There's a lot of information, history and a broad perspective on how things work in various countries.

Housing politics is key to so many things:

* The economy - allowing people to live in productive places is a benefit to them, and all of us, because they put their talents to more productive use. California, where the housing crisis is worst, also has the highest poverty levels of the US when cost of living (which is mostly housing) is factored in.

* The environment - cities are more environmentally friendly than sprawling suburbs.

* Equality and "social justice": the history of how people of color have been frozen out of the housing 'ladder' in the US is not as well known as more blatant and vicious examples of racism, but it is a huge reason why certain disparities have persisted.

"That's why the same size house costs more in a city." This idea is actually debunked in the report; Singapore and Tokyo do not have a similar kind of problem in American cities because there's more construction of housing. In America, there are more restrictions around building and less tenant rights (compared to Germany/Switzerland) which causes American housing to be an asset for both wealthier/older US citizens and foreigners.

No, it wouldn’t. A proper land value tax is based on the unimproved value of the land. Farms are almost exclusively built in areas that have much lower land values than cities.

Farming would already be discouraged if farmers could build skyscrapers over their fields and collect the rents from those buildings. Since nobody wants to live in a skyscraper in the country, this never happens.

Interesting. After some thought, I’d summarize that all taxes on income and assets..including property.. are inappropriate.

We should have a flat consumption tax for all. And a single one time child tax. It is in effect a double tax, but still will be lower impact than the cacophony of various taxes we have now...it can be used to fund education. Currently funded by property taxes.

a single flat consumption tax will stabilize economy. I suspect that it would also curtail consumption and carbon foot print. A tiered consumption tax might be punitive but not a terrible idea even though it ought to be a back up or a emergency measure during crisis situations.

Food, shelter, medical and educational expenses should be taxed after a minimal deduction.

I don't know a lick about the book mentioned or literal references you have been silently recommended to study. Obviously the implied message that you've yet to pick up on is that you should try and research your own ideas before profoundly postulating positive platitudes that are .... full of P?

anyway, i suspect your "idea" is bad from the start... you say tax consumption... AND THEN tax the (just?) born... do you even darwin bro?

You are giving the disenfranchised the shaft from the outset.. who do you think would like this? who do you surround yourself with to get to this line of thinking? Rhetorically, I'm done.

i am assuming it’s the child tax that’s seems to be a problem for you. I didn’t suggest anyone read anything. I think you might have mistaken subsequent comments to be mine.

Perhaps if I expanded that as ‘pay taxes for the consumption of your own child’? And pay a fee before having kids. This could be in the form of a community trust or an investment fund at county, state or country level.

We pay different kinds of taxes but children are negative taxes. As in, cost of rearing children is mostly subsidized by the govt with taxes.

My suggestion was that every consumption good needs to be taxed. When income, property, inheritance etc are not taxed and only sale of goods is taxed, everyone pays a tax according to their lifestyle.

Example: a sleeping cot is taxed much lower than a yacht or a house. Parents save and pay for their children’s education. The retirees live off retirement plans.

In my last sentence I mention that food, shelter, medical and education are only taxed after minimal deductions. Which means, everyone essentially gets a kind of UBI for essential needs before their consumption in these survival categories is taxed.

Obviously if one is ‘disenfranchised’ there is charity. Currently we consume too much using credit lines and debt. The key is to restrict consumption and eliminate waste/scarcity...have more local governance than regional governance.

It will discourage hoarding. Unproductively using land in high value locations that are growing is currently rewarded - with asset appreciation.

If it is discouraged - with taxation, that land will be yielded to more productive use.

Nobody creates land but somebody gets to "tax" it. Either we can let that revenue stream fill up government coffers or it can go into private pockets. It's our decision.

> Nobody creates land but somebody gets to "tax" it.

Well put. If I suggested privatising air and that you needed to pay the owner to breathe it, that would be seen as ridiculous, and rightly so. Meanwhile, land is an equally natural resource and equally essential to human life, but private land is just accepted as "the way it is".

This isn't a reasonable comparison because air is almost completely fungible; it's automatically redistributed throughout Earth by the magic of physics. Not only that, it's not scarce.

People in fact do pay for 'special' air in the form of air purifiers, air conditioning, heating, etc.

Land taxes won't lower rents but probably won't increase them either, as rents are set by supply & demand. The cost for renting out a space over keeping it empty is minimal. Meanwhile the tax revenue can be used to subsidise rents (for example).

IMO land ownership is a big negative externality, as others can't utilise that land and land is a finite resource. As with all negative externalities, they should be taxed heavily.

In most places there are a lot of restriction on building houses, so i would argue that housing is more finite than land. If you have planning permission in the UK, your land will be worth a lot more than land without.

> Equality and "social justice": the history of how people of color have been frozen out of the housing 'ladder' in the US is not as well known as more blatant and vicious examples of racism, but it is a huge reason why certain disparities have persisted.

In my city (and several others) you can overlay a current map of "above/below poverty line" on top of a 1930's map rating neighborhoods by "risk".

Those rated low quality/high risk due to "threat of infiltration of foreign-born, negro, or lower grade population" in the 1930s line right up with the largest swaths of below-poverty-line neighborhoods today.

>California, where the housing crisis is worst, also has the highest poverty levels of the US when cost of living (which is mostly housing) is factored in.

The housing crisis is relative. It's a crisis when your relative moves in.. All joking aside, _every_ major metro has an affordable housing crisis.

That's a funny joke but the housing crisis in CA is no laughing matter. many have lost family and friends who have had to leave the state. millenials have stopped having children. and the few who can buy are taking on insance mortgages to pay off million dollar homes which are supposed to cost 250K. Imagine global warming burning down every last house in your city 2-3 times and now you've got the approximate financial damage caused by the housing crisis in CA

That mostly seems like an artifact that first world countries are much more urbanized than third world countries. Wealthy consumers generate much more carbon per capita in general.

New York City may produce more emissions than Papau New Guinea. But I don't think moving people from Manhattan to Vermont would lower emissions. Just the opposite in fact.

A person's carbon footprint is directly related to their wealth/income. If 80% of wealth/income is in cities, this isn't surprising.

Further, the definition of "city" can include a lot of sprawl in places like Houston, Phoenix, and even Beijing and Tokyo.

Even further, can you cute your source? I'm skeptical of both numbers. And it would be very easy to cherry pick either side of these numbers.

For example, a lot of concrete is pored in cities to build mid/high rises. Concrete produces a fuck-ton of carbon. Is this amortized over the expected lifespan of the building? Where is the carbon cost accounted for? A lot of the carbon is emitted in rural areas. But is it all just lumped into the city because that's where it's used? That seems unfair. A lot of rural wealth comes from natural resource extraction used to build and power cities...

Most power plants and factories are outside of cities. Yes, they mostly power the city and produce goods for the city -- but their providing a lot of income/wealth to rural areas...

This is based on the concept of a "consumption emission", which is an interesting concept. The point being that cities (especially western cities) have seen their emissions drop due to de-industrialization, but consumption has increased (hence your statement about carbon footprints correlating to wealth/income). To say that cities impacts are smaller when they just outsource all of their carbon impact is disingenuous.

From your source: It usually incorporates the population in a city or town plus that in the suburban areas lying outside of, but being adjacent to, the city boundaries.

GGP suggested that suburban living is greener. How does the 50%/70% support his point if cities include the suburbs?

The point is, there's likely a certain density at which it gets progressively more green to live in. If you're treating all cities equally, there's hardly a point in distinguishing between cities and small towns. There's not much of a difference between Omaha, Nebraska and Podunk, Kentucky. There's a gigantic difference between Manhattan and Yonkers.

I wouldn't be surprised if Dallas is "less green" than small towns in Italy, even adjusting for income/wealth. I would be surprised if the same is true when you compare to inner Tokyo (Shibuya).

One thing that would be interesting to know -- high rises can use a ton of energy to heat & cool. And the taller they get, a significant portion of the building is just stairs and elevators. I wouldn't be surprised if density gets "less green" at a certain maximum. Manhattan & Shibuya could very well be past that point.

>One thing that would be interesting to know -- high rises can use a ton of energy to heat & cool.

Sure, but how does that compare to the energy needed for lots of smaller buildings, which can provide the same floor space to the same number of people? I suspect the high rise is more efficient: it has far less surface area on the outside. The more surface area that borders the unheated/uncooled outside, the more energy you need to expend.

>And the taller they get, a significant portion of the building is just stairs and elevators.

Again, how does that compare to smaller buildings? Once you get past 1 floor, you're going to have to use space for stairs and elevators. You can't have a city with 1-floor buildings; the sprawl would be ridiculous.

>Manhattan & Shibuya could very well be past that point.

Have you been to Shibuya? Buildings really aren't that tall in Tokyo, especially in Shibuya. Remember, Tokyo (and pretty much all of Japan) is a highly tectonically active area, with frequent earthquakes. Manhattan has no earthquakes and has a huge layer of bedrock under it; it's basically the most idea place on the planet for building skyscrapers, except for being close to the sea (because of hurricanes, but these are rare because it's pretty far north). There are some reasonably tall buildings in Tokyo, but nothing like the 100-story behemoths in Manhattan.

Yeah, skyscrapers have a lot of stairs and elevators, but I'm pretty sure switching to a bunch of smaller buildings and replacing the stairs and elevators with roads and automobiles is not going to come out ahead on environmental impact.

I think in the statistic you cite, 'city' includes both the urban part and the sprawling suburbs. You'd also want to compare apples to apples: someone living a very green life in a "western" city is still likely to live a more carbon-intensive life than someone doing subsistence farming.

Carbon emissions aren't the only impact humans have on the environment. As one other commenter pointed out, the further humans sprawl the more we encroach on wildlife habitat.

This trope of environment === greenhouse gases in the atmosphere is dangerous.

There are significant demographic issues to account for, especially when looking at such high level statistics. Your breakdown also doesn't take into account the inverse land-use factor. High density in one location allows for lower density elsewhere, with additional environmental effects.

Directly touching sure, but what about indirectly touching. If those city dwellers are all using more carbon and creating more pollution, then they may touch more wilderness.

yeah, that might be true if we built cities where the only means of transportation was public transit. But I'm thinking of all those skyscrapers in SF, and how many folks make 1-2 hour commutes to work in them.

If there were more housing close to those skyscrapers; if it were legal to build it, those people would have shorter commutes - and occupy less land to boot.

Instead, San Fran is one of the NIMBYest cities on the planet and so all those people are forced to come in from further afield.

The skyscrapers themselves are pretty eco-unfriendly as well, frequently built as essentially a giant greenhouse with heavy heating & cooling loads to maintain comfort.

I suppose you might look at some technical discussions of whether you're better off with a larger area built up to 6-10 stories or something like that, than fewer, taller skyscrapers, but in general, that denser environment keeps cities from sprawling out, and is more friendly to people walking around.

Many european cities max out at 8 stories simply because they were built before the advent of elevators, or the design aesthetic started before the elevator and they're keeping new neighborhoods consistent.

4 floors is mildly inconvenient on foot but 8 floors is becoming a real chore for people over 40.

Almost no buildings beyond 4 floors (5 the way Americans count them) lack elevators in Germany or Austria at least. I suspect it's the same elsewhere in Europe.

That seems counterintuitive to me. I'd expect only having one or two walls exposed to the outside (maybe 3 if I'm on the top corner) would reduce the amount of energy I lose to the environment compared to a house with 5 sides exposed. Plus a skyscraper can use a larger and more efficient system than a single family home.

Right, but your family home is likely insulated to at least R-13 in the walls and R-38 or better in the attic while an all-glass skyscraper is probably something like R-2. A tall & thin skyscraper also has an uncompelling surface to volume ratio.

When will it finally crash? Housing prices has reached a level of nonsense again.

Back in 2007, there was a report of some guy spending an astronomical $800,000 USD for a house somewhere outside of Silicon Valley, like in Tracy, I think. This was bonkers back then.

But now, nobody bats an eye anymore, and thinks it’s perfectly normal to spend that much on a house in previously economically depressed areas.

QE has impoverished us all (except for the fat bankers).

What is the black swan event that will finally trigger the stock market melt down? The price of SPY has gone exponential. A look at it, and it appears to defy gravity. But yet, everyone is celebrating on the streets it seems, as if the good times will finally last forever.

It will not crash. There maybe a temporary double digit dip in prices described in hyperbolic "end of the world crash" terms to demand government intervention to prop up prices. But without large social-economic change, land/housing prices will quickly recover and continue to outpace wage growth and many other productive investments.

We have shifted to an economy that increasingly favors rent seeking in every field and land is quintessentially that. Even without that trend, land reform meets enormous resistance under any circumstances but given that shift, even more so now.

Note that we know people will endure housing conditions seen everywhere at all time up until the 20th century, and unless the people hurt[1] by this do something remarkably effective, that state of affairs is guaranteed to return: there is no invisible hand guaranteeing even one family per room let alone per unit.

[1] disproportionately wage earners and the young but also all paying rent and mortgage interest.

> land/housing prices will quickly recover and continue to outpace wage growth and many other productive investments

Saying land/housing prices are outpacing many other productive investments seems like a stretch. If you look at the performance of large US REIT ETFs versus market indices like the SPY the rent seeking behavior by real estate investors doesn't look so profitable.

I can't claim expertise comparing particular funds. But for example, hasn't Vanguard's Real Estate EFT outperformed the S&P 500 by a wide margin?

And beside serious investors, for the typical individual, a home loan allows them to leverage funds that are unimaginably beyond what they could raise for investment with vastly more safety. Not that I suggest it would be better if half the population could and did buy stocks on unlimited margin or the like.

I just want to point out that even on this one particular issue, we gradually made policy and decided and made it such that one kind of loan is vital and the other insanely too risky. That at this point, this is so ingrained that it's hard to imagine any alternative. But I suggest we should probably try.

> And beside serious investors, for the typical individual, a home loan allows them to leverage funds that are unimaginably beyond what they could raise for investment with vastly more safety. Not that I suggest it would be better if half the population could and did buy stocks on unlimited margin or the like.

This is a very important point. Buying real estate is the most accessible way for an average-income household to get leverage - at least in the US where heavily leveraged financial products like CFDs are not easily accessible (at least to my knowledge). But in my opinion this another argument against investing into real estate because lots of uninformed buyers are in the market with increasing amounts of leverage leading to rather dramatic boom and bust cycles (like in the housing crisis of 2008).

> It will not crash. There maybe a temporary double digit dip in prices described in hyperbolic "end of the world crash" terms to demand government intervention to prop up prices.

This is probably true. In the short-medium term housing will not be allowed to crash for the simple reason that homeowners vote. The soundness of the economy in general will be sacrificed to pump house prices.

This feeds a feedback loop that makes housing an even more attractive place to park capital, further driving up housing costs.

Of course eventually this gets so unbelievably ridiculous that we have some kind of revolution. Look for $2m starter homes before that happens.

I’m hoping for a less drastic resolution, like people voting left-wing parties whom will more or less cap rents/increase capital/estate taxes to even things out a bit. Would you not see this possible?

I don't see how that is a resolution. Increased taxes mean more expensive housing. Capped rent means less available housing stock which will be fine for the first 10 years but over time more people come to the location and drive up prices again.

There are two things you can influence either supply or demand. You're reducing supply but keeping demand the same or allowing it to grow. The answer is to increase supply and reduce demand.

The thing is, the places that are supply constrained have optimized themselves into being in extreme demand. They know they don't have enough housing but that doesn't stop them from building more commercial real estate to enable new businesses. Those businesses could have been founded somewhere else but why bother when the most suitable city still has enough room for you (but not for the employees)?

That depends. In Barcelona prices peaked around 2008. Then went down at around the same rate that they went up at. Until ~2013 Then went up again. Is that considered a crash?

in '08 it certainly was. this is not "important" if its your house - since you live in it, values could go down to zero - who cares? you still need a place to live in. It becomes very important if we are talking investment.

I don't think that makes much sense in a country that's population is growing. People need to live somewhere and increasingly its in cities (where most of the price growth seems to be happening).

I tend to agree with you. Land and housing are still very cheap in rural towns in the midwest - they've moved no more than 2% / year or close to the reported inflation rate.

So why are homes so expensive in urban areas, including now tier 2 and tier 3 cities, and not just NYC, DC, and SF?

Look at our population growth. In the 'good times' of the 1960s, we had 180M people. Now we have double that in two generations, or the difference between Boomers and Millenials approximately. In 1960, places like SF and Arlington, VA weren't rural farmland, they were still urban areas. We now have higher density in the large cities due to jobs having moved there, so we probably have 3x the number of people desiring homes in the same area as we had in 1960.

And families are smaller now. In 1960, you'd have a family of 5 in one house. Now you need two houses for the two 2.5 / person families.

So essentially we've probably got 4x the demand for the homes close to working centers, along with rising base prices due to far more women in the workforce. Add perpetual low interest rates, underreported inflation, and I'm surprised houses aren't at SF levels in every city yet.

Many of those cities are only in the last few years returning to their peak populations. They certainly aren’t more dense, but there are fewer units of housing available now. In many places lots of housing was torn down, or multi family homes were turned into single family homes.

The cost is directly related to the fact that it is defectors illegal to build new homes in the most economically vibrant zip codes.

Go back to the 70's, San Francisco was losing population. By the 90's it had dropped from a peak of 775K (1950) to 670K (1980). It's now ~880K, so only 14% higher than 70 years ago.

What we have now is much worse than a housing bubble. We have a severe housing crisis caused by lack of supply, regulation, zoning and thus costs to build.

The difference is: Even if no one can afford housing: There doesn't have to be bust. For example: if there's only 9 houses on the market, there only need to be 9 people willing to buy in at that price. So, essentially, with a severe housing shortage, only the richest 0.1% need be able to afford the houses on the market and they can still maintain an extremely high prices.

Meanwhile the coping mechanisms are in full effect:

1. longer and longer commutes causing ever more CO2.

2. multiple generations living together

3. roomates bunking together, not having families, not having kids

4. decreased spending in other areas as every last dollar goes to housing

5. ever more louder cries for rent regulations which makes it even hard to build more supply thus resulting in a death spiral.

More and denser and with new public transport to go with the new denser neighborhoods. It's really not a hard problem if you take the city-politics out of it.

It's bad fiscal policy that's leading these trends. Our government has a huge deficit and huge debt. QE is essentially money printing, but rather than simply printing money, they (central banks) take equivalent value in assets off the market until they can be repaid the money to destroy. As so it has the same affect as inflation in the form of asset price bubbles until said money is destroyed. A large part of the FED's balance sheet is composed of mortgage backed securities and government debt, and it continues to grow with the repo stuff going on now. Other central banks around the world have been doing similar things...

When will it all end? Not sure, but the way I see it, there's 3 ways things can play out...

1) It will not end, and we continue to accept runaway inequality, where housing/healthcare/education etc. become more and more unaffordable in comparison to normal wages. Only owners of capital will be protected (i.e. stocks/assets continue to get propped up).

2) We somehow turn ship and slowly fix our fiscal problems (not going to happen so long as we have deficits). This would mean accepting economical stagnation for a long while to essentially pay off our accrued debts

QE has been horrific for banks. Net interest income has collapsed. it's less pronounced in the US, but in Europe where central banks have taken rates to 0 (or below) bank profits have all but been wiped out. Take a look at the share price of any European bank since 2008

QE and low rates has been bad for the banks, in a perspective of having kept them all alive.

Think about the Euro crisis as another example. Zero rates and ECB buying all the sov and fin debt bailed out banks that would have gone under.

If 30% of the banking system collapsed, then surviving institutions would probably have profitability consistent with historical rates.

But keep everyone alive, and bring rates to zero, and you squeeze margins both with excess competition, and compressing the diff between the rates they lend and the rates they borrow.

It hasn't reached that level of nonsense again. In 2006, the median price of a house was 5.1 times the median income. Today it's 4.4 times median income, which is high compared to most of recent history, but is actually lower than it was in 1955.

Nobody thinks SPY is going to keep increasing forever. The conventional wisdom is we're looking at a recession in the next 1-2 years.

You know there's something seriously wrong with the state of the housing industry (how it's regulated, zoning, etc), when our only hope is to hope for a Recession or worse.

People have been saying a recession is 1-2 years away since 2012. Statistically, it's getting more likely this 1-2 year recession pans out with each passing year. But no one has a crystal ball.

Economies don’t follow a random path with each year like the a ball with each spin of a roulette wheel. A driver of business cycles is accumulated malinvestment and suboptimal policy.

Another way to look at it is that a gambler can’t do anything to affect the roulette wheel, but a recession can be brought about or deepened by all sorts of human action.

The S&P 500 has more or less, always gone up, for its entire existence. From the late 50's to today, the CAGR was 9.97%. That's including the recessions.

At risk of stating what I think is the obvious: Either when the faithful change their minds, or when the USD is no longer so devalued. Money is based on faith, as well as the value of other assets like real estate (including precious metals).

I purchase multi-family rentals to be short the US dollar. My assets slowly gain value (while cash flowing) as the Federal Reserve continues its stimulus efforts (currently called Not-QE), which in turn devalues the currency.

If rates go up, I have also locked in a lower rate of financing using the banks money, typically 75% where I invest. And we hold our properties for the long term, as we get tax consideration for almost 3 decades. Depreciation is a powerful tool to amass an investment base faster, and 1031 exchanges can postpone the tax from sales of the properties if and when we do sell. Lastly, that event would be similar to the game of Monopoly, i.e. trading in 4 houses for a hotel.

Another merit is positive cash flow is now. If I were to continue to enjoy financial deals like I negotiated for our first 4 doors, $600K is all that is needed for control over enough assets to bring in $8K a month in cash flow.

In the US, currently cash flow/investment returns can be received with a lower tax base than earned income, again making it more powerful. Subject to change, of course, but I work with what exists now and hopefully let the future work out how it will.

There will be corrections, local crashes, but global crash is very unlikely. Land is one of the few resources that's 100% constrained in the world - we can have renewable energy, plant trees, produce drinking water, etc. But land - nope (except for very small areas of artificial islands/peninsulas, but that's insanely expensive, and also - limited). At the same time - world population is still growing, and people are being lifted out of poverty results in more of them moving to the urban areas, and increasing demand for the land there.

In high cost areas most of the value is in the land, not the house.

I don't know what it's like in other countries, but in the US the federal government owns 27% of the land. I wonder what it would take for the population to demand the government divest.

but it doesn't have to be that way. We're using up barely like 2 or 3 percent of the land in the US. We can simply build more cities and there will be more than enough land for everyone. by artificially keeping people penned into a limited area of land like a bunch of chickens in a crowded chicken pen coupe, we're only hurting ourselves.

The key is:

1) companies first (with tax incentives they'll do or move anywhere).

2) jobs next

3) Where jobs go, people follow.

I think it’s now time to outlaw non-primary residences.

And you can’t just tax them on it, because they’ll just push that as increased rents on their tenants.

They must divest, and release the housing unit, and sell it to someone that will actually live in it. And they cannot be allowed to do some other shenanigans to circumvent the spirit of this law.

In my condo, there's a bylaw that new owners must occupy the unit for one year, in order to discourage speculators and try to maintain a high percentage of owner occupation. While there are definitely efforts to skirt it, it does seem to mostly work.

Imagine if entire neighborhoods could create such ordinances. Prices would surely begin to trend downward, providing access to home ownership in desirable areas, allowing those with normal incomes to purchase starter property and begin families.

It seems like that number counts "paying a mortgage" as ownership. It would be interesting to see the figure for "fully paid off homeownership percentage". I'm betting a huge portion of that those homes are actually owned by banks.

USA real estate is number one market for money laundering. Very easy to setup an LLC and buy up properties through offshore entities without raising any red flags. Cartels, mafia, dirty politicians etc. invested heavily in Real estate in USA in last two decades. Specifically in San Fran, NYC, Boston and Miami.

QE has been fantastic for the capitalist class, and the ruling class.

But for the rest of us, it has made life a living hell on Earth. A survival of the fittest.

Life is now a reality of Mad Max sitting behind the steering wheel of a Prius, driving for pennies a day, if you can even make a profit after all the hidden expenses.

Life is now a fierce competition for resources, where you can’t even make your rent, or afford to start a family, or even to have children.

Meanwhile, the rich just laugh at you: “Here’s a dollar for your tip, see I believe in trickle-down economics.”

The lucky ones were those in the right technology companies, or those with the right medical or professional certifications.

Because of QE, there is now more homelessness. Even with people who shouldn’t be homeless.

The rents are much higher, and have kept pace with expensive mortgages. The landlords raised the rents just because they can. The rents in some areas can easily exceed $3000/month. This squeezes the rest of us that couldn’t afford a house before 2007. And after the crash, nobody was getting any mortgages, after they locked down all borrowing. And now, the higher rents eats up our earnings, that reaching that 20% down payment is an elusive dream. How do you even save for 20% of a $700,000 house ($140k), while paying your rent and bills?

The price of a house seemed to have gone up on average about $50,000 per year, for the past 4 years! Can most people even save up this much money a year? The same house that was listed for $500,000 just 4 years ago, in 2016, is now listing for $700,000 today. And there wasn’t even any renovations done on it.

Because of QE, the interests are so low, that it jacked up prices for everything: housing, stocks, education.

If you had $100,000 sitting around in cash after 2008, and was daring enough to plow that money back into the stock market and sit on SPY, then today, that net worth would be $270,000. Not bad, you would’ve made a cool quarter million.

The problem is that the capitalist class had $10 million dollars sitting around in cash, and if they aggressively plowed all that money into stocks, then they would’ve netted $27 million instead!

And some may have done that with their own money. But the way the capitalist class did it instead, was through their companies, with the share buy backs. They took public money, easily printed by the Fed, at low interest, to buy back shares to reduce availability, to force a supply and demand run. The stock goes up, it looks nice on the quarterly balance sheet, and they pay themselves a very very nice bonus. Which they then use to buy up real estate assets, in the form of LLCs and special corporations. They were the fox guarding the hen house!

This is the key thing that is driving inequality. And with the refusal of cities and governments to build more housing, to meet public demand, then it forces this situation on the rest of us. The rest of us are forced to compete, when the game is rigged against us.

So to the question of who are the winners in this QE fiasco? It is certainly not the normal people. It is the capitalist class. The rich, the wealthy, and those that own the corporations, and make all the rules.

When will the normal people rise up with their pitch forks and torches, and realize what the capitalist class has done to them?

Oh well, I guess they’re too busy drowning their sorrows in their iPhones, Facebooks, YouTubes, and instagrams, to bother seeing what has been done to them.

My hypothesis is that all this QE will eventually show up in terms of higher inflation. A ton of money has been pushed into the market and yet amazingly, inflation is still incredibly low.

If inflation doubles to ~5% (which is closer to the historic norm), interest rates will also rise to ~6% (again, a historic norm). Suddenly, people who could swing an $800K mortgage, can now only do $600K (keeping payments the same). That will have a huge impact on housing prices.

I doubt it will crash (50%+ drop in price), but no doubt we'll see some sort of slow burn, where houses drop 10-20% over a 5-10 year period.

Once income catches up with prices, we'll see a recovery.

> When will it finally crash? Housing prices has reached a level of nonsense again.

2007 was not about high housing prices. It was about ridiculously easy mortgages and everyone was able to afford a house outside their genuine payback limit.

The symptoms can appear similar, with different causes.

> QE has impoverished us all (except for the fat bankers).

What is with Americans who continually fail to understand that there's a world outside of America?

The link is about global housing, not just the US. That means an explanation can't rely on US-specific excuses.

What's your explanation for how US quantitative easing drives up house prices in Sydney, Hong Kong, and London but doesn't affect Singapore, Berne, or Munich?

> The link is about global housing, not just the US. That means an explanation can't rely on US-specific excuses

QE is not a US-specific phenomenon, either in origin (other central banks have engaged in it) or in effect when the US does it (given the US dollar’s global role.)

When the Fed prints money to give it to bankers (or whoever gets it), the recipient isn't constrained to spending it in the US. They'd invest the money where they expect to get the best returns.

qe is just overnight rate maintenance in the post-2008 world

if you're looking for a 'black swan' economic collapse event, look for a lot of outstanding debt and the possibility of an interest rate spike on that debt

Not at all. Median household income in Kansas City is $45,000. The median home price is $192,000 (4x income). Median income in San Francisco is slightly over double at $95,000. But the median house price is more than quadruple, at $1.7 million (18x income). Median household income in Manhattan is $85,000. Median home price is $1,000,000 (11x income). DC is a bit better. Median income is $85,000 and median home price is around $620,000 (7x income). Of course it goes without saying the median house in Kansas City is bigger than the median houses in those cities.

Also, the income difference is less than a factor of two for the same person. 57% of people in San Francisco have a college degree, versus 45% of people in Kansas City. So part of the difference in median income is due to the difference in education, not the difference in local salaries.

> Plenty of people who aren't doctors can make doctor money now. Just look at tech.

> Plenty

Plenty of tech folks make north of six-figures and often do better than most, but neurosurgeons make $800k, and plenty of mid-level medical types can pull $300K+. I personally know a dentist making "in the ballpark of 400" (his words) in the Washington DC 'burbs.

There are certainly IT/CS gigs paying north of $600K -- they're discussed all the time here on HN -- but those don't really exist outside of SV and maybe a handful of other areas, and generally require a pedigree that, while not a Med School, are still fairly non-trivial.

Your ITT-Tech trained Active Directory Admin isn't going to make anything near GP or Dermatologist money -- most tech, even with real degrees and certs, wont.

Specialized surgeons in the US are the top 1% of the field, especially if they own their own practice. That's really not a fair comparison. Especially when you account for artificial control/capture of supply and demand through the American medical system, which includes everything from schooling through residencies, all the way up to employment and licensing.

Lots of doctors make under $200k. I would say the majority do, because the majority don't own their own practices (partly nor in whole). Most doctors in the US are just salaried internists.

I think more than 10% of SWE with experience in the US are making that much or more when you account for compensation that is not pure salary.

> I think more than 10% of SWE with experience in the US are making that much or more when you account for compensation that is not pure salary.

I live in a big US city. We have one large tech employer which pays engineers ~125-150k (they max out at 200k for principals in specialized areas). At almost every other company in town, the going salary for a developer is 80-100k.

The latter type of job is far more representative of engineering jobs in the country. We told everyone "go do STEM and make bank at Google!" Meanwhile there aren't enough of those top-end jobs to go around, and a lot of folks who didn't go to a name-brand university or have friends in the right places work for (comparatively) little money.

Physician average was $300k in the US https://www.medscape.com/slideshow/2019-compensation-overvie.... I hate to say it as someone in the tech field but they have us best in compensation. Any suggestions how I can bump up my compensation as a junior developer in low col area without a fancy uni degree?

The problem with comparing doctors to techs, is that while a senior software developer may make as much as a doctor’s salary (from 10 years ago), instead, the doctor’s salary (of today) has easily kept up with inflation.

An Anesthesiologist makes over $250,000 annually. Try making that as a senior tech.

A Physician’s Assistant makes over $170,000 annually. Easily beating an average senior software engineer. And they’re not even medical doctors.

Nurses make over $125,000 easily, especially with their mandatory overtime schedules baked into their union agreement.

And here’s the kicker: because women make up a larger share of medical professionals, then you have a situation where doctors end up marrying other doctors or nurses. Which is good for them, but guess what they do? They buy up the expensive houses. And then they buy their second or third houses, thus pricing normal people out of that also.

Maybe in California, but most of the US is not union and most nurses do not make anywhere close to this. $30-40/hr is much more typical. That salary is far about the top 10% of nursing salaries (which is $106k).

If the GFC was any indicator, it won't ever really crash. The US government will always backstop this market. Too much of people's lives depends on this asset

US high school enrollment increased 1-2% every year from 1990 to 2007, after which it went down, not recovering for a decade.

The median first home purchase is at 33 currently.

Combine those two facts and you have demand for a first home peaking between 2035-2040. Add on top of that the older boomer generation peak dying or otherwise vacating homes and the effects of significant immigration backpressure and you have yourself a housing crash which will likely get priced into the market before these peaks happen.

That could well be round two as it is far enough in the future, the first round being the current global political breakdown and long running bull market reaching a tipping point.

I'm not sure how you get from those stats cited to a first home demand peak in 2035-2040. Class of 2007 grads are ~31 now. They want to buy now, not in 2035. Did you mean to type 2025?

1) Realize that this was back in 2007, when most people only dreamed of making $100,000 USD annually.

2) And housing prices were exceeding $500,000 USD in most of the state of California, because of all the shady house flippers borrowing on the ARM (adjustable rate mortgage) loans. So $800k was a significant percentage higher than most already over-priced mortgages at the time.

3) In order to qualify for a normal 30-year fixed-rate loan to buy a $500k house with 20% down, then you’d need to make an annual salary combined of $120,000. And since most people didn’t make that much, then you’d have to be dual-income to afford that mortgage.

4) And there was a saying at the time: House rich, but home poor. Meaning that these people bought an expensive house, but they were too poor to fill it with any furniture.

With faster connection to residential areas at the periphery of commutable distances becoming more and more common remote working opportunities are growing.

This is already having a huge impact on working in western Europe, and the more prevalent it becomes the more normal it will be to work from home, reducing the demand for proximal residence.

The example of Tokyo is showing that even if the population decreases, the urban center can keep growing for a while because of the benefits of urbanization.

On top of that, I anticipate growing displacement due to climate change. This is not the time to slow down home construction.

It's hard to compare Tokyo to other places -- it's a global mega city that is only comparable to a handfull of other global cities like LA, London, HK, or Moscow.

>QE has impoverished us all (except for the fat bankers).

Tech people crying foul about "the bankers" making them poor them is hilarious. Easy money is big reason the industry is booming; it's made you rich (by any reasonable standard).

It's difficult for me to describe tech workers as "rich" when the majority of them don't own any significant assets, like houses. They're a perpetual renter class with high income, the majority of which immediately goes to paying taxes, rent, and services that are more expensive where they need to live in order to earn those high incomes.

We've got a LOT of runway before the "big one" in the US. In other countries (Japan, Italy, some parts of France) the slow decline is already well underway.

The answer to when the big crash happens is in the population data. At some point population starts to decline.

As with everything, the boomers will ride in the sunset with bags of gold. In 30 years housing will be fundamentally different in the US and just about everywhere in the Western world. Outside of the major cities it won't even be much of an investment anymore.

If you buy a house today for $500k on a 30-year you'll spend close to a million dollars before you own it if you ride the loan out, and adjusted for inflation, you will probably take a loss on it. Possibly a large loss. Unless we see mass immigration the market 30 years from now is simply going to be smaller.

If you buy a house today for $500k on a 30-year you'll spend close to a million dollars before you own it if you ride the loan out, and adjusted for inflation, you will probably take a loss on it.

What's the basis for that conclusion?

Just like the last 30 years, some markets will decline, while others will appreciate. Not sure why you think things will be so drastically different.

Because population growth is decreasing in almost all western nations. Our models don’t really have good data for this since it’s never really happened since we started modeling off census data.

How does population growth affect my note? My amortization schedule is fixed and I know exactly how much I will pay to close it out, unless I choose to change that in some way.

> If you buy a house today for $500k on a 30-year you'll spend close to a million dollars before you own it if you ride the loan out, and adjusted for inflation, you will probably take a loss on it. Possibly a large loss. Unless we see mass immigration the market 30 years from now is simply going to be smaller.

It really depends where your $500k house is located. "Location, location, location" is the saying for a reason. If your home is in an area with continued economic opportunity and growth and it has not been destroyed by climate change related severe weather events, it doesn't matter that much what the macroeconomic housing market is doing; your property will be in demand.

30 year mortgage rates are around 3.65% this week. So if a buyer puts down 20%, that will be around $259k in interest over the life of the $400k loan, putting the total interest at half of what you said (~$760k total the life of the loan versus $1 million).

While certainly the US population is aging and slowing in growth rate, I have not seen any predictions for a population decline by 2050 or even 2100.

You are right that further urbanization is expected and buying outside of cities may not be a good investment.

Mortgage interest rate deduction is much less important since the standard deduction doubled under Trump. There's lots of home owners will will take the standard deduction now.

There is no indication I can see that these trends will reverse. If anything it seems like the rates of decline may accelerate more rapidly like they did in Japan.

Perhaps when the boomers die off the next generation will open the borders so someone can pay for their entitlements. Perhaps.

Ok, so something has been bothering me ever since I started thinking about housing in an economic sense. Housing prices seem to consistently rise faster than inflation over long periods (at least in large/medium metros). This means that housing is currently more expensive to people than it was 30 years ago. So what happens 50 years from now? or 100 years from now? Who will be able to afford to buy a house? Will people spend more than 50% of their take-home pay on mortgage payments? This doesn't seem sustainable long term.

Thank you for those links. My underlying assumption was that wages grow close to inflation, but obviously that may not be the case, so getting direct wage numbers is much better. Its interesting that the home price to income ratio is climbing back up after the recession. It looks a bit ominous.

> Who will be able to afford to buy a house? Will people spend more than 50% of their take-home pay on mortgage payments? This doesn't seem sustainable long term.

The US housing market is open to bidding from the richest people in the world. Wealthy people in other countries see US housing as a good way to store value, and are driving up housing prices. To answer your question: while Americans will be priced out of the housing market, wealthy people from across the globe will continue to buy into it.

Can someone point me to statistics about this phenomenon? It sounds true that foreign investors use US housing as an investment and inflate prices, but I have no idea how large this effect is.

For reasons pointed out by another reply to your comment, it's difficult to quantify. Anecdotally, I live in newer construction in a suburb of Seattle. At first the neighborhood was populated by local people who live and work here. As the original buyers have been moving out of the neighborhood over the past 5 years, the buyers of literally all been foreign Chinese. All of the houses surrounding mine are now occupied maybe 50% of the time, and I see luxury cars with Chinese license plates parked in front of these houses all the time.

There may not even be statistics - Canada doesn't have any comprehensive foreign demand data - that accounts for multi-unit demands for recent immigrants (now citizens or PR) acting as proxy buyers for third parties to evade taxes, and various other reporting gaps that exist.

So it mostly comes down to relative wealth & population sizes versus desirability of an area, and then spillover effects into surrounding areas. But unless China crashes I would expect this to be an increasing source of demand over time, especially if you live in a pro-immigration country that needs to paper over domestic government budget shortfalls.

That's basically the direction, yes. It's like healthcare in the US: Since people can't opt out of it, the system continuously optimizes for taking as much of their income as possible for the same good.

I started shopping for a home a few years back, and I noticed something interesting: prices had adjusted so that the total cost of owning (including mortgage interest, taxes, maintenance costs, etc.) was almost exactly the same as the total cost of renting! It didn't matter what I did; the choice had been reduced to "Do I want to make a leveraged bet on the housing market, or not?"

I did. That bet was basically a wash when I sold last year. After final calculations... I paid within $100 a month of market rent for the place.

The only way you can get out of the trap is to acquire enough cash to simply buy outright (and then hope you never get the itch to move). And, of course, then that money is locked out of the investment market.

I did that a long time ago (not in the US) and owned the place until a few years ago, when I radically misjudged the market and ended up selling it at the bottom. Oops.

Now I own a nicer and much more valuable place, with a mortgage; I may be able to keep it and pay it off, or I may have to sell if I ever want to move.

For me personally, the lesson was that I want to own outright, or if I can't do that then rent, and I think I can do that for the rest of my life subject to some obvious limitations.

Mostly because of the mobility trap presented by a mortgage.

>It's like healthcare in the US: Since people can't opt out of it

We do not have a national healthcare system as most of the world does. We are not forced to have healthcare. Yes there are provisions of Patient Protection and Affordable Care Act that charge a tax penalty if you are not covered or exempt.

I always thought the bet is not rent vs mortgage, but whether or not you can sit out the mortgage. Of course it's cheaper to rent if you plan to sell within twenty years.

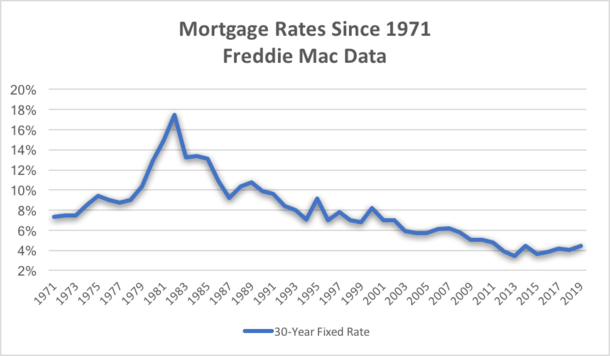

It's true that housing is getting ridiculously expensive. But there is a side that's often not really told, or really explained well, which is interest rates dropping consistently and hard.

(ignore the weird domain, there's plenty of similar sources).

Fact is that rates used to be as high as 18%. Recently they've gone as low as 3.5%.

Real estate is hugely debt-driven, and the standard mortgage contract is set for 30 years. Thereby 'housing costs' isn't really reflected in just the price of a home, as say, the price when you buy a banana, which you buy instantly with cash. Instead, housing costs are dominated by the financing costs, which you pay for over the course of 30 years.

Those housing costs have price as a major factor, sure, but it's multiplied by interest rates. You can't leave that out of the historical context. And if you do, housing costs have in fact not increased quite as sharply as people think.

To illustrate, a $100k home with 3.5% vs 18% rates over 30 years, will cost $160k vs $540k.

In fact, a $333k home at 3.5% rates, will require total payments equal to a $100k home at 18% rates, both around $540k. In short, prices could have tripled since the height of the mortgage rates until the bottom, and yet, you'd have made exactly the same total and monthly average payments.

We often get shown price to income graphs getting worse and worse. But that doesn't capture the reality: monthly payments aren't getting nearly as bad, as interest rates have dropped hard. Higher prices are easier to pay off.

That's not to say that housing isn't getting more expensive, it is. But if you correct for inflation (i.e., average income growth) and correct for much lower financing rates (lowering monthly payments), it's not nearly as bad as is often presented.

An easier way to look at this is the percentage of money we spend of our income on housing. You can see it's on the rise, but really, it's not as extreme as some would think. None of the doubling-tripling kind of figures about housing you see in the media.

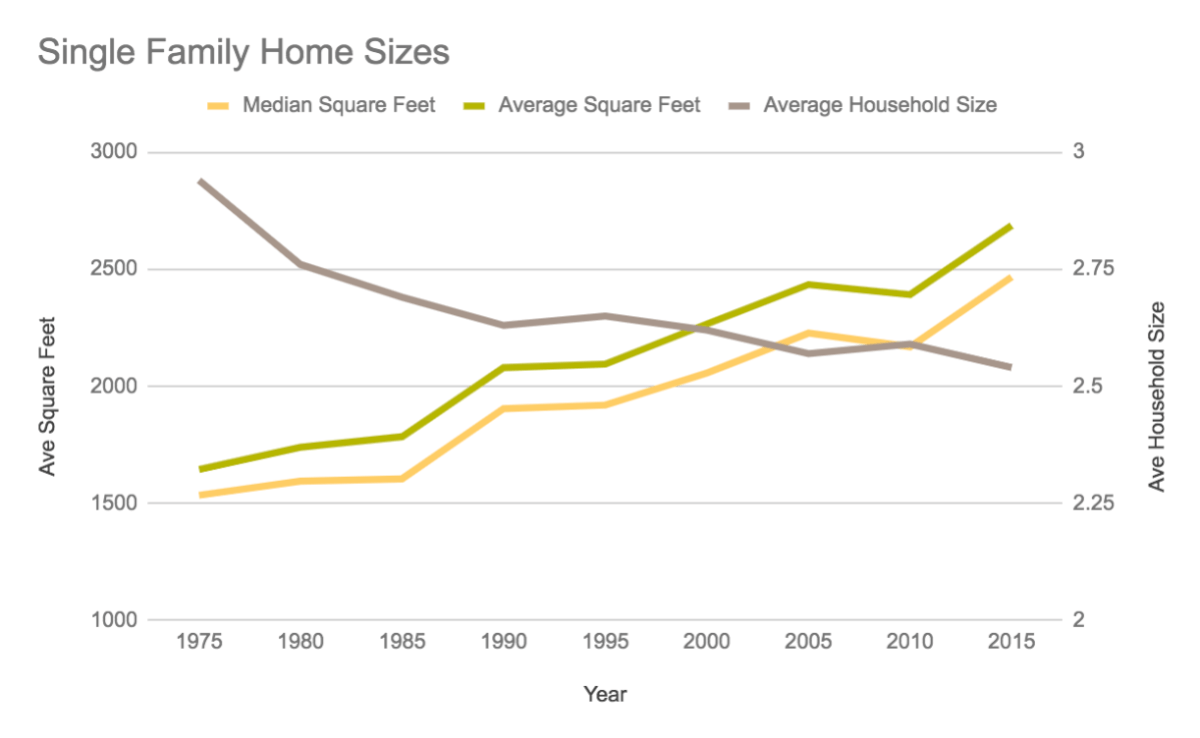

Then lastly, we're just looking at how much we spend, not at how much we get in return. Suppose phones got more expensive, nobody would bat an eye, the phone today is 10x the phone of 20 years ago. What about housing? Here too the data is a bit tricky to get, I'd love to see more research on this. But there are some figures about average home size:

The average home size grew from 1500 to 2500 square feet, while the average household size decreased. In short, in part 'housing' is not getting more expensive itself, but rather we're purchasing more of it, thus spending more on it. If you correct housing costs (i.e., bring it back to a $ per unit of house size), the growth is also much lower.

If you take all this together, then housing is still getting more expensive, but most places are not all that much worse than many years ago. That's not to say we should ignore this as a policy issue, I think it demands lots of attention. But I do think the media narrative and vox populi currently is blind to the other side of the story and only has one message: extreme prices, unseen crisis, lost generation, no hope, etc.

This is very important, especially when discussing it with people who rent. People who are paying 3000-3500 a month looking at a 1 million dollar house as something insane (well, it is, sorry I'm just using round numbers to make it easier for myself).

But depending on interest rates and property taxes, these might be almost the same thing, or very close. Once you consider the portion of the mortgage that goes to the principal, and if you assume some amount of inflation and increase in value, the 1 million dollar home might be cheaper, even if you consider that you could have invested the money in S&P (in this particular example the market would have to be in a fairly ideal state to favor the mortgage, but still, it's close, and you get to make holes in the walls without anyone bitching about it).

Homes are this expensive because, for better or worth, they're worth it. That's the problem. As long as they are worth it it will keep going up (and rentals as well as infamously AirBnB are making sure they're always worth it unless you push out an INSANE amount of supply, where incremental boosts in house building, rent control and affordable housing initiatives may make things worse rather than better.

What your analysis doesn't take into account is that if interest rates go up, demand plummets and the 1 million dollar home at 3.5% is worth 600k at 10% interest rate.

A big RE mogul used to say "Its better to buy a cheap house with expensive credit than an expensive house with cheap credit. You can refinance the latter"

When you have a $300k loan and refinance midway from high to low or low to high interest you will pay the same amount of interest in the end. The reason why low interest rates are bad is because everyone is bidding prices up. Paying $1000k at low interest for the same house is fundamentally worse than paying $300k at high interest.

Sure, but in the markets people bitch about that hasn't happened. Even during the crash, prices didn't move downward that much. There is a risk for sure, but that's true of all investments that pay better than t-bills.

We've seen a shift of preferences towards externalizing the risks of asset ownership to third parties. Many people today prefer to purchase a stake in a real estate conglomerate, and contract out the maintenance and labor, rather than own an apartment building outright and operate it themselves. It's an attractive option for the owners, but carries the risk of creating bureaucracy for the renters.

I think if we continue in this direction, we'll see a resurgence of co-op style ownership, where no individual can afford to purchase the 4 story brownstone in Brooklyn, but a board of 4 shareholders can.

If you want to buy a house for yourself to live in, you might be purchasing a vanishingly-small set of "living-rights" shares from a conglomerate. You won't have to pay for your hot water heater, but you won't have the right to repair or fix it yourself.

> If you want to buy a house for yourself to live in, you might be purchasing a vanishingly-small set of "living-rights" shares from a conglomerate. You won't have to pay for your hot water heater, but you won't have the right to repair or fix it yourself.

Life, Liberty, and the Pursuit of Happiness -- that's all you get. For everything else, you gotta pay.

One significant aspect of increasing house prices is increasing house sizes, amenities, and services (from an HOA). People keep buying more because they think they need it, and I think a return to spartan living would do well for the country but I don't see that happening for a variety of reasons.

The price of assets is directly related to interest rates. This relationship is obvious if you think about it. People borrow money cheaply, the more money that's available, the more money people have to bid up prices of assets. The way interest rates are (including negative interest rates across the globe) I doubt there will be a curb anytime in the future. The biggest unknown IMO is related to the status quo. Perhaps people will value freedom more than security and therefore won't chase those housing values.

For a growing city a house changes in definition. Eg in new cities houses are a 1/4 acre, then they get subdivided then eventually apartments. So the land can keep going up faster than inflation/wages and still a housing unit remains (relatively) affordable.

Also medium term affordability fluctuates so when a boom ends you often get 10 years of flat prices so its a drop after inflation.

Rent is probably cheaper than ownership, except for the investment component. Because the market isn't efficient here, and because of the asset growth, owners can get a positive return even if rent doesn't pay the full mortgage.

the "rule of thumb" is to rent out for 5% (per annum) of the price of the property. This is the unrecoverable cost of owning a property - 1% in maintenance, 1% in

property taxes, and lastly, the cost of capital (which, i've set it at 3% as an estimate).

If your rent is exactly 5%, then the landlord is cashflow neutral, and the property appreciation is what the landlord gains. If your rent is below 5%, it's a good deal, and if it's above 5%, you're getting shafted by your landlord.

Interesting. I have not heard this rule before (and I assume it's modified by the actual tax rate).

That said, unless the local real estate market is strong I don't think it makes sense as an investment to break even on the rent. It's a lot of headache and risk to bet on a >5%[1] average annual appreciation. I don't think that is a reasonable rate to expect in many (most?) real estate markets.

but TLDW; the unrecoverable cost of rent is just the rent money, and a lot of people compare it with a mortgage incorrectly. A mortgage is not 100% unrecoverable, but some portions of it is unrecoverable (the interest). The other unrecoverable cost of owning is the initial downpayment.

The 3% capital cost is the combination of the above interest payment and the lost income opportunity from the downpayment. Whether you buy out right with cash, or get a mortgage, you still end up paying a price either way (via interest, or via lost opportunity to deploy the cash downpayment).

That assumes a hot market where values are riding quickly. The math doesn't work very well if the value growth is around the typical 3% per year.

Also, if the value of appreciation really is that high I don't think it is correct to leave that forfeited value out of the "renting is cheaper" equation.

First, that's not entirely true. We just moved out of a half-duplex that we could have bought if we wanted to (the owners decided to sell it near the end of our lease term).

Second, in the case they are different kinds if properties, comparing them on cost alone isn't valid.

Yes, that was my point. Saying that renting is almost always cheaper than buying when the properties for rent are inferior to the properties for sale is meaningless. Renting the properties that are worth buying is not almost always cheaper, except in certain markets at certain times.

As someone else pointed out, people from all over the world, not just people who want to live there, can buy a house. That means a LOT of people can afford them even if they were a few times more expensive.

Still, the majority of homes are still either bought by people who plan to live in them, or by landlords who will rent them to people who will, so obviously some people can afford them.

Turns out, doctors, a subset of lawyers, various other high end professions including, yes, software engineers, make a lot of money, and there's quite a few of them. Add couples and families and you don't need everyone in the home to be able to afford it, either. Roommates can split the bills. DINKs end up with much more disposable income that can seem astronomical to more traditional families. Older people may have been able to accumulate wealth that seem impossible to 20something or even 30something years old. You can add a lot to that list of examples.

Even when you take away all of the outliers (like rich Chinese investors), turns out a shitload of people can afford these places (which is why if you want to use supply to reduce prices, you need to build a LOT before it goes down enough to reach the lower and lower middle class).

Also consider that 50% of your income (in an investment, no less!) when you have a family income of 250k isn't the same as when you have 50k. I'm fairly privileged, and if I gave up 50% of my income to housing (with a large portion really being a stored investment), it would still make a ton of sense financially.

For sure it shouldn't be that way: even if you were a rich selfish bastard, its easy to see how the people you're displacing are going to come back and be a pain in your butt (see San Francisco), so it's in everyone's interests (not just for social justice) to fix this problem. Still, it's this expensive because it's still worth it and there's still a ton of people who can afford it.

It really dawned on me when I last looked at the status of my mortgage and my savings. When I bought my place less than decade ago (so not as expensive as the market is today, but still when the market was red hot as the interests were at an all time low), it was a non-trivial percentage of my income, the downpayment was most of my savings, and we were definitely running the numbers to see what would happen if my wife or myself lost our jobs. It was tight. A few promotions, job changes, and favorable economic conditions later and I could almost pay cash if it was still at the same price it was back then. Early 30s me thought it was an insane amount of money, but 40something me wouldn't have much issue with it. That's the kind of economic reality and competition we're dealing with here.

turns out a shitload of people can afford these places

Yup! I noticed that in the SF market. With all the tech, biotech and finance jobs here, there are a lot of households with incomes in the $500K range or ~$25K per month after tax income.

A $1.5M mortgage is ~$6K, maybe $8K total including taxes.

That's only 33% of take home income for this hypothetical household.

I'm not on the west coast but was just reading an article a out the entry level salaries for software engineers at top tech companies in the Bay area. Many are really close to the numbers you used in your example, so it's well within the reach of these people if they are DINKs before they are in their 30s.

So to make a dent in the market price you need to have more supplies than there are tech folks. That's a lot.

Don't hold your breath. Kind of hard to find the exact figures, but median home equity is somewhere in the range of $30-150K. (Probably per-household, so divide by two?)

I'm sure substantial transfers do happen, but I've never met anyone that was so lucky.

The relevant figure is median home equity at retirement or potentially age of death.

The overall median would include 20-30 year olds that have only a deposit, 30-40 that are still paying it off, etc. They're not handing down anything for another 20+ years.

> HELOC's to pay for their assisted-living. So the transfer is from boomers to doctors

Eh, I did some work for nic.org. Assisted living is a real estate game, and the market reports are identical to apartment market reports. The medical bills go to Medicare and private insurance. Doctors aren't getting rich off Granny reverse mortgaging her house. Unless said doctors own an assisted living facility, preferably in one of the 30 major MSAs. I vaguely recall Florida being particularly attractive.

True, not HELOCs. I was thinking of Medicaid spend downs there.

It's been a few years since I've looked at it, but if you needed nursing home care, the typical advice was to spend down your assets in a hurry to qualify for medicaid. And in some circumstances, medicaid could put a lien on your home for post-death repayment of services.

Houses keep getting to be better quality. 30 years ago, houses were smaller, built with shittier materials, cost more to heat and cool, didn't have as many bathrooms, appliances, or wiring.

None of this is free.

Houses should be outpacing inflation under these conditions.

This is complete nonsense are at the very least, localised to you and you region.

2 bedroom, shitbox, shoe-box apartments are being sold for $1,000,000 in Sydney that are being condemned less than 10 years after they were built because of the shocking quality of their construction.

I'd go further than that, and say most of Metropolital Australia is the worst example of a bubble.

```

Over 66% of Australians live in the greater metropolitan area of Australia's 8 capital cities with Sydney being the largest (around 4.9 million), followed by Melbourne (4.5 million).

```

> Housing prices are driven by the people paying the price

Not sure how that relates to the Ricardian theory, but while prices are technically "driven" by the people paying them, this does not seem like a useful observation to me. This isn't "if you keep buying every next more expensive iPhone, Apple will keep raising the price". You can't just not buy/rent property. It is a basic necessity.

While prices vary between regions, that is still hardly a choice. Most places, jobs are scarce and transport is a disaster - you can't just go live somewhere else because your job is here (and most jobs are in high-rent areas).

This means that no matter how high* prices get, people will have to find a way to pay (even if that means basically starving for the rest of their lives) and landlords are aware of this, so they keep raising the prices with the argument that "people clearly have the money, so it's fine".

In theory, it makes sense for a finite resource to increase in price with increasing demand, but prices are increasing a lot faster than demand is and housing isn't as finite as land is (we can build up). This points to the supply side (landlords and developers) being the problem, not the people just trying to survive.

With the birth rate dipping, I'm wondering if this will self-correct when the baby boomer generation dies off and there is a larger supply of housing per capita.

It'll just go to their children and accelerate some fun inequality problems

eg: living in fancy inherited house with no mortgage but way out of your price range based on income. The "real" cost of the house then isn't what it's worth but what your taxes come out to be...

In California property taxes are not re-evaluated when a property changes hands by inheritance. So, they really aren't paying anything close to the actual value.

Which, lets admit, is just plain ridiculous. Prop 13 needs to be repealed or at least severely amended. Right now it is a wealth transfer program from the poor to the rich.

As more wealth is tied up in houses and houses are passed on to children, owning a house will become even more dependent on the wealth of your parents than your income.

Someone with a house they pay low taxes on but is worth several millions is unlikely to sell so housing prices will keep shooting up and exclude many people who simply weren't lucky enough to be born to richer parents.

But the trend is also that there are more people per household. I.e. I don't know that we can say that it's a 1:1 relationship that as the population grows so does the number of houses needed.

The other part people don't think about: your ownership of land is only as valid as your (or the government's) ability to enforce it. A lot of major civil wars in the 20th century have been fought over land rights -- in many cases, it has been local citizens seizing land back from foreign corporations and land barons. Many countries have laws on the books restricting land ownership to citizens as a result.

The US has also basically had unrestricted capital accumulation barely interrupted by war / mass societal reorganization (only the high tax rates around WWII and abolition of slavery) for over two centuries. Now that there is no more frontier there’s no more land that is both cheap/free and desirable

I'm a big fan of the folk wisdom that the power of housing as an investment is essentially a self-discipline mind trick. Paying your mortgage feels more urgent than contributing to a brokerage account, withdrawing home equity feels dirtier than withdrawing stock portfolio value, and holding onto your house during a downturn is easier than holding onto your crashing stock portfolio.

Once you know those things, you can rig yourself similar safeguards around other asset classes (automatic payroll contributions, tax sheltered accounts with early withdrawal penalties, etc).

There’s been some research lately about whether Private Equity outperformance is partly driven by the illiquidity making it harder for investors to dump their positions in a moment of panic. Your thoughts about housing illiquidity seem related to this concept. (If you’re interested, Matt Levine has covered it in Money stuff with links to the research papers).

In addition, we have affordable margin loans, mortgage interest tax deduction, property tax deduction to juice the system, not to mention additional legsilation like 1031 exchanges, prop13, etc.

Many of these were put in place as public policy promoting homeownership driven by the idea that homeownership would be less costly / beneficial to society compared to long term tenancy. That thought doesn’t seem to necessarily be wrong per se. but if you help out demand side legislatively while restricting supply legislatively, sometimes you’ll get cases of imbalance like we see in the coastal cities.

Given what we’ve observed in the last couple of decades around the world, a managed system like Singapore where property appreciates at a ~2% rate a year (and if demand suddenly shoots up, they’ll add transfer taxes or stamp duties or inject supply into the market) seems much more stable for society.

> There’s been some research lately about whether Private Equity outperformance is partly driven by the illiquidity making it harder for investors to dump their positions in a moment of panic.

There are apocryphal stories of studies purporting to find that the best performing investment accounts are those that belong to people who are either dead or had forgotten about their account:

Generally, even if one invested lump sums right at market peaks, just before crashes, you'd still get a decent returns as long money was not withdrawn:

2008 really showed that homeownership is no different than tenancy. Look at Detroit. Entire city blocks were owned by the bank simply because people either couldn't afford the mortgage, their loan was called due, or they thought the short term loss in equity wasn't worth staying in a run down place anymore.

I believe that the purpose for homeownership in the US was primarily to foster a competitive housing environment. That way landlords wouldn't control the majority of the housing market and people could help keep housing prices down per month by being able to have the ability to qualify for housing just as easily as tenancy.

It seems like housing demand is almost entirely a function of population growth. Supply is tied to a finite resource, land. We cannot do much to increase supply. The conclusion from this set of facts should be obvious.

You could if you wanted to, though for whatever reason people are much more comfortable with leveraging 5x to purchase a home than they are with leveraging 5x to invest in a brokerage account.

Nah, it is indeed much easier to invest in real estate on 5-10x leverage than doing the same with stocks or ETFs, because the banks are usually much more comfortable lending you the money in the first case.

I think it's because of the mind trickery that makes the first thing a solid "buying a house" investment and the second thing a "gambling on the stock market" game. You can easily see that trickery at work: just confront someone who bought a house on credit with the fact that he just put all his money into a highly leveraged single investment, which combines two of the usual "don'ts" from the "Investment for Dummies" book. You will usually earn blank stares.

Not saying that doing such an investment doesn't make sense in certain circumstances (use the house yourself and plan on staying there for decades), but one should be very clear about the risk profile of it.

This seems to be the benefit to me as well. The average person won't get a £100,000+ loan from a bank so easily for anything else.

Want to start a business with that money? Better have a rock solid business plan. Investing elsewhere? No chance, a bank won't lone that money for you to play with on the stock market, and the rate you would get would wipe out any gains from something safer like a tracker fund.

For anyone that is not content living in the same area for the rest of their life buying is a poor decision. But it is the only way most people can access a loan that size and leverage in that way.

I've resigned myself to the fact you have to buy (in my country at least), and I will just make sure it can be rented easily when I want to move.

Some European countries are much more renter friendly and I would consider renting exclusively there. Germany and Berlin seem more appealing in that regard with the rent control that was put into place recently.

The thing is housing almost comes with a rock solid business plan and as a basic need is somewhat resistant to radical decreases in price (it is almost impossible that your house would depreciate by 100% - company stock/your own business investments could).

With the way the market is it is likely that mortgage principal + interest + maintenance is actually less than rent...

Lots of things can drag down the value of a home to zero. Lack of maintenance or a natural disaster are two big ones, but also the neighborhood could turn to crap or an infrastructure crisis that isn't resolved.

Add to that property taxes continue to accumulate on buildings. There are quite a few ways to drive a house to worthless. I used to live in a region where houses were <$10k because they were condemned shells in crime-ridden areas.