Congress has not been friendly to startups this past decade.

A few results of their well-intended efforts:

1. Startups today have little or no realistic hope of gaining liquidity through an IPO, leaving them in a position where M&A is their only realistic exit, with the result being that valuations are lowered for founder exits (the consequence of Sarbanes-Oxley, among other new laws).

2. Startups today can't simply price their stock based on the reasonable business judgment of a board of directors, nor can they use a simple 10 to 1 ratio in pricing their preferred versus their common stock, but must instead incur significant expense in having to do independent outside appraisals just to take simple steps such as issuing stock options (the new 409A statute and accompanying regulations have brought this about).

3. The VC market has been all but dead for the past two years, owing in no small part to congressional actions that helped fuel the Fannie/Freddie subprime mess, leading to a financial meltdown.

4. Add to this the hammer that is about to fall on angel funding as reflected in the Dodd bill, and startups will not only have their VC funding sources largely dried up but will have far more restricted access to early-stage funding across the board. In practical terms, this will mean that funding activities will need to be based on: (a) having access to comparatively wealthy angel investors (maybe 25% of the current pool) while being prepared to incur significant delays in getting funds pending a minimum 4-month wait; or (b) relying on Section 4(2), which is the section of the 1933 Securities Act that offers an exemption from registration for private placements but without benefit of the safe-harbor approach of Regulation D and its rules relating to accredited investors (the equivalent of "walking on the high wire without a net").

Maybe any given point above is over-simplified or overstated but the broad pattern is clear. No individual item is ruinous but each contributes to costs and restricts options. It is not a good trend for startups.

Freddie and Fannie did absolutely nothing to fuel the subprime mess. They were not allowed to invest in any subprime mortgages during the bubble and were later forced by law to invest in them when the crash was already happening, because that was Bush's plan to stop the crisis. This is just an excuse that people that caused the sub-prime mess use.

- In 2000 Fannie buys $600 million, and Freddie buys $18.6 billion, and guarantees 7.7 billion more.

- 2002-2006 the GSE's buy 38-90 billion a year in subprime mortagages

As far back as 1999 you can find stories stating that Fannie was being pressured into subprime:

Their activity appears smaller than the market at large, but it's not non-existant. It doesn't seem on face value that they were not allowed to invest. Is there some rule I am missing?

It seems I was wrong about that. But still their activity was just a small part of the market at large and they only bought the safest tranches. Saying they were responsible for the mess is just wrong, imo.

One, they did buy subprime mortgages; two, they've lost hundreds of billions of taxpayer dollars so far (and will lose more) paying for their distortions of their mortgage market. Hundreds of billions of dollars burned, lost, destroyed fueling housing demand, and you think that had nothing to do with the subprime crisis?

If you didn't have GSEs in the market, interest rates on mortgages would have been higher. That is the role they played, but it was quite small on a relative scale.

<rant>I am amazed at the things people find important enough to take action on -- or not.

Seems to me, just guessing, can't be sure, but a bill that has these things in it should be the #1 item on HN, and we should be organizing as a community to stop it. I don't care what your politics are, this is a political thing that needs to be stopped.

Parallel Haskell is awesome and all, and goodness knows I want to hear more about Apple and Flash, or linux, or iPads, or Adobe, or browsers, or Jon Stewart's jokes last night, but this is real, live stuff that could impact anybody with a startup.

If the Philadelphia news ran a story "Philly on fire!" people would come out to try to put the fire out. HN runs a story "VC investing seriously challenged!" and you can hear the crickets chirp.</rant>

The bill does not have these things in it. It is merely a huge overreaction. Most people that complain about this section, are really worried about other parts of the bill but do not want to admit that they are worried about those other parts of the Dodd bill. So this is merely a red herring and people that know what they are doing recognise it as such.

It says that the Securities & exchance commission should raise the threshold, using its existing authority, as the Commission determines is appropriate and in the public interest, in light of price inflation since those figures were determined;

..and in the next section, directs the Comptroller of the Currency (the banking-specific regulator) to examine those investment thresholds and evaluate the feasibility of forming a self regulatory organization for hedge, private equity, and VC funds.

Now, I recognize there's a wide spectrum of opinions on the degree to which government should regulate the financial industry. And I totally agree that angel investment is critical to small businesses like tech startups. And I agree that a million $ in assets or an annual income of $200k is already a fairly high barrier to entry, while technological change since 1982 has significantly lowered startup costs. And so, I agree that just mindlessly jacking up these thresholds would likely be a Bad Thing - for startups, angels, and the economy.

What I'm grumpy about is the meme that the bill does mindlessly jack up the rates. The SEC's existing rules require public consultation on such changes - so if the bill passes, the thresholds will not suddenly shoot up. Rather, the SEC will announce they're considering it and invite input from the public - including people like us - for 3 months. And the SEC has been responsive to that input in the past. Mainly they're worried about not allowing another Bernie Madoff episode; it's entirely possible that they might employ their rulemaking power to carve out an exception for Angels and VCs.

And in the next section, where venture capital is explicitly mentioned, the bill directs the other regulator to study whether and how such funds - which are, obviously, quite different from banks - could be allowed to regulate themselves. the main purpose of this bill is to regulate big wall Street banks. There's a clear understanding here that small funds are not banks; they operate differently, are much more competitive, and probably shouldn't be regulated like banks. The bill supports the idea that such firms will do a better job of keeping each other honest than direct regulation by government!

Participants in a diverse a competitive market (for fund management) are best placed to decide what constitutes 'fair play'. Where self regulation fails is the situation where a few players utterly dominate the market - for example, the fact that 6 large banking firms currently manage about 60% of all capital on Wall Street - and tailor the rules to suit themselves, to the detriment of the smaller players, and of the customers. For that reason, the bill also seeks to put an end to the practice of large banks creating and capitalizing hedge funds that are nominally independent, but in reality are just legal vehicles for large institutions to take advantage of the lighter regulatory and disclosure requirements for hedge funds, while leveraging the reputation and deep pockets of the creating bank to attract customers away from smaller funds.

Why is this important? Because the SEC failed to heed warnings about fund managers like Bernie Madoff and Alan Stafford. Their competitors knew the performance of those funds was 'too good to be true' and repeatedly asked regulatory agencies to step in, but were mostly ignored. The bureaucrats' reporting requirements were being met, and they did not understand the sheer improbability of such consistent profitability in a volatile market. Competitors did: customers preferred fairy tales to honest reporting of market behavior. Hierarchical regulation failed dismally where peer review would have put a quick stop to the abuse.

Result? Jittery investors lost faith in all private capital management and VC funding fell by almost 50% in sectors like biotech and internet from 2008-2009. Some $5 billion was taken off the table - perhaps more. Less VC funding means less angel funding: no mezzanine capital means no exit or equity partnership. You can't grow an oak tree in a one gallon pot.

Self-regulation of the private capital market could reinvigorate capital formation significantly. Reduced red tape and peer review are strong economic incentives for honest and transparent risk management. Investors want transparency, and they want innovation rather than speculation, in which it is all too easy to end up on the wrong side of a zero-sum trade. There is enormous potential here to deepen and diversify the investment pool, and that would be very good news for startups.

So as it affects Angel and VC funds, the bill does two things: directs the SEC to re-examine investment thresholds in the wake of a real financial meltdown; and directs the CotC to consider reducing government regulation of private capital management, rewarding true competition with greater trust.

Instead of seeing this bill as a giant monolithic gravestone for capital formation, entrepreneurs, angels and VCs should look at the potential long-term benefits and use the public consultation process to tell regulators what kind of market they need, and how an open self-policed market could unleash a wave of innovation in the real economy. The giant Wall Street banks do not like this bill, but you can worry about them when you're ready for your IPO. Until then, they won't take your calls anyway. Consider your own interests rather than theirs.

Can we have a little more risk and a little less nanny state please? I don't mean that in some kind of Republican or Libertarian or Randian sense, I just would like more opportunities to raise money. So I can create ideas and raise capital for a startup.

Instead of us being so happy about everything is working, and putting in our order early for just the kind of market we want regulators to create for us, is there really something that wrong with just being left alone? I'm not talking Madoff, I'm talking Bob's Pizza Parlor.

You've got 250K, I've got some hair-brained scheme, you pays your money and you takes your chances. Most of the time you lose. Sometimes I'm a crook. This is risk. Change is based on risk.

Somehow is this same size expenditure good for a drunken weekend in Vegas yet somehow terribly harms society when applied to startups?

Yes, the bill does not mindlessly jack up the rates. And yes, there are wonderful reasons for something getting done. If that makes you less grumpy, isn't it a reasonable thing to ask, while Dodd is writing this bill, to make things easier? I'm not trying to move the goal posts, but if you're under the hood anyway, could you try cutting us a little more slack? Why do we always have to gravitate to more "market management"?

I guess I'm grumpy as well. This is the 4th or 5th time I've read about this bill, and I'm just amazed that we're quibbling over reasons and precise language and missing the fact that, for us, we're heading in the wrong direction.

Can we have a little more risk and a little less nanny state please?

C'mon man, 3/4 of what I wrote was about legislatively reducing state oversight of capital management, and how strongly I favor the idea, for the same reasons that you do.

And in the other 1/4, I talked about using the mandatory public consultation period to shape the SECs decision, as has happened before and which (IMHO) is much easier to argue on its merits to a regulatory agency than in the febrile atmosphere of a legislative session.

Error in above - I keep saying 'Comptroller of the Currency' when referring to section 413, which actually says Comptroller General, part of the GAO. Sorry if this has resulted in confusion.

Also, this link for the bill is slightly more up to date than that of the banking committee, although the passages discussed above haven't changed substantively - the only difference is that section 413's 3 subparagraphs have been reconfigured as sections 413, 414, and 415: http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=11...

> It says that the Securities & exchance commission should raise the threshold, using its existing authority, as the Commission determines is appropriate and in the public interest, in light of price inflation since those figures were determined;

Actually, it says "shall". Should is a request. Shall is a mandate.

There's some wiggle room in "determines is appropriate and in the public interest" but the marching orders are pretty clear. Do you really think that they're going to come in significantly lower than where the inflation numbers come out?

I'm serious - the inflation numbers give us $2.3M. What's your "I was wrong" number? Is it anything over $2M? How about $1.5M?

Note that Section 412 has two parts. The second "(2) adjust that threshold not less frequently than once every 5 years, to reflect the percentage in crease in the cost of living." doesn't have any discretion.

There are no requirements that the increase follow inflation numbers. It only says that the SEC should increase the rates as "the Commission determines is appropriate and in the public interest, in light of price inflation." I guarantee you the SEC will not double the standards over night. They will have a long rule making session will ask for comments from the public as they are required, and will slowly increase the standards while studying the effects.

So yes every article that says "The Dodd bill also raises the net worth and income thresholds to $2.3 million and $450,000, respectively" like this WSJ article is dead wrong. The Dodd bill does no such thing.

> There are no requirements that the increase follow inflation numbers.

There's some discretion in the intial bump but, as I quoted, there's no discretion for subsequent and regular increases.

> It only says that the SEC should increase the rates as "the Commission determines is appropriate and in the public interest, in light of price inflation."

That's only for the initial bump.

> I guarantee you the SEC will not double the standards over night.

"Guarantee" implies that money will be changing hands if you're wrong....

Yes, they'll probably have hearings, but they've been told how they "shall" compute the new number. That's why I asked what you're "I was wrong" number is. I'm asking again.

But consider that the SEC has been responsive to input on this very subject after previous consultation - and I really don't think a policy review is inappropriate, in the wake of a financial meltdown. And while 412 does indeed have 2 parts, it's clearly a placeholder directive, pending a year long review of both accreditation and regulation of private capital by the Comptroller's office mandated in 413.

Now here's how I look at it: Goldman and other large institutions are politically radioactive right now. We could debate whether or not that's fair, but there it is. Public support for Wall Street is at a low ebb, and Congressional Republicans have decided to debate financial reform rather than fight the tide. The big issues are bank liquidation, derivatives markets, and who will regulate consumer finance - neither the GOP nor the White House are too hot on creating a new agency that might get into fights with existing ones. this investor accreditation issue is way down the list. You should certainly call your senator to express opposition if that's how you feel, but: a) for the many tech startups & VCs in California, that's Dianne Feinstein who is unlikely to empathize; and b) it's easier for Congress to delegate the nitty-gritty details to the agencies. Frankly, I'm surprised the bill isn't more prescriptive on this issue.

So suppose it passes. Two new factors come into play. One is that the SEC will hold their public consultation as discussed, and we can predict a negative reaction from startups, angels and VCs. Given the parallel review and the weak recovery so far, it's possible - I think likely - that the SEC will prefer not to introduce job-killing rule changes that would block access to capital in the short term, but wait on the other agency.

----

EDIT: I mixed myself up royally earlier, talking about the 'Comptroller of the Currency' when what I should have written was 'Comptroller General' - part of the GAO. I then looked back to my own text for further reference, perpetuating the mistake through two more paragraphs to no meaningful purpose. Sorry.

I do still think that the year-long review of accreditation and fund regulation is important to HN readers.

New factor two is that in August, John C Dugan will finish his term as head of the OCC (main commercial bank regulator

[... EPIC ACCURACY FAIL....]

small business is something that's easy to sell for both Democrats and Republicans.

----

So again, I respect your skepticism about the bill as a whole; but passage of it could increase opportunity rather than just cost.

Have I missed a runaway profusion of investment scams targeting people with net worths between 1 million and 2.3 million? The perceived need for this just perplexes me.

There actually are such scams all over the place. Couple of years ago I was in a position where I was an accredited investor (based on income) and I had to basically reveal that information on the Internet. I was an attorney in one of the large international law firms and they required you to post a professional biography online. The biography did not mention your salary, but the top lawfirms pay lockstep and publish their salary info so anybody familiar with the legal profession could have figured out the salary from the posted information.

Anyways, as soon as I fit the criteria for an accredited investor I started getting calls for what seemed to be obvious scams. There were generally of two types. One type was a call from a boiler-room type operation from some guy with a hilariously exaggerated Jersey accent asking me to buy some over the counter stock. They would suggest a stock for me and then call a couple of months later and say "see the stock we suggested before doubled in price, you should have invested with us, why not try this new stock we are suggesting now." Of course OTC stocks are so thinly traded one can easily manipulate the price.

The other type of scams are calls that are made to sound like they were accidentally made by people that have their cell-phones in their pockets and accidentally press a button. It is usually conversation between two people that is supposed to be private and you are only hearing it by accident. The two people then disclose "important inside information" that is supposed to make you rush out and buy a certain stock.

So yes those scams are out there. There are boiler-room operations all over the place trying to bilk people that are on the lower end of the accredited investor spectrum.

Usually, they prefer accredited investors because stocks that require such investors do not require SEC filings so the scams are easier.

call 1000 people today, tell 500 of them football team A is going to win this week. call the other 500 people, tell them that football team A is going to lose this week.

Football Team A wins.

Next week call 250 of the people that you told team A would win this week, tell them football team A will win again. Call the other 250 and tell them that football team A will lose.

by the end of the season you'll have a dozen or so (i think?) people that will believe anything that you tell them

[if anyone can tell me the source of this idea (book/movie?) let me know!]

The article is behind a paywall, but I'd be curious how big this population is. How much actual funding derives from investors in that range? My guess is not much, and of that I suspect a lot of it is of the "rich uncle" form, where you can just make the trusted relative or friend a "founder" and get around the rule.

You do not need to make the relative a founder. When it comes to relatives you probably do not need to worry about the accredited investor stuff at all, as there is an exception for purely private placements. (this is not legal advice, do consult a lawyer).

Anyways, I agree that the lower end of the accredited investor range probably does not contribute much or anything to angel investing.

I seem to recall reading some advice that friends-and-family money is limited to a couple dozen people, and their involvement can make early VC rounds more complicated therefore harder to get. Is there anything to that?

The exception for private placements is not limited as to people or amounts invested. But a lot of lawyers do not like using that exception because it is not entirely certain what constitutes a private placement. So if they are not very close "friends and family" you may get in trouble. Therefore, a lot of lawyers prefer to use other better defined exceptions.

Regarding VCs, they dislike any earlier investors, and they probably dislike laypeople more because they prefer to deal with professionals.

In any event, again please make sure you consult a securities lawyer for your particular situation. I am really an IP attorney, so while I know the securities laws I do not have much experience in that field.

"they probably dislike laypeople more because they prefer to deal with professionals"

If they've got a clue they most certainly do. There's few things worse than dealing with a squirrelly non-professional investor (been there, done that, both myself and my father).

Still, if you have to get money somewhere to attract bigger investments and if this bill passes without fixing these problems you may find yourself pretty much limited to "very close "friends and family"".

I.e. if you live in a state where all others are forbidden to invest ... and from that TechCrunch item posted to HN the association of those state regulators may be the entity that's pushing this hard. Which means we may get much less of a fix that we desire/need.

This article leaves out that along with moving the net worth from 1 to 2.3 million for accredited investors, they are also not allowing primary residence to be counted anymore, which for many people is a large part of net worth.

The SEC filing for startups is insane. The last thing we need is further roadblocks and delays for early stage startups.

PG, would this affect y-combinator? YC is the first investment for companies in your portfolio. Would they have a 120 day delay? Four months is a long time in startup land. This would certainly give a head start to bootstrapped companies.

As indicated in my first comment, the article is focusing on the regulatory problems first; as you note, filing with the SEC with a 120 day delay is awful. Letting the regulators of all the states into the game might be worse, in that I'm sure angel investments would be de facto or de jure outlawed in many states (the state residence of the firm and/or of the angel).

Wow, the economy is stumbling and the only way out is innovation and now they are trying to make it harder to start a company. Just how do they propose we get the economy back on track? Sorry printing more money is not a long term solution to economic recovery. It amazes me that our elected officials have zero grasp of how the economy works. These are supposedly educated people and yet they consistently treat the economy like some grade school battle for teacher's pet honors. Sorry for the rant but crap like this makes me question the viability of our current governing system.

As @rmaccloy I'm not against the idea of bank reform but these types of provisions and attachments to bills are causing so much waste and then we wonder why we have such a huge deficit.

I think it's more our current ruling class than the system per se, although that depends on how you define "system".

No system can work if you have fools running it. Our big C Constitutional system has worked better in times past when better people were in office ... and worked worse when worse people were in, e.g. Hoover and FDR making their economic mess worse and prolonging and worsening the agony.

It's just not that bad yet. While e.g. Cash for Clunkers was pure "broken window" bogus economics, do we have anything quite as vile as the Agricultural Department destroying food and preventing its production while at the same time they calculate 1/4 of the nation is malnourished (which the DoD confirmed in the WWII draft)?

Well, maybe this is as perverse, although not hardly as vile. As grellas details in some length, in a period of bad economic times (starting with the dot.com crash) our ruling class as seen fit to steadily destroy the foundations for startups. And it's a general bipartisan thing, e.g. a ruling class problem.

There are, realistically (ignoring the rosy projections of going below a trillion in FY 12, a Presidential election year), trillion dollar annual Federal deficits stretching out as far as the eye can see. Where is this money going to come from? Not from new enterprises and new industries, there will be few if any new Apples, Suns or Googles ... hmmm, Microsoft managed to bootstrap itself, but such opportunities don't come along often and the computers and their components that ran Microsoft Basic and so on were largely/almost entirely not self-funded.

I'm surprised this hasn't been brought up more on HN. I'm not against bank reform, but these provisions seem clearly detrimental to prospective founders without providing any actual protections to people who need them. Correct me if I'm wrong...

If someone's going to make this case, could they please do so from somewhere without a paywall and if at all possible, from a source who's logic is more honest than "are republicans or democrats in office right now"?

IF the claims are correct though, then that needs to be fixed in the bill, particularly the part about filing with the SEC.

I'm also waiting for a second source. The only other story I've seen on this bill was also from WSJ, and also written with a heavy spin on it.

This paper's editorial page will argue against anything the current majority party does. Their news reporting is fine, but it's widely known that the editorial page leans strongly to the right.

This same editorial page argued that the healthcare bill contained death panels. Republican politicians, including Palin and Dick Cheney, are regular writers.

And I think you underestimate the significance of the editorial board of The Wall Street Journal taking a strong position on this issue in a house editorial.

The Wall Street Journal's opinions are driven entirely by which political party controls Congress.

After 8 years of the "deficits don't matter" administration, all of a sudden these guys turn into budget hawks 1 month after Obama inherits their fiscal situation. They're against quote "socialized" healthcare even though the bill didn't socialize anything that wasn't already a government program.. but the more expensive Medicare Part D program was just ducky with them. Etc, etc etc.

I have no problem believing there are problems with the bill that would accidentally affect startups. But if we're talking pithy 2-sentence characterizations from a source with a history of partisanship? Citation needed.

Hang on, I mention the fact that WSJ is hopelessly biased, and you respond with a link to an even more biased source?

Ok, let's back up and try to engage your brain for a second. So you have a set of 10 year projections there. Those are predictions about the future. With me so far?

Now think about what they were on January 15, 2009 as opposed to January 25, 2009.

Do you think that the act of Obama taking office changed the future and mandated a ton of future government spending? Or do you think these might be fundamentals that we were going to have to deal with regardless?

For bonus points: How much of those future deficits would you guess have to do with the increasing cost of healthcare?

And I'll leave out entirely what they might look like if we hadn't just endured 8 years of studied fingers-in-the-ears idiocy from the Bush administration. Remember that surplus in 2000?

Heritage and WSJ are concerned about deficits. Who did they support in 2000 again?

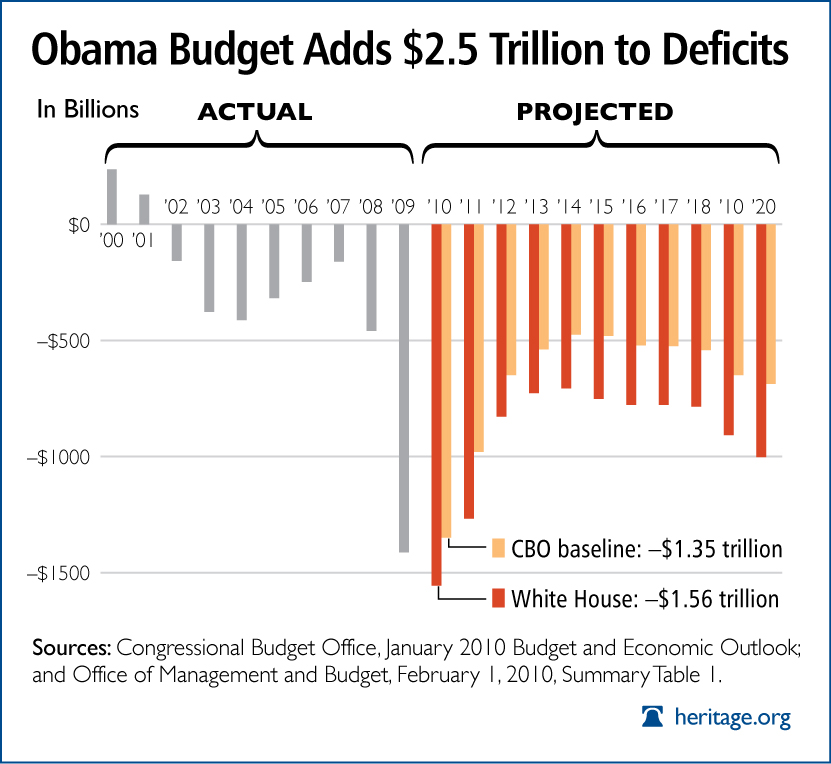

You asked for a second source, you have it: the CBO and the White House. The fact that heritage put CBO numbers onto a graph does not make them invalid.

I asked for a second source regarding the financial reform bill. I'm well aware of the approximate projected size of our federal deficit, thanks.

The fact that Heritage supported Reagan, opposed Clinton, supported Bush and now claim to be concerned about deficits says a lot about the Heritage Foundation.

EDIT: Awesome, downvoted for clarifying a willful misinterpretation of my original comment. Ladies and gentlemen, your conservative movement -- it's not about facts, it's about which side you're on.

You were given several other sources for that as well, all of which were posted here. You also criticized another source simply for being conservative, which is what I was responding to.

Regardless, please clarify your point. Do you believe the WSJ is lying about the contents of the bill? If not, then what is the relevance of pointing out their opinion on other political matters?

I believe they're extremely prone to exaggerate any bad parts, and there was room for a lot of weaseling in their descriptions. Especially considering that the bill isn't finished yet.

I'm still waiting to see the death panels. Since they'd never lie, of course.

I didn't criticize Heritage for being conservative. I criticized Heritage for being Republican, regardless of principle or policy.

EDIT: To clarify, it's entirely possible that the provisions in the bill still being written are just as bad as the WSJ says. It's also possible that they're significantly less bad. Regardless of which they are, the WSJ would have written this exact article. Does that make my complaint regarding their worth more clear?

Agreed that a second source is sorely needed. FYI: you can always access WSJ (and most other news articles) by doing a google search of "<article title> site:wsj.com". News sites aren't allowed to show article text to the Google crawler without allowing the user to access the article.

Oh, for fuck's sake. We're not hurting for a lack of angels because of the accredited investor rules. We're hurting for a lack of angels because there aren't a lot of people who are willing to cut checks to young companies without revenue after other people they know said no. Jacking up the minimum threshold to $2.3 million from $1 million (assuming this passes in current form, which it won't) is a complete non-event for almost every founder.

If we assume, for the moment, that your thesis is correct (and ignore the friends and family type of angels), the other regulations are arguably worse than the new threshold requirements. Which the WSJ implied by the editorial board's placement of this issue at the end of the editorial.

How many startups will still be alive after they've waited as many as 120 days for the SEC to bless their fund raising effort? How many will be able to run the gauntlet of state regulators? If the Massachusetts regulator is as conservative as it was in the '80s, there will be no angel financing in that state, full stop. How bad will nanny state California be???

I think the minimum NW change is the most minor of the issues here (especially in SV). Imposing more of a regulatory burden isn't going to make anyone more likely to cut checks, and increasing the barrier and latency to initial funding is going to make plenty of potential entrepreneurs decline to make the leap.

I think it's quite dangerous to assume such provisions aren't going to make it past whatever partisan wrangling goes on; I doubt either the dems or the GOP are going to give much of a damn about the startup ecosystem unless a lot of noise gets made about it.

"[...] increasing the ... latency to initial funding is going to make plenty of potential entrepreneurs decline to make the leap."

That's a very good insight. Up to 120 days is a long time to develop second thoughts, have something else come up that changes things for the investor, etc.

I suppose you could include a CD or DVD of porn as a bribe to overall speed up the SEC's processing of your request ^_^.

{kind=link}

A few results of their well-intended efforts:

1. Startups today have little or no realistic hope of gaining liquidity through an IPO, leaving them in a position where M&A is their only realistic exit, with the result being that valuations are lowered for founder exits (the consequence of Sarbanes-Oxley, among other new laws).

2. Startups today can't simply price their stock based on the reasonable business judgment of a board of directors, nor can they use a simple 10 to 1 ratio in pricing their preferred versus their common stock, but must instead incur significant expense in having to do independent outside appraisals just to take simple steps such as issuing stock options (the new 409A statute and accompanying regulations have brought this about).

3. The VC market has been all but dead for the past two years, owing in no small part to congressional actions that helped fuel the Fannie/Freddie subprime mess, leading to a financial meltdown.

4. Add to this the hammer that is about to fall on angel funding as reflected in the Dodd bill, and startups will not only have their VC funding sources largely dried up but will have far more restricted access to early-stage funding across the board. In practical terms, this will mean that funding activities will need to be based on: (a) having access to comparatively wealthy angel investors (maybe 25% of the current pool) while being prepared to incur significant delays in getting funds pending a minimum 4-month wait; or (b) relying on Section 4(2), which is the section of the 1933 Securities Act that offers an exemption from registration for private placements but without benefit of the safe-harbor approach of Regulation D and its rules relating to accredited investors (the equivalent of "walking on the high wire without a net").

Maybe any given point above is over-simplified or overstated but the broad pattern is clear. No individual item is ruinous but each contributes to costs and restricts options. It is not a good trend for startups.