I like the idea of a hot potato effect caused by taxes that match the 'real' value of an asset. This should apply not just to real assets (like houses) but the current commodity value of a 'future' in any other value.

I had desired such a tool relative to speculation on the stock markets (and at the time postulated that requiring whoever 'owned' a future __must__ receive it when it comes due); however the idea of taxing that invested value while it is held seems to be an even cleaner way of handling the problem.

In the Netherlands (and probably other countries too) this effect is used the other way around - there is a large tax on savings, from 1.6% to 5% depending on the assets, that actually incentivizes moving cash to more speculative investments.

Regarding futures, I was under the impression that's how it works - if a contract expires on your hand, you have to take delivery. There are a few funny stories around of that happening accidentally to paper traders.

I believe this works in the Netherlands because they have a robust pension system. Disincentivizing savings without having a good system in place for retirement would break a country in a single generation.

Savings in the US are not quite disincentivised, but not actively encouraged. You're only taxed on interest, the principal in a savings account isn't taxed.

On the one hand, as a person with relatively few assets I'd say it would be clearly in my advantage that there are no assets and all value needs to be produced by labor.

But at the same time it is also a natural desire that you build up something that you can use when you are old and tired. And that shouldn't necessarily be a lot, lot worse than what you are used to in your prime time. So in some regards we also need assets.

Probably the best way to do this that would actually be fair and as accurate as plausible would be to auction some sort of contractual instrument that pays out or charges the bearer depending on the difference between the sale price (whenever the land happens to sell again, if ever) and a predicted price (set by the auction). The land would be taxed at the rate established by the auction, and the instrument would be configured such that manipulating the auction on your own property is economically unfavorable. This would allow people with expertise in accurate land pricing to make (a bit of) money and remove any arbitrary or unfair pricing from a tax assessor.

For easily traded assets, it's easy; the owner sets the value and must accept any offers to buy above that value. There are obvious issues doing this with residences though.

That ignores sentimental value, though. I wouldn't want to be taxed a huge amount for my father's watch.. but neither would I be interested in selling it for less than a huge amount. It's certainly not worth that huge amount to anyone but my family.

I have seen people argue for it still working for other forms of property (most notably houses; I don't want to be forced out of my home) with the argument that if people set a value e.g. 2x what the property is worth, that will deter forced selling and then the tax rate can be lowered slightly to be revenue neutral. I'm less convinced.

Well yeah, in practice, we can say an asset's value is what the buyer and seller agreed upon for the price, but I'm asking about valuing it while it's being held for taxation purposes. This is easy for stocks, etc, which are homogenous units that have other sales going on all the time, but for a house, for example? Comparisons are hard in practice! No house I've bought/sold has come in at the government's valuation.

In the case of real-estate or other location dependent properties, there's often an assessment process of some sort.

As a simple means the government could also act as the 'auction house' for properties and entertain prospective bids on a property. The median of those bids could be used to set the asking price if it's higher than the last public valuation of the property (this is mostly to discourage front companies down-bidding to cheat taxes).

For more fungible items the current market valuation seems much more obvious.

I've long felt that the appeals process for a real estate tax appraisal should include the owner's option of, "Deal! I'll sell it to you [the city/town/county] for 90% of the value you just appraised it for, subject only to being eligible for a Certificate of Occupancy [which cannot be unreasonably withheld]."

Optionally, add a provision that, if the town objects, the owner names a new price for the appraisal that the town can either accept as a valid appraisal or purchase the property for 111% of the owner's figure.

In Vancouver we have the opposite: realtors call you weekly and promise you 1.4 million cash on the spot, while the tax value is 600k. Can’t raise taxable values to be realistic, as a lot of older folk are sitting on fixed income in multi-million dollar homes.

It seems that when prices move in this direction, you could raise the taxable value and simultaneously lower the millage rate so that the overall tax receipts are what the city needs.

This way, people whose properties have skyrocketed in value relative to the rest of the city would have their taxes go up slightly, those whose values have gone up but gone up by a relatively lower amount would see a reduction in taxes, and the city still gets all its revenue for operations.

If everyone's value has doubled (as an example), it would seem better to raise everyone's assessments by 100% and cut the millage rate by 50% than to have some weird half-Prop13 situation where 123 Main St is assessed at half of 125 Main St because 123 last sold in 1984 and 125 sold last week for $1.4MM in cash.

We don't have a land value tax in Australia. But I think we should.

> Can’t raise taxable values to be realistic, as a lot of older folk are sitting on fixed income in multi-million dollar homes.

In this situation, maybe we should allow retired/older folks to defer taxes until the sale of the property (kind of a government-based reverse mortgage). Would be messy to administer though.

>Well yeah, in practice, we can say an asset's value is what the buyer and seller agreed upon for the price, but I'm asking about valuing it while it's being held for taxation purposes

Hah, it's kind of zen - if a house isn't being offered for sale, does it really have a selling-price?

As a hypothetical, you could mandate that people put a value on their house, and then say "you must accept offers more than Nx that price - so say, if N=2 and you value your house at $1million, then if someone offers $2mil, you automatically sell.

Then, charge them tax based on their own evaluation. If they value it way too low for the purposes of tax fraud, then someone will just buy their house for said stupidly-low price and sell it at market-price for a profit.

I mean, there are all sorts of social problems with it (that might well sink it), but it seems like a pretty nifty solution to the problem.

and composite utility. Ie location, size, amenities, etc. A home near a good school will always have a higher value. Aka hedonic regression and valuation.

I understand what you're saying about selection bias, but he has given a reasoned argument, providing a model that matched reality in multiple places. You're response of "it doesn't always work" is without value unless it provides an example of where it doesn't work.

His prediction would carry a lot more weight if he had written about it prior to the recession. A lot of people can say "I predicted that" after it happened, but those who have proof they can point to have a lot more credibility. All he has is that he "won a bet" after a "conversation with a friend."

Unless he was wrote about it ahead of time, we have no way of knowing whether he also made a similar bet with another friend in a different conversation to say that housing prices were going to continue towards the moon. If he had also structured the bet in which he got his school payed for and seemingly no downside if he lost, then he could have guaranteed free school, and looked like Nostradamus either way.

So it's quite possible that this is selection bias at work, and he "flips coins" on a regular basis and only brags about the ones that come up heads.

Exactly. And even if you have one million people making only a single prediction. Some people are going to be right. Especially because a downturn is like a 1 in 20 chance if you go by years. So out of a million people having one guess at the next downturn, about 200.000 will be right and can brag about it, without having any higher understanding about what happened (even if they will staunchly believe they understood something, because they were right).

What I observe though, is not large numbers of people making random guesses and exponentially fewer being validated through random events.

The people who become notable are those who predicted an economic crisis, for decades before circa 2008, and once they got notoriety for that, have continued to predict doom for the subsequent decade. Eventually they either die or are right again.

I think the article is not about being right about something but more about the concept that s/he learned about it in a virtual (extremely limited) environment.

IF s/he was confident about the prognosis, making really money in the marketplace would have given leverage x-fold higher than a bet between friends would allow.

What he predicted was a correction to a housing bubble. Specifically, it seems, the Californian housing bubble.

There is nothing particularly special about housing bubbles and their correction. This happens all the time.

What he didn't predict was the effect that that correction in 2008 would have on the global financial system. That's because you'd need to include securitisation, how the big players were holding risk and the effect of perceived credit worthiness on short term liquidity.

A while ago, when I looked into this, I found just one paper, written prior to the crash, that could reasonably be considered to have predicted what occurred. Unfortunately, I can't find it, if I do I'll add the link.

And even if you did find something, how would you know if they were just lucky or truly prescient ?

Folks are constantly predicting gloom and doom. Some have even made successful careers out of it, their low probability of predicting such catastrophes not withstanding.

That's my point. The paper didn't predict bad things happening.

It specifically said that banks were holding higher level tranches of CDOs. Because they're MTM accounted they could suddenly drop in value if default rates increase. This, in turn, could cause other banks to suspect their creditworthiness and pull their funding lines.

In other words, it was very specific about what it thought a collapse mechanism was and it turned out to be spot on.

I don't believe they were either lucky or prescient. I think that they were well informed and joined the dots in a way that few others had.

I read a book prior to the crash that I consider an accurate prediction of what was coming.

"The coming crash in the housing market" by John Talbott

The author used a mountain of evidence and trends to back up the books premise, and going through it all it was hard to deny. Timing such an event though is always difficult, as exemplified by other books like 'The big short'.

Similar story: Card from realtor, offering a townhouse just like mine, but for over 2X what I'd paid four years before, and 3X what they'd originally sold for six years before.

Me to realtor: Is that a realistic price?

Realtor: I sold one just like it for that much last week.

Me to wife: Time to sell.

* - Along with a pile of other reading, it was the Robert Shiller 100 year graph of the relationship between house prices and income [0] that told me trouble was coming. Ultimately, most mortgages and rents are paid out of wage income, and there's only so much blood you can squeeze from a stone.

The intervening years have colored my perceptions. I'm uncomfortable with prices as high as they are... but it is clear from the interventions of the last ten years that the US government will pull out all the stops to keep the mortgage debt load in place. I don't know what breaks next - the 2016 election is an example of something that broke - but it probably won't first be the overall mortgage debt load.

Started reading short seller message boards. Got deep into the weeds with credit default swaps. Found that you could actually see prices for credit default swaps on markit.com. watched priced for BBB- credit default swaps increase dramatically in early 2007. That was the signal that it was over.

Got back in in early 2012 when the loan rate resets from the housing bubble all tapered off.

Moral of the story: in every bubble the money is coming from somewhere. Figuring out where it is coming from will let you predict the big market turn. If you don't know where it's coming from then you probably shouldn't play with bubbles.

I don't think housing is in a bubble except for the Bay Area since new home sales are in a relatively normal range currently[1].

As far as the Bay Area goes it appears to be trickle down from FANG stocks buying up VC backed companies and the associated recycling of those proceeds into new ventures. There's also a bit of China money buying up single family homes, but China has been putting steady pressure on all that trying to plug those foreign exchange leaks, so if anything that's waning.

Where's the money for the stock market coming from? It used to be quantatative easing and FED reserve bond buying. I guess the yen carry trade in part and probably lately tax cuts a bit. It's harder to see where the money is coming from in the stock market though because buyers are largely anonymous.

You may be right but without context or the background for your educated guess that comes off as a snarky flip.

I would personally add Russia to the mix. The reason is simple: both China and Russia are sources of capital flux, where those with means are funneling funds outside their respective countries.

Because there are, or have been, capital controls in place, those who move money out of their countries are willing to pay a premium for it. Funnily enough, there is a name for the phenomenon where actors with money are willing to pay exorbitant transaction costs in order to move funds from one jurisdictional domain to another.

Russia's economy is not that big. About as large as Italy. I seriously doubt they are fueling much except a few oligarchs buying very expensive homes here and there.

Similar story. During summer vacation in the mid 80s, a Chinese guy from Hong Kong came to our door in NYC and ask me to tell my dad that he wanted to buy our house.

I took his card and said “sure”. As I closed the door he said “wait”, ran to his car and grabbed a Miami-vice style aluminum briefcase. He opened it up and said “400 thousand dollars for house, see?”

Given that my folks paid like $18k for the house about 8 years earlier, that was pretty amazing. They didn’t take it and sold in the 90s for less. A few years ago it sold for $2.5M and was torn down. The replacement condos sold for about $12M

I didn't count it... I was probably 9-10 years old. It was a pretty surreal experience, honestly. I do remember that it was real, my parents talked to him, i guess he was a reasonably well known real estate guy in our area.

In retrospect, it's even stranger. I couldn't fathom cold-knocking at a random house and offering the owners a suitcase of money. Double++ bizarre making the pitch to a little boy. That said, we had alot of interesting stories from that house and neighborhood, this one isn't even the strangest!

Sort of similar here. A coworker said I should buy real-estate - any amount, any way I possibly could. It has to go up 20% a year, he told me.

There's just something when random people who have no particular interest in investing suddenly are preaching an investment that smells like a bubble - and one close to bursting. It still took a couple of years from there, though.

Maybe it's because the pyramid has nowhere else to go from there.

And of course me pointing to previous real estate downturns was dismissed - it was still viewed as fundamentally impossible for real estate to lose value.

Wise men do at the beginning what fools do at the end? Combine that with Sturgeon's law and if more than, say, 20% of people are doing something, it's a fad at best or a bubble at worst.

Not US, but my wake-up call was my sister purchasing a small apartment for just 8000$ in 2002, in an industrial part of the city, surrounded by beat-up apartment houses and humungous acetone storage units. Whole place reeked of chemicals and the low price was justifiable, as "nobody wants to live there". She sold that very same flat for 80 000$ in 2006. Bought by a young couple, who's combined income was enough for 110% financing with no down payment and some extra cash left to spend. Suddenly a lot of people wanted to live there, because it was the only thing they could afford, or it was one of the last areas in the city with somewhat lower prices, thus giving way better profits when speculating. Then came 2008 and the rest is history. Taught me another lesson - never rely on savings too much, they dwindle way too fast

Happening here in Sri Lanka. Still waiting for the market crash to happen. People are spending upwards of 70% on all their leasing across housing, expensive cars, and luxury items like 65 inch TVs not to mention CC bills. Banks have started buying up debts and offering refinancing plans. Meanwhile I'm hunkering down and saving cash wondering if I'll get lucky

You could be waiting a while. If a government with good control over a sovereign currency doesn't want a housing crash to happen, it can forestall it for a long, long time by keeping interest rates low. People were predicting a housing crash in the US starting in 2003, and people have been predicting one in Australia for a decade.

>People were predicting a housing crash in the US starting in 2003, and people have been predicting one in Australia for a decade.

That's because of negative-gearing. Basically, mortgage payments are tax-deductible. So if you have a house and rent it out, then you can take the tax, use it to pay off the mortgage on the house you're renting, and not pay any tax on it at all.

This, naturally, makes investment housing a much better deal than it should be, and discourages selling a house (thereby driving up housing prices, and therefore rent prices, thereby making investment housing more lucrative).

It's broken bullshit. Blame the (main right-wing party) Liberal party.

Sometimes I wonder whether the parties in Australia are named just to screw with Americans - the Liberal party is conservative, and the Labor Party is officially spelled with the American spelling, despite "labour" normally having a U in it, here.

Defaults can cause interest rates to rise, which happen when expectations aren't met. Such as labor costs rising more than expected, causing businesses to default on their loans or shortage of a natural resource causing it's price to spike. It can then cause a chain reaction of defaults and interest rates rise to reflect the increased risk premium. Unfortunately, due to lags in the feedback loop, this is inevitable as you can never accurately predict the future.

If inflation gets too high, the government needs to find a way to take money out of the system, and raising interest rates can help to do that. Raising taxes can, too.

Sounds like the kind of situation which will crash once interest rates rise. I hope your cash is in USD or another solid currency. At this point I do not think it is a question of getting lucky, if anything you want it to keep going. Longer it goes on the more cash you have and the higher the discount rates.

My worry would be that once prices crash two challenges will appear:

1. Once the crash starts there will be tons of attempts to stall the inevitable. It could be months before prices hit a true low point.

2. Credit is going to dry up. Domestic banks will not have the balance sheets to allow for further lending. What loans will be available will be hard to get and more expensive than is "fair".

Which speaks to how difficult it is for consumers to benefit from conservative behavior in times of folly. Unless you save enough to buy discounted assets in cash out-right consumers buying at the bottom of the market are also buying in the context of restricted credit.

For my own situation, me and my wife are buying a house here in Japan. Over here bank's balance sheets are super-healthy and banks are extending large volumes of credit easier than they would in the past. My friends and co-workers got accepted for large home loans at reasonable rates. I have studied the bank balanace sheets as part of my stock investing so I am not worried of us being in a over-credited state. In fact japanese banks home loan load has been decreasing on a percentage basis over time as old bubble era loans get paid off.

Yet it appears to me that Japan is in a phase of expanding home credit. Or atleast expanding home credit to lower/younger quality borrowers in response to fewer traditional borrowers starting families and buying homes.

The net result in Japan is that buying a home is a massive good deal. We were careful with the location and builder but I needed to put no effort to get a loan at an insanely low interest rate.

Problem with Japan's housing, last I checked, is that there is no resale market. This is due to their culture were they want it new so they usually don't buy used houses. Not sure if that has changed but it would be something I would want clarity on.

Here in South Africa I am also hunkering down and saving money. People are getting behind on repaying unsecured debt at an alarming rate. I'm just concerned that the value of cash will become useless if the economy crashes. I also keep some in Etherium, physical silver and a little bit of USD.

I've stayed closer to %20 and it's allowed me to support a family of four for 20 years on one income while riding through two employment layoffs during that time.

Also, rather than spending our proceeds from the sale of our home in 2005 I put it back into our new home once the market was near the bottom. The net of all of it was that I was basically able to cut about 18 years off our original 30 year fixed rate mortgage.

It’s a standard used by mortgage underwriters, presumably based on analysis of decades of past mortgages they’ve written and calibrated to balance their risks and rewards for maximum profit.

"I mean that when a tax or rent is paid in EVE, this does not cycle back into the economy, it just magically disappears. In the real world, when a property tax is paid it cycles back into the economy through expenditures on public infrastructure such as education and road maintenance"

"

Interesting - there's not a way to develop something in the game that could cycle it back in?

Simply cycling it back in is certainly doable, and arguably already done (or approximated) - I'd argue it's more the local infrastructure deterioration/modeling that isn't (fully) simulated in EvE, for NPC infastructure. A couple of gamedev terms:

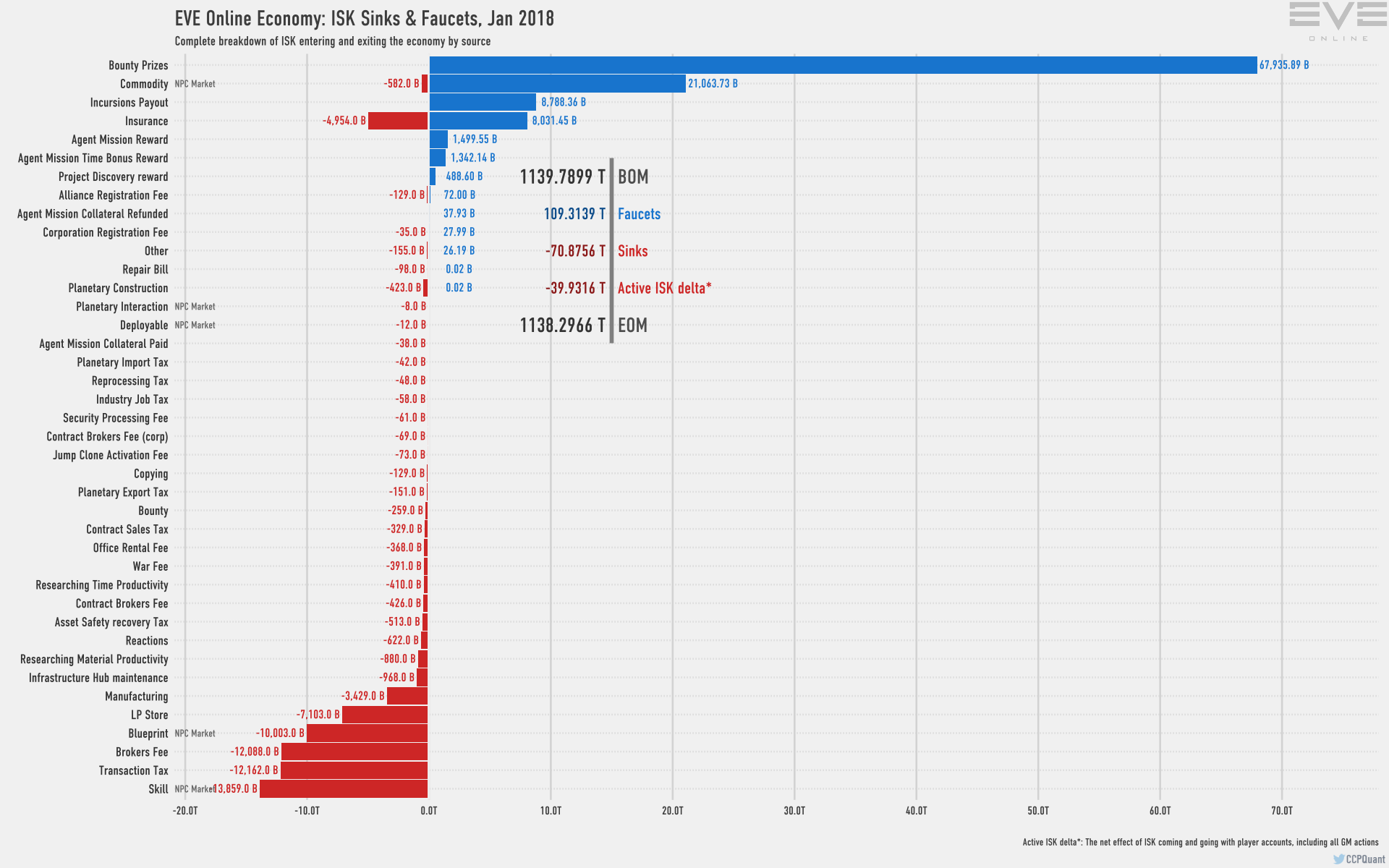

- Cash faucets - sources of currency generation / magically introduced into the economy, functionally equivalent to the bank printing currency in the real world.

- Cash sinks - places where currency is magically destroyed / taken out of the economy, functionally equivalent to the bank destroying old currency in the real world.

If your cash faucets and sinks exactly balance each other out, you could look at it as the bank simply reinvesting the currency instead of creating and destroying an exactly equal amount - externally, the net effect is identical. Of course, this is rarely the case - both in games and in real life. For the currency to be "healthy" and serve a purpose in a player economy, you want to avoid faucets outnumbering sinks to the point that you have extremely inflation. E.g. in Diablo 2, one would barter in known rare items - gold is effectively worthless, there are few effective sinks to sink it into.

(Games of course usually use an impossible number of magical faucets and sinks - the kind of centrally planned economy that would require a star trek style post-scarcity environment run by complete and utter LARPing fanatics to ever pull off, contrasted to our current real world where you maybe have a single state bank trying to carefully control inflation with a currency printing lever.)

Returning to EvE online: They still have a bunch of magical zero-maintenance infrastructure in "high security" space, but they've also added a lot of player buildable infrastructure that generally needs fueling and defense. If you don't pay for a road's upkeep in real life, it starts to get a few potholes. If you don't pay to maintain and defend your player owned stations in EvE online (be it through your money or your material and your time), someone's going to blow it up or take it from you - for amusement, profit, or both. This is a much stronger deterioration of infrastructure than you generally see in real life. (I forget how much of this player buildable infrastructure predates this article, if any.)

Of course it's possible. But in a game you don't want to create the most detailed real world simulator but an abstraction of the real world that feels real enough while at the same time is a lot easier to implement than the real thing. In MMO economies that usually means you have magic money creation boxes (mostly killing monsters or mining resources for unlimited sources) and money destruction boxes (e.g. repairing your items or paying tax/rent for different things). If you have more creation than destruction you have inflation, which is fine to a limited extend.

There are plenty of 'taxes' in game that are cycled back in. What is being referred to here are fees that deter certain gameplay styles such as not ever joining a real corp. That said, there are some currency sink fees that are used to help maintain reasonable economy stability as well. That's needed in any game with an important economy aspect.

I thougt it funny to spend a huge realestate tax increase on building aditional houses. Then do the same with food and utilities. Like government tossing the hot potato into the air and catching it again.

Bookmarked this thread. Does anyone have information on what the current state of the global economy is and if we are facing another recession imminently?

> "The basic algorithm divides points by a power of the time since a story was submitted. Comments in comment threads are ranked the same way."

> "Other factors affecting rank include user flags, anti-abuse software, software which downweights overheated discussions, and moderator intervention."

The prior discussion was from 42 days ago. From what I've observed and seen mentioned, normally if the previous discussion is from a year ago or more, then it won't be marked a dupe.

If you think something was done unfairly, the best way to get an authoritative response is to email the mods via the Contact link in the footer.

{kind=link}

{kind=link}

I had desired such a tool relative to speculation on the stock markets (and at the time postulated that requiring whoever 'owned' a future __must__ receive it when it comes due); however the idea of taxing that invested value while it is held seems to be an even cleaner way of handling the problem.