ year CD or bond at current rates is almost certainly going to beat inflation in the long term. Also FWIW, I do expect rates to continue to rise for a few more months, so I am keeping plenty gradually rolling my savings into these investments.

Turns out “cash on the sidelines” disappears quite fast when assets broadly devalue.

Housing is correcting faster than GFC, though it remains to be seen if it ends up deeper. But when it falls at this pace, people start to get cold feet

But the mortgage payment is in the process of skyrocketing. Even if home values drop, the majority of people are going to have less ability to buy a house as more of that money will go to the bank.

That rewards savers. It also means savers end up saving more money, as higher interest rates reduce demand for loans creating downward pressure on the real estate market.

The spenders of what they didn't have got rewarded for long enough.

Even when I was a forklift driver, a job available in practically every middle-sized low COL midwest city, I could save $10k a year by only spending on necessities. That's only like 15 years to buy a house somewhere like a middle-sized Midwest town with forklift jobs. Not too shabby if you can buy a house by 33.

The piggy-bank method does work. Maybe more people should be doing it rather than us having a system inflating the hell out of our economy through loans with negative real interest rate.

I just Googled it and the average forklift driver salary is $40k. After tax and retirement you’re taking home around $2500/mo. After putting $1200 in your piggy bank you’re left with $1300 to pay for rent, food, gas, car, phone. I seriously do not think that is possible, let alone pleasant.

There's a certain segment of people with a smug self superiority that think because they earn six figures in places like Seattle or San Francisco that the simple forklift driver in bumfuck, WI has even less chance of buying a home than they have.

They couldn't be more wrong.

While the forklift driver is slowly saving 10k a year for a 150k house, the SF bro is saving 50k a year for a similar house for $1M. Guess who gets to the target first.

Nowadays one can also work remotely for an SF/Seattle firm and live in Appleton & buy a very nice house & talk about Bucks games at the bar rather than website capitalism.

Or have room mates for a few years, and then move in with a partner and split the rent on a cheap 1 bed. It's doable without being miserable, most of the country lives like that.

Of course, one may choose to work harder than average to make more than the average.

> I seriously do not think that is possible

Rents can be very low in these kinds of places, especially if you're young and willing to share a house with others. I personally knew a couple who spent less than $20k a year on all household expenses; granted it was a few years ago, but they weren't even in a very low CoL area.

Productivity is output per unit of time worked. More productivity is getting more out of the same amount of work. AFAIK median hourly wages have been flat or better per unit time worked, thus working more would indeed mean more pay.

What is a midwestern forklift driver giving up when they buy the 150k house? Just a few years ago I was raising a family in HALF of a duplex that was worth 80k. My kid had their own room, a nice big yard to play in, close proximity to parks and outdoors, water electricity and internet for kids shows or whatever. Are you saying I was depriving my family of something huge that I otherwise could have provided them?

The downvoters are being pedantic. Sure you could save 400k in cash with thrift and gumption, but the simple fact is that almost no one does, and certainly not enough people to soak up all the excess housing stock as rates continue to rise. A person could save that, but people do not.

>I’m in that camp and I’m starting to suspect there are enough people in that camp that any noticeable drop in prices will be immediately met by strong demand, even at current rates.

Same. I dropped out of the market last year after refusing to take part in the insanity. No, I am not going to waive all contingencies, give you 5% earnest, and bid over appraisal, for the hope of having my offer selected. Hopefully this will change with the corporate money drying up.

The price of a home is what people that want to live in the area are willing to pay per month (important detail!) to live there. This is made up of the principal, the interest, and property taxes. As interest rates fell more and more, the interest part of the monthly payment went lower and the principal part went higher. Coupled with inflation, we saw dramatic rises in prices.

Interest rates are going up so we'd expect to see prices go down, and they likely will in some markets. However, we are also seeing inventory dry up since who wants to sell their house and get a new mortgage at a massively higher rate?

With a low interest rate and inflationary pressures, current home owners are living for free. They can leverage this as well as their appraisals have all shot up.

I've made this comment before but you can correctly time a downturn and still end up worse off than people who buy at the height of the market. You lose upside, low interest rates, and continue paying rent (which has zero return). It depends on how long you can hold out during a bear market and what exactly interest rates do.

Plus there's the quality of life factor if the home you purchase is a better fit for your life... spending 10 years in a home you don't enjoy has a mental cost to it.

FWIW we borrowed $2m at 2.5% (thanks Bay Area prices!)

Thanks to that low rate even if the house drops in value by 30-40% we still come out ahead on the mortgage cost assuming we stay in the house. And it is likely any money not spent on the down payment or paying it off early can be invested which thanks to the current market and interest rates can take a risk to get a good return (stocks are discounted right now) OR easily find safe investments that exceed the mortgage APR.

Plus we have a house that fits our family way better with a lot more space. We also have knock-on effects (installed Solar with a <5 year payback, something renters can't do).

It is hard to imagine a scenario where waiting out this downturn would have worked out better for us.

That's why it is just one possibility. I usually only ever see people patting themselves on the back after the Nth time they're finally "proven right" about housing being over-valued. My point is just that you can be right about housing (or the stock market), make well-timed correct decisions, and still end up losing compared to the supposed "chump" who just went with the market. It all depends on your exact situation, exact market conditions, etc.

My guess is most people doing the back-patting have never run the numbers on an adverse scenario. They just see the top-line number dip and say "see, I was correct to wait!"

tl;dr: Run the numbers comprehensively for several scenarios. Include gains you missed out on, rates moving against you, your time horizon, risk appetite, etc. It isn't theoretical, real people have lost real money by being correct about a downturn.

We bought at pretty much the rock bottom of 2020/2021 interest rates (nothing like wiring away your hard earned money on the very same day when the US capitol was being overrun and the government seemed just about to topple…)

We had to work hard to avoid areas in SF that had been overbid. We didn’t find a bargain but we found a good deal, something that the prior owners needed to let go off but which wasn’t in a super popular area. This was in a hot market. So I think in the coming market you will find good opportunities.

So, as I obsess over listings today pondering if there might be an opportunity… I think that there will be good deals to be had, but not necessarily steals. In the Bay Area, people trip over themselves to live in a few neighborhoods so I think prices in those highly sought after areas won’t reach absolute bargain levels.

But If you are prepared and ready to step in you can already find properties that I think are marked down.

I’ve been watching closely dreaming of a place for our parents, or maybe more space for us, or maybe a rental…

Ultimately you have to live somewhere and people don’t choose to live in the cheapest place “in the country at any point in time.”

At the time we bought we found a house that gave us more space than the apartment we rented previously and where our newly arrived daughter could spend her first few years. It’s not one of the trendy neighborhoods and yet it’s close to downtown SF and the peninsula, where we work. We can afford it on one income. All those factors made it a good deal for us. I feel ok about it so far, but I’m certainly open to the possibility that there are better options.

I have not found that to be true unless you are looking for a standalone single family home. If you are looking at condos, SF has had good deals during the pandemic as that particular market segment has been hammered.

Almost bought a second home a year ago to get out of (and sell) our starter home. Was looking at houses with a realtor, a few new constructions, etc. Both glad and not glad we didn't buy at the time.

Glad because everything is likely to crash at this point and we would certainly have an underwater mortgage, but not glad because with the more than doubled mortgage rate since we were looking, it'd be stupid to sell our current home and upgrade now (especially with prices still high), so now we feel stuck (granted, stuck in a home with a fairly cheap mortgage payment, so it could be worse, but stuck nonethless).

We also held off on refinancing during the super low mortgage rates, because we were pretty sure we were going to buy a new house so it would have just been wasted money, but now it's obvious it would have saved us some money. I had a feeling that would be the case, but my wife seemed adamant we were going to move last year (until we both got too busy with work), so I held off on pursuing it.

I'm in that camp, kinda. We're looking for a small "vacation place". The area we wanted to buy in saw ~40% increase in the first half of this year. We hope it goes back down the same amount (but have no idea!)

In my case, I think it is increased AirBnB demand. Don't know if that will start to ebb.

> I’m in that camp and I’m starting to suspect there are enough people in that camp that any noticeable drop in prices will be immediately met by strong demand, even at current rates.

What you're missing is that when the bottom is in nobody will want to buy a house. They'll be way too terrified or plain incapable of acting. Afraid of losing their job. Of further declines. Of the bottom falling out of the economy. Of homelessness invading their area. Of they job they lost.

Depends on the location but I would say that there are going to be a lot of people who bought homes on expected gains in equity / salary that haven't priced in inflation. Ive been watching homes in a couple markets and the prices have come off and things aren't moving quickly.

If you want to see significant drops in pricing thats going to depend how the winter macro economic environment hits everyone. Next summer is when you will see movement is my suspicion.

Well, the problem with this strategy is it assumes you're employed and still in a financial position to buy a house once prices drop. Housing price drops are rarely disconnected from wider economic issues. If you're unlucky enough to be in the 13% at Facebook then you're likely going to be unable to take advantage of lower house prices when they finally drop.

It's an interesting question, but you might also want to ask which markets people are based in. While the overall economy, interest rates and other factors do correlate to some extent, of course, some other important fundamentals (and price movements) can vary significantly even within the same country.

Some owners will also be forced to sell as adjustable rate mortgage monthly payments increase. Those have still been popular among small investors (and some individual homeowners trying to live beyond their means).

Only 10% of mortgages are ARMs and a smaller subset of these folks may not be able to afford and forced to sell. This is not going to be the hail mary people need.

Prices aren't going to drop significantly in major markets because political forces won't allow it--there are simply too many retiring people with the bulk of their assets tied up in their house. Probably prices will get eroded by higher-than-usual inflation until they come down to somewhat sensible numbers in real dollars, which is somehow more politically palatable, but that's a much more gradual process, so there won't ever be a "great time to buy" in that scenario.

We were thinking about buying for ourselves but opted not to.

However we did hedge that decision by buying my mother in law an apartment and essentially becoming her landlords. We timed it as well as we possibly could have and locked in 2.5% on a 30 year in December of 2020.

We have waited the last couple years, so it's no sweat to wait another year or two for the prices to correct and interest rates to come back down to Earth.

boomers are going to start downsizing or moving to retirement communities eventually. I'm holding back part because of what you said, and part because I can't really make up my mind about where I want to live long term. Happy to rent and collect index funds in the mean time.

Whatever the Boomers are going to start doing, the majority of them have probably already done it. I'm the last of the Boomers, depending how you measure, and typical retirement age is single digit years away for me. The first of them started whatever they were going to start doing close to fifteen years ago.

The big trick is that a lot of systems right now for older folk are built around taking over legal custody of their home, as payment for end of life care or for living money because boomers didn't save for retirement. I don't think we are going to see boomer housing turnover to younger generations. The boomers broke basically every system and process designed to let the next generation get on their feet.

But if they are sold to people who then rent it out, instead of selling it as a home, it has reduced the stock of housing. The game being played is to try and force as much of the US as possible to be renters instead of owners.

Most of these layoffs are mimetic: Meta is insanely profitable and does not need to lay anyone off, this is just an excuse to get rid of some people. So they try to copy everyone else in most of the details.

You can't just view Meta profits in their income statement in isolation. Profitability from the owners' perspective is very largely impacted by the stock price, which has plummeted. From an owner's perspective it makes sense to shore up losses when you're "losing" money (even if unrealized) in other ways.

That said I'm not defending Meta and wish they became employee owned or that capitalism in general would go away.

Redfin's decision is not similar to the others. They are in real estate business and try to take over the market like zillow. Real estate game is more difficult than social media.

Compared to the Blackrock buying up entire neighborhoods, this is unlikely have any effect on prices. Additionally, Redfin's transaction volume was already way down.

We still need a more efficient way to let people transact real estate.

Even just the environmental impact that makes it cheaper to commute an extra 20 minutes to work rather than move seems like reason enough to work on efficiencies. The rental market is also insane, so maybe just focusing there would be easier than in the owner market.

agree, totally disgusting practice which has made homes across all of the US more expensive and forced first time home owners to delay ownership and continue to rent.

Honest question, why is it gross? Fixing up homes is very inefficient and usually done by mom and pops. Why not find an efficient model to do it, just like car manufacturing, chip fabrication, etc.? It's a massive industry and could be a boost to productivity, which is the ultimate driver of living standards in the long term

Former real estate dude. There are a lot of reasons but I'll just run through a few:

A company like Open Door can monopolize a local market very quickly. Pick up 10 listings in a neighborhood, suddenly they control all the comparable properties which means they dictate the housing prices. Or maybe they want to buy up the remaining home inventory in the surrounding areas, and they'll use 10 of their own properties to explain why your home is now worth less.

Corporations can qualify for nearly interest free loans and offer up ridiculously high bids that most private individuals cannot hope to compete with. The effective buying power of a private individual vs a corporation is next to zero.

Corporations probably don't want to flip the home in the short term, they might want it to be a rental for the next 10 years while it appreciates on the books.

So in short, you have a system that can control the housing supply, control housing prices, force out real potential buyers, turn a lot of would be buyers into renters, all while increasing some billion dollar corporation's bottom line. Should absolutely be illegal.

This is the kind of take that could fearfully explain why a national corporation like like McDonald's would be able to corner the food supply to raise prices, then buy up restaurant sites to prevent others from using them. Or how billionaires could purchase all the tickets at Disney World so no one else can go.

Sure, you _could_ waste all your money on villainous anticompetitive practices, but it's more profitable to a) provide a service where you have an efficiency advantage b) only purchase things you need, bidding at the margin, where people don't mind selling to you.

I would expect a system where Open Door is active to be better for consumers and investors than the incumbent system you represent.

This comment is so intentionally disingenuous I don't even know where to start.

But I'll just offer up this:

"Large investment firms are converting single-family homes to rentals and building communities to rent in the Houston metro area to help meet rising rental demand, while the housing shortage is driving more people into renting. The Houston Association of Realtors reported June 15 the number of leased single-family home rentals increased 24.8% from May 2021 to May 2022. While rising mortgages and low inventory are contributing to the trend, experts said potential homebuyers are also facing competition from real estate investment firms—or institutional investors—buying properties to sell or lease.

Locally, NAR data showed 38% of single-family properties purchased in Harris County in 2021 were bought by institutional investors. Property data from the Harris County Appraisal District shows nearly 7,000 homes in Harris County as of June are owned by five NRHC members and their subsidiaries."

In what world would you imagine that this is better for consumers?

I also don't "represent" anything. I worked in real estate from a technical side (mostly CRE), and had nothing to do with the trash that goes on from either side. I just got to witness it.

Yes but opendoor just competes against other companies of scale.

The issue is that individuals who wish to purchase and live in homes cannot compete with companies of scale at all.

So it’s not about anticompetitive practices, because it’s now two corporate incumbents competing, but a corporate incumbent competing against an individual, who stands no chance against that scale of cheap money.

Competitive effects do not always lead to desired outcomes even if they create healthier markets.

Its different from restaurants because housing is a local monopoly, or locally monopolizable. This is due to regulatory constriction of supply and lack of for-like alternatives.

You can't corner the food market by buying restaurants both because there are grocery stores and anyone willing to wade through a small amount of red tape can start a hot dog stand to undercut you. You can corner the housing market in a school district, or neighborhood because families can't live in tents or cars and the government forbids via zoning would-be opportunists from undercutting a monopolization attempt by e.g. turning their 1 unit dwelling into a 5 unit dwelling.

I'd argue that the key difference is that the public isn't having to deal with a McDonalds induced food price increase while the public is very clearly having to deal with housing price increases induced by practices of this sort, especially in big cities.

As soon as someone isn’t improving a property, it isn’t a flipper. Sitting on property exposes them to market risk and makes them a regular corporate landlord.

Yeah I'd have no problem if they want to just swoop in, fix up a house that just needs some love and then get a profit. I don't mind buying an old place but I really don't want to deal with renovating one myself.

If every house costs $600k because it's been "flipped" with brand new appliances, a coat of paint, and other BS things, how the hell is a new generation supposed to afford that?

The problem doesn't necessarily blow up immediately. If people's analysis of the EV of a particular deal is positive on the basis of the bubble continuing, some groups will find continued investment is within their risk tolerance and keep going.

However, if interest rates rise, the EV drops, and sentiment may shift which will substantially increase the risk that market appreciation strategy fails.

Eventually the music stops and enough investors stop pumping the asset class, it peaks, and the lack of retail ability to shoulder the debt-load results in collapse in pricing - some major US banks have indicated that mortgage originations are down 90% this year.

Interest rates are only part of a larger calculus. What ultimately blows the problem up is a shift in perception about real estate being a good investment vehicle for large sums of capital.

Open Door has laid off 20% of it's work force, it's stock has gone from $24 to $1.5 in a year, and it's losses are increasing.

Black Rock was buying entire subdivisions developed for the purpose of being sold to investors. They were basically large scale apartment complexes. That's wildly different than buying up random homes throughout a city.

Zillow had to give up last year and showed a $300 million loss, and now Redfin is too. I'm not saying it's impossible, but SFH flipping doesn't scale well at all.

I still dont know what you're talking about or if you're just unaware of the data.

"Locally, NAR data showed 38% of single-family properties purchased in Harris County in 2021 were bought by institutional investors. Property data from the Harris County Appraisal District shows nearly 7,000 homes in Harris County as of June are owned by five NRHC members and their subsidiaries."

>Citing NRHC member-provided data, Howard said that out of 23 million single-family rental homes in the U.S., only about 300,000, or 1.3%, are owned by large companies.

NRHC includes the aforementioned Blackrock. Your quote says the top 5 SFH companies own 7,000 homes in Harris County. A county with 1.6 million homes. The sexy headline of 28% of all homes being bought by institutional investors says an LLC is an institutional buyer. It wasn't Blackrock hoovering up all these homes, it was smaller shops and normal people flush with cash and leverage.

Your idea of "normal people flush with cash" is ... private equity lol. It's incredibly common for companies to spin off random LLCs to buy up whatever they want.

Putting a rental in an LLC is very standard advice for anyone buying one. You've clearly made your mind up about this and won't change it if you think PE is buying up all these homes when you linked an article saying 5 public companies with $110 billion in market cap with access to almost unlimited amounts of cash only managed to capture 1.3% of the market.

There are plenty of REITs operating in my city that have substantial detached residential holdings.

The EV on renting and holding substantially improves if the housing market takes off like a rocket. It might not work in your market, but that doesn't mean it doesn't exist.

It's not a hypothesis. You don't need to believe it exists and it may be less common in your market. I know this is true firsthand as in the course of my work, I review the financial and legal side of these entities at times.

> Fixing up homes is very inefficient and usually done by mom and pops. Why not find an efficient model to do it

I 100% agree with this premise.

However this is not what Redfin/Opendoor/Zillow do. The most you're going to get regarding "fixing" is a very bad coat of paint, replacing a couple angle stops, and putting a full cover-plate over an outlet that seems iffy.

These companies are not taking an unmarketable product, actually fixing it, and putting a restored property on the market.

I agree that actual property restoration is a fantastic industry to optimize, and I could talk about this for way longer than is appropriate in this post. But the best you're getting from these companies are some lipstick-on-a-pig photos and a sellers disclosure that says "We never occupied the house so have no idea if there are any issues".

There are also other financial-engineering-esque fashions in which they make money, which are all at the expense of residential home buyers. None of the ways are actually "improve the property".

Could you imagine if corporate buyers were required to upgrade everything to meet current code before selling? It'd likely kill the process dead, of course, but if not then at least we'd see improved homes as an outcome.

It's really just daydreaming, but in any case, I'm not convinced that corporate buyers of used houses increase the quality of housing stock. Corporations building new houses likely do, and that's where their money would go if they are truly interested in real estate investment.

Given that a lot of flippers/corporate buyers use corporations as a liability shield in case of something going wrong, they have less skin in the game than potentially negligent previous owners. It generally seems reasonable to treat individuals and corporations differently in terms of legal expectations, in part because of that.

There is no difference in legal expectations. Any negligence by previous owners is legally irrelevant. The previous owners are in the clear regardless of what they did to the property, provided they follow state disclosure laws. They would only be liable in the case of actual fraud.

New construction is a bit different in that some states have a mandatory warranty period for major construction defects. So the new homeowner may have several years to make warranty claims against the property developer or contractor for negligent or non-compliant construction work.

Sure, agreed. And I figure a corporate buyer would only go through with that is the home is bad enough that it's worth replacement. Most probably aren't, so they'll be left available for humans. It's win-win.

(I fully acknowledge this is an unrealistic proposal.)

They are doing it out of speculation - not improving the efficiency of the market. They thought that they had a lock for a large windfall of profits based on the trajectory of the housing market.

People don't like that because that profit comes at the cost of people who are trying to find homes at a reasonable price. I am happy their model didn't work.

Also I think you assume that their model would be efficient but I don't think it would - you still have to work with all the small mom and pop shops who are doing the actual renovation work and that quality is worker specific. There is no proof that Redfin's model would improve quality or efficiency.

Add in redfin trying to guide the market buyer on the price to purchase with their price forecast mechanism ... which I would not be surprised if they boosted their own properties (speculation, but wouldn't be surprised at all).

If that is all it was, then that would be great. It would be nice If we had a handful of corporations that outsourced to local contractors to refurbish houses before reselling them, while taking a small profit for themselves.

The problem is that these companies are more interested in driving up the price of housing, than they are in fulfilling the need to facilitate a market, and make repairs. So you end up with prices artificially driven up, and many properties being used as investments against inflation. Which means that people in lower valued homes are now unable to upgrade, which means that there is less available at the low end, which leads to more homelessness.

I think local municipalities should enact speculator taxes, for anyone who owns an unoccupied property that was not recently inherited. Maybe you get 18 months after your parents die to either sell their home, or take on a tenant.

There are properties near my house that have been for sale for over 15 years. Which means the speculators holding these properties have likely paid more in taxes than they will ever get for them.

Basically I don't think that holding property hostage should not be a legal business, either you sell/rent it at the current market values, or you pay out the ass for the privilege to wait it out.

> I think local municipalities should enact speculator taxes, for anyone who owns an unoccupied property that was not recently inherited. Maybe you get 18 months after your parents die to either sell their home, or take on a tenant.

I'd actually agree with this, with the addition of "or appeal as to why you can't". 18 months seems like a long time, but there are many situations where you just can't get something settled in that amount of time.

It's gross in my opinion because they drive prices up. Not only the companies, but also individuals that purchase multiple homes to run a rental business. I want to see legislation that prohibits orgs from purchasing home to flip, and individuals to be taxed heavily for their 2nd+ home.

If an org really wants to profit from real estate, go build new homes, there is a huge shortage, we don't need to competes with rich companies when trying to purchase a house.

As a real estate investor, I can assure you that taxes on an investment property are already much higher than a homestead property. This is the main reason that outside of HCOL areas, monthly rent tends to cost more than mortgage + taxes on the same house.

I would love to build houses but unfortunately, it costs about twice as much to build a new house or apartment building than it does to buy an old one and bring it up to date. That's not even including the zoning/permitting headaches of various municipalities.

(And to be clear, I'm not advocating for the abolishment of zoning/permitting, just that some municipalities make the process unreasonably hard/expensive just because they can.)

I think if we're allowing people to own multiple homes, that should be available not just to the ultra-rich

Putting on a heavy tax burden realted to the house price means that eventually, you get rich enough where its not even an inconvenience, and those people will have an even stronger cartel over land use

They won’t. This means that there will be properties eventually owned by a local taxing authority.

What people don’t get is that you need some houses to sit empty. This allows people to find a place when they move. This allows people to move around within a territory.

Also not all secondary houses are bad. I want to buy a plot of land for a small farm and a place to go in case of hurricanes. Presently there is no house. Should I be taxed for improving land for personal ways that didn’t remove housing?

Many of the comments so far are emotional. We need to do better when making policies.

> Should I be taxed for improving land for personal ways that didn’t remove housing

I’ve never done this so don’t know the answer, but when you build a house don’t you then also start to get government services in support of that house?

> Fixing up homes is very inefficient and usually done by mom and pops.

This doesn't ipso-facto make it inefficient.

There's evidence that construction does not become meaningfully more efficient with scale [1]. At GIGANTIC scales, you're looking at maybe 10% savings. And these scales are quite rare in the US & the EU - mostly only happening in Asia.

True, on the largest investment of most people's lives - 10% is something...

Anyway - you're not going to get great returns with layers of high-paid management and beat mom & pops by much.

> It's a massive industry and could be a boost to productivity, which is the ultimate driver of living standards in the long term

Is it thought? Productivity has been going up for 20 years, so have essentials like housing, healthcare, and education. Wages haven't kept pace. Efficiency in the service of inflating housing prices further seems like it's going to tank living standards for many people.

Would you be OK with pricing food so high that only a limited amount of people could eat, with the pure purpose of "make more money for our stakeholders"?

How about the same, for water?

How about the same, for basic medical?

How about the same, for electricity?

Profiteering and gatekeeping essential things to live is ethically abhorrent. And yes, housing SHOULD be a right. Instead we have "right to badmouth government" and a bunch of other 'self-actualization' (Maslow) style needs, but We collectively ignore the bottom ones, like food/water/shelter.

You don't need to go as far as to demand detailed central plans, as if the parent poster is a Soviet tankie. All you have to do is get rid of the already-extant central planning regime that the US has, which is specifically designed to keep land expensive.

Or, in other words: "housing is a human right" does not need to be construed as a positive obligation.

Even if we decided on positive-freedom housing rights, it doesn't mean giving everyone a California beachfront property. This is the thing a lot of Americans don't get about positive rights in other countries: when they exist, it just means that the country is going to use tax money to pay for and provide that good. This works for the same reason that welfare programs work: the existence of a large buyer, even one that's lowballing, provides price stability to suppliers.

California beachfront property can remain expensive, but the houses behind it should be allowed to build up to whatever density that the market will support.

> Or, in other words: "housing is a human right" does not need to be construed as a positive obligation.

I struggle to think of a way to construe it that is not a positive obligation.

Increasing zoning is not making housing a human right. It is bringing down housing prices, which is great, but it would make words meaningless if it qualified for “housing as a human right”.

On the other hand, the government reimbursing everyone for the annual cost of housing in the 20th percentile of the US is something actionable. For example, if housing at 20th percentile is $12k per year, then everyone gets $12k per year to spend on housing. They can choose to move to wherever they want.

And that example is basically UBI, so might as well just advertise that as the solution.

> You don't need to go as far as to demand detailed central plans, as if the parent poster is a Soviet tankie. All you have to do is get rid of the already-extant central planning regime that the US has, which is specifically designed to keep land expensive.

I'm not advocating public execution of billionaires here.

I'm talking about getting rid of companies like RealPage ( https://www.propublica.org/article/yieldstar-rent-increase-r... ) and other companies that either collude information asymmetry or otherwise buy up the market and wait to artificially drive prices higher..

I'm talking about restrictions of companies buying residential dwellings (not corporate dwellings, but im sure that could be gamed).

I'm talking about rent control. I'm aware that's a top-down command approach. Maybe use it as a cap per sqft?

I'm talking about relaxing or eliminating zoning restrictions. Much of them were put in place as a racist plan during the 40's-60's.

I'm talking about having banks *require* including on a mortgage application if you've paid rent for X years at Y rate, that you qualify for a mortgage of the similar terms.

I'm talking about having the mortgage rate be different (LOW) for your primary residence.

I'm talking about converting apartment complexes into a benefit corps run by the people who live there. Again, having people live in dwellings where they reasonably know that they are safe is inherently a great thing, and builds a real community. Problems that arise can be handled by the people who live there, like if a recession hits and 1/10 lose their jobs. (Yes, this is more radical.)

Every one of these changes would enable more people to have their own place to live, and live better how they want to live. Does it solve every problem? Of course not. It's steps to do this. And what I see here in my area, we're going the very wrong way. More and more are going homeless or vanlife every week. And that piece of stability disappears. And it's hard to reestablish once you're in that direction.

It's not just an individual issue - at a certain number, it turns into a societal issue that needs a society-wide solution.

This is true now and we don't need a government guarantee of housing to make that happen. What I don't like is people who want to live in a specific place they would like to live, and wanting subsidies from others so that they can live there at below-market prices.

Right, so I am interested in determining how space is allocated under a system with a “right to housing”.

Do you apply to the federal government and get sent to where it is cheapest for the feds? Do you get preference for a certain region if your ancestors and relatives are more numerous there?

People would have to use alternative modes of transport, and eschew individual cars, like people in Hong Kong. I do not understand “roads turning to dust” though.

You should look at the track record of providing food, water, and shelter in places where you don't have a right to badmouth the government and instead had "rights" to things like food and shelter.

So the government has the right to take your money to spend it building housing for someone else? "Housing is a human right" is a lazy, armchair argument that demonstrates a lack of understanding of the housing market.

Whereas I'm arguing that housing shouldn't even exist as a "market" to begin with, at least in terms of residential housing. Or at least, prevent companies from owning residential housing, except under stringent terms. There's plenty other places capitalism can take hold.

I fail to understand why heavy controls that enable real humans (not made-up on paper corporate humans) to get a residence of their own, is so damned radical.

I see what the environment looks like, with RealPage ( https://www.propublica.org/article/yieldstar-rent-increase-r... ) and Zillow and Redfin, and whomever else is buying residences left and right. And I want none of it. Burn these parasites to the ground. And damn the "profit".

Because they do a terrible job at it. I looked at a flipped house once, and they built a laundry room - with no place for a dryer vent! (I guess they hoped no one would notice.)

They had gas service in the home, but instead of running that to the dryer or range, they ran electric because it was cheaper to run a wire.

Every single thing they did they picked the cheapest, worst, option. Anyone buying that home is in for an expensive annoying time as they have to re-fix tons of things they did.

They had to change the plumbing in some areas, and instead of a 3/4 pipe, they ran 1/2 inch to far too many fixtures - you'll never notice, until you try to shower and run the dishwasher at the same time.

It was just non-stop shortcuts.

I made a policy of not even going to look at a home that was fixed without the owner actually living in it afterward.

Hopefully the home inspector is noticing these things.Clearly permits weren't pulled for many of these things since they wouldn't pass code.

But yes I agree, often flippers are taking every short cut they can to make something look nice to unsuspecting buyers but it will all fall apart in 5 years. Cheap vinyl windows is the biggest violators I've seen. Even in nice homes going for $1m.

Efficient as in "most profitable?" That means changing a few cosmetic things about the property and charging the original value plus 2-3x the useless improvements that were made.

When I was house hunting a few years ago, you'd see this all the time. Someone buys a crappy house: bad plumbing, bad electrical, leaky windows, foundation issues. What do they do? Put in some frosted glass Ikea cabinets, granite countertops (wooo fAnCy!!!1), and some crappy click-lock flooring. Then they charge 150K more for the house than they bought it for.

This is my experience with flippers, and it's totally in line with "find an efficient model." They did find an efficient model: efficient for them, but sucky for the people who can no longer afford the home, and sucky for the poor sap who actually buys it and now has to dump another 200K into it to fix the real issues (and will likely end up ripping out the cabinets anyway because they are cheap and ugly).

I know there are people who do good flips, and who fix the foundational issues, but I am willing to bet they are much more skewed toward the "mom and pop" flippers.

A lot of people are cash-poor and need to make up the difference with "sweat equity". That puts them in direct competition with professional flippers, since its the same unrealized value that is being leveraged. The difference is that for one its a tidy profit, whereas for the other its a way to own a home.

Then the people needing to make up the difference with sweat equity should be able to pay more for the house than a professional flipper, since they do not need to account for the profit and costs of subcontractors of professional flippers.

unfortunately sweat equity (ie fixing a place up) doesn't add anything to your down payment from the bank's perspective.

Cash poor is cash poor. Most people start off as young people or young couples with little to no cash and have to make their way in the world in the basic range of minimum wage and starting off with zero savings.

Saying that corporate profits should come before home ownership for the average person is what was being thought of as "disgusting" earlier in this thread, I think

There's a large grey area of old/marginal/condemned housing stock where buyers are making a tradeoff between a teardown + rebuild vs buying an old house and patching it up.

Flippers who successfully rehabilitate an old house do increase the effective supply.

Where I live (UK), I think most young people would be grateful for an increased supply of cheaper rundown houses to buy. Done up houses we can't afford don't help at all.

I might have answered my own question - perhaps it's when we see corporations speculate and win it adds no value and is gross? But if they actually do come up with a better way to price houses and fix them efficiently it's a positive right?

Maybe at the end of a long road of terrible home buying conditions for the entire country. One has to wonder if put together it would be a net positive.

For the parachute pants aficianados, the 1980's used the term poison pill to thwart certain strategies. The linear explains a lot of "fun the mentals/fundamentals" in place in 2022.

Isn't the more apt to compare this to car restoration/repair or something? Fixing up homes isn't like a factory you can streamline and automate.

Just anecdotal, but the first house I bought had some issues that enabled me buy it at a discount and fix it up over time to my liking. I'm thankful I had that opportunity, and I still would've probably upgraded certain things if the flipper just went with the base options.

They aren't really in the business of fixing up a home, as other people have already said. The analogy for what they are trying to do is more like high-frequency trading (as the amazing and invaluable Matt Levine has pointed out for years).

When you want to sell 100 shares of Company A, and someone else wants to buy 100 Shares of Company A, sometime you do so at just the same moment, and you can directly transact with them. However, almost all of the time you are selling and they are buying a few minutes apart. So called "Market Makers" (aka "High Frequency Traders" aka "Flash Boys") take the other side of both transactions, and get a very small cut (generally less than 1% on the modern stock market). They are basically in the business of time-arbitrage. Their goal is to almost always be net zero on the market- to have roughly the same number of buys and sells at any given moment, so that the market floats along smoothly and they make their tiny cut whether it is going up or down.

And so the home buying version of this is, it is a real pain to have to find a buyer for every seller at the exact same moment. If we could similarly have a market-maker who can buy houses and sell houses when someone comes along looking to be the other side of that transaction, wouldn't it be awesome? You could take a tiny cut of the transaction, but what a big transaction! Just for some time arbitrage. Of course, the differences are stark: shares of stock are fundamentally fungible, whereas houses are almost as non-fungible as one can get. Stock transactions are quick and painless, and don't require months of work by teams of mortgage originators, with inspections and appraisals etc. It is difficult to be net-zero as a market maker in houses, since your inventory sits on your books for months and months, either appreciating (yay!) or depreciating (boo!). All of these are serious problems with the business model. The current wave of companies attempting this basically said "what if we fix this with <waves magic wand> Artificial Intelligence?" The actual answer is that they have once again found themselves in the business of picking up pennies in front of a steamroller- the fate of all arbitrage attempts that blow up.

Matt Levine wrote about Zillow's failed flipping business in his newsletter last year. The way he described it seemed less evil than I imagined. I had imagined corporations trying to corner a market so that they could sell at inflated prices.

Instead, it sounded more like Zillow was providing a service of adding extra liquidity, which can be useful. For example, if I want to move to another house, but it's going to take me 90 days to find a buyer and close, I might be willing to pay a premium to sell it to Zillow so that I can get out faster.

I don't know if that accurately characterizes Redfin's business, but I think there's more to it than just evil corporations making life miserable for everyone else.

I don't know about gross, but just shows insanity of the market involved. In sane and reasonable markets there should not be enough room for such action to be profitable at large scale.

On timing the market: you cannot time the market. However, you can have a sense of what the historical rates for mortgages are and will probably return to.

Back when they were at ridiculously low levels, I would tell people "Get a 15-year loan now! You'll be paying off principal as well as interest, real soon."

They'd object, reasonably, "Oh, I can't afford those payments!" So now with higher rates, what will they pay for that 30-year?

You can also object that nothing stops you from making extra principal payments, on top of your regular monthly payment. That's true. But will you?

Is all that incorrect? You can do this analysis in Excel or Google Sheets.

This doesn't make sense to me. Why wouldn't you go for a 30 year loan when rates are low? You lock in your low rate, and you lock in a low monthly commitment. If budget allows, you can make additional payments towards the principal.

This is almost always optimal, even if you can easily afford a shorter term loan. Banks usually give a better rate for a longer term loan.

> Banks usually give a better rate for a longer term loan.

I think, only in rare circumstances, like rates being unusually high, such that they will almost certainly go down.

Locking in rates costs money. Nobody will give you a reduction in risk for nothing. Often they are a bad gamble, because if you're in a long term loan, even if the rate is variable, the length of the loan itself provides the averaging to de-risk that.

Most people work with spot rates for all sorts of stuff they consume. You don't get to negotiate a 30 year rate on steaks, milk or gasoline. You can still buy those things when prices are low and average things.

You're missing the point, or you didn't read the post.

A 15-year payment is higher, of course, but after 15 years you've paid it all off. After 5 years, much of your payment is going towards principal, not interest. You can do this calculation in a spreadsheet.

The question is: when rates go up, at what point does the new 30-year monthly payment equal the old 15-year, when rates are lower?

> If budget allows, you can make additional payments towards the principal.

Flexibility is tremendously valuable. In absolute terms a 0.7% difference is really small. Individual circumstances varied, but for average middle-class consumers the smart move was to take the 30 year mortgage. Then they could make extra principal payments, or if money gets tight one month then just pay the minimum without worrying about defaulting.

Sure in an ideal world we would all have 6 months of living expenses in an emergency fund plus multiple independent income streams so that getting laid off would be only a minor inconvenience. But the reality is that most homeowners have few other assets and just one job, so they have to plan within those limitations.

At any given instant, your monthly payment for a 15-year will be higher than for a 30-year. You're right that if you can't afford it, then you shouldn't do it.

If you can possibly afford the payment for a 15-year: in 15 years you'll have a monthly payment of zero, because you'll have paid it off. After a few years, you'll have started paying off the principal.

And, of course, if rates go up (as they have), then in a few years the monthly payment for the 30-year will be approaching what you would have paid a couple years ago for a 15.

You also are missing the point. Potentially having the mortgage paid off in 15 years is meaningless if you have a cash flow problem in 5 years and default. That is the greater concern for most consumers.

Rates going up in the future is irrelevant if you have a fixed rate mortgage, so I don't know what point you're trying to make there.

> Rates going up in the future is irrelevant if you have a fixed rate mortgage, so I don't know what point you're trying to make there.

OK: assume you locked in a 30-year loan 2 years ago, because it didn't even occur to you to get a 15, or you couldn't afford it.

Now, you're set in your place for another 10 years. You didn't expect that kind of stability, but time just flies.

So in 12 years, you'll still need 18 years to finish paying it off. There's no point in refinancing, since rates are higher now.

Had you gotten the 15-year, you'd be within 3 years of zero mortgage payments. If you're in high tech, quite likely you'll be earning much more after 12 years, and that monthly payment will be no problem.

You're right, the "quite likely" does do a lot of work here. You're taking a risk. No argument there.

> if you have a cash flow problem in 5 years and default

That isn't a problem in practice. Most banks don't want to foreclose and they'll restructure your loan, as long as you're not a deadbeat. And in 5 years, you'll have paid down the principal, at least a little. More than you would have with a 30.

I am this person. I refinanced from a 20 year at 3.6% to a 30 year even lower. I could have afforded a 15 year rate, but intentionally chose the longer term. The payments are lower and give me more cash now to put in the market and earn significantly more than my mortgage rate.

At the moment, my mortgage is dramatically lower than inflation. I would take almost unlimited credit at this interest rate and not pay it back early; several hundred thousand was a no-brainer.

Many or even most people would just spend the extra money, not "put [it] in the market and earn significantly more than my mortgage rate." The default rates after the 2008 crash proved that.

EDIT: The parent post is a modern sophisticated financial theory, and it's absolutely correct.

Your great-grandparents, who lived through the Depression, might have a much different take: "Debt is bad. Do not have any debt."

That's irrational, for sure. It probably resonates with you on some level, though.

This entire comment lacks evidence or data to support it but I used to work in SFR and still keep tabs with several companies on a personal basis.

Redfin and Zillow are not the problems in the SFR industry. These are tech companies that were trying to capitalize on the PE flowing into SFR. Their lack of success is not an indicator for the industry as a whole.

Make no mistake about it: SFR is alive and well and increased rates will not hurt them. Most have paused acquisitions but their cash flow is still fantastic. The outcomes over the next 24 months will play in their favor and those companies will grow as the economy pulls back.

I recognize you have a username that implies that you know a thing or two about this SFR space, but I don't think anyone here is saying that redfin/zillow/etc are the problem with single family rentals, because they are.... not in single family rentals.

Rentals, and trying to quick-flip properties, are different business models.

I think your point about SFR is correct, but it seems off-topic and confusing/misleading in the current discussion context.

Pension funds want to mitigate risk and rental cash flow is a reliable and proven way to do it. When the economy pulls back, these funds will look for solid cash flow options. SFR, like a REIT, is a good choice. When money flows in, this will be used to acquire additional homes.

In short, pension funds looking to de-risk in equities will move towards SFR. This isn’t US-only, but the SFR will be US-only. So expect EU nations that allow their pensions to investment in US assets to move more money towards SFR. The number of homes managed under institutional SFR will grow substantially in the coming years.

IMO the mistake was having the demand almost entirely unregulated while having supply highly regulated. It's a system designed to steal from the youth via regulatory capture by the property class.

I had no idea Redfin had the home flipping unit too.

The real estate prices and estimates clearly are on a downward trajectory. Previously redfin struggled to keep up with growing value in their estimates and so always came in lower to the asking price. Now they constantly come in higher.

> Nothing stopping it from coming back when rates go down

True, IF.

> It's a feature of the 7.7% average mortgage rate, which is not great for buyers.

It's not AMAZING, but it's also pretty good. I bought my first home in 2010 at 5.4% - thanks in part to a ton of incentives at the time. My non-subsidized rate should have been closer to 7%. My parents bought their first home at a whopping 17% in 1976. It's important to maintain perspective; just because interest rates were incredibly low for a very long time does not make it the norm. The historical norm is far higher. The crux of the problem now are home valuations and asking prices combined with the interest rate. A home I bought in 2018 is now valued at 125% of my purchase price 4 years ago. The lack of inventory and inflated pricing are a direct result of the corporate buyers' actions over the last six or so years.

>The lack of inventory and inflated pricing are a direct result of the corporate buyers' actions over the last six or so years.

Is there any portion of lack of inventory and inflated pricing attributable to zoning restrictions, agglomeration of secure economic opportunities in fewer regions, increased labor and materials costs, and taxpayer subsidized mortgage lending?

> No, it's because we stopped building homes after 08 but didn't stop wanting new ones. The REIT's are just responding to that.

That's patently false, universally. A sibling comment has a good reference. You can't go an 1/8 of a mile in the greater Tampa Bay region without running into a new build.

A couple of years ago I tried to rent from one of these companies but things didn't work out. I did double take and was thankful because I don't want to support and encourage this kind of business model .

Corpo home pillagers deserve everything bad they're getting. Young families need homes. I wish the government would step in and protect something so necessary for it's citizens.

> I wish the government would step in and protect something so necessary for it's citizens.

You mean like the mortgage interest deduction, 30-year fixed (subsidized) rate, SALT, Prop 13, etc - that actually make the problem worse for new buyers?

Not sure if you're being sarcastic. The comment you are responding to is specifically saying that by doing all those things that it makes the nominal prices of homes more expensive. It's basically identical to the idea that by guaranteeing/subsidizing college loans (and disallowing most borrowers from discharging loans in bankruptcy) that the government has been instrumental in the skyrocketing cost of college.

{kind=link}

I’m in that camp and I’m starting to suspect there are enough people in that camp that any noticeable drop in prices will be immediately met by strong demand, even at current rates.