Agree, last time the world had any significant CPU performance increase was SandyBridge, and that was the tipping point. Since then we have been using the same CPU performance with less energy usage. Apple already knows this that is why they continue to refine in other areas ( Macbook being a prime example ) rather then providing more and more performance where the user don't need / feel.

Interestingly 2011 was also the year SSD were available in not so luxury price. It was the when 64GB dropped to around $100. Anandtech has been calling this as the largest performance upgrade in history. And I would agree you should trade SSD for ANY CPU performance. That is assuming you are not using some more then a decade old CPU or you already have 16+ GB memory.

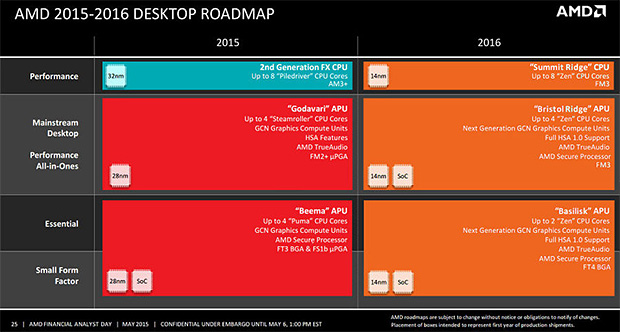

If the rumours are true then it is a combination of things making this a perfect storm ( not sure if that is the right way of putting it). Intel no longer has a significant lead in Fab node processing. The money from Mobile processor has help pure play foundry to catch up big time. Zen would offer significant performance increase that pass what most consider as enough ( for now ), and Intel hasn't had much performance gain with Skylake. Running along is the perfect match of new GPU coming from AMD. Which should be first the time ever AMD has a APU competitive with Intel in performance and run circles around Intel in GPU performance.

This sounds all good good for AMD, that is until Intel provides more detail on Goldmont, their next gen Atom.

Goldmont, and its Apollo Lake platform, provides all the essential features one would expect for the most common PC user for a very cheap price. Cherry Tail, based on Airmont was already doing well in Surface 3, if Goldmont as rumours suggest provides much higher IPC ( think Core2 Duo like performance rather then SandyBridge ) and comes with Skylake Gen9 GPU along with much cheaper price, this could be a tough battle.

Can wait for both to reveal more details, 2016 will be an interesting year for PC.

The state of Skylake software support over the last year for both Linux and Windows (with many Linux issues still unresolved) kills any excitement I might have had for future intel products. To be honest, I'd rather have a slower passively cooled ARM chip, at least then my ultrabook wouldn't sound like a jet engine when some background task kicks in (not to mention battery drain consequences).

I agree, Zen + already great GPU designs from AMD in an APU package could be just what AMD needs right now to regain volume PC sales. I think they might actually have a better chance of succeeding here than in the server space where absolute performance/watt is more valued than in PCs and notebooks, but I still think for AMD to really regain their glory(and profits) they need to have the top performing CPU for a while and let it trickle down to APUs instead of eating scraps at the bottom of the pile like they are now.

How long before we can have open source CPU cores made a la carte by pure play foundries?

Beyond Moore's Law I wonder if we'll just see a massive drop in the cost of computing power to the point where something near parity with a 48 core Xeon is like $10. Then it would become very cheap to put tons of them in a box and build little desktop supercomputers.

I think silicon still has a bit longer to go before we will run into the end of Moore's Law on it(not even counting other substrates for transistors or logic gates), beyond simply scaling there are a bunch of other techniques to squeeze performance and lower power usage that will be economically attractive if you can't shrink anymore, we've already seen some of them like clock gating and voltage scaling, but they can go a lot further. Once we get to the terminal node(probably 5nm with our current understanding) I think we will also see a lot of architecture innovation as well. Not x86 vs ARM or MIPS etc, but fundamentally different ways of thinking about processing units. I think FPGAs, GPUs, and other currently specialized architectures will become even more important, it is possible that everything in a "PC" could be as configurable as an FPGA is today. A lot of things open up once we hit the scaling wall and are forced to make better use of the given resources.

I also think die sizes will grow, including the possibility of "3D" wafers, but that will bring its own manufacturing and design challenges as well.

Anyway I think the end of classic Moore's Law scaling is still far enough away on the horizon that nobody can really predict what will happen, but if it does indeed happen as soon as the 2020s we will be in for a treat no matter what happens I think.

Never? Or not for the next 10-15 years. The cost of producing (in your example ) 48 Core Xeon exceed $600 for any pure play foundry. This does not include any profits for Foundry to operate and no return on investment from their initial billions of equipment. Even if moores law is working at the same pace as before, you still won't see it in 15 years, let alone how moores law has slowed, and dead in price / transistors terms. Price for 10nm are in 10 billions. And will go even more expensive when we go down further.

>> Intel plateaued, no significant user-appreciated progress in the past 5+ years

It's not true. Their 3DXpoint memory offers 10x GB/$ of dram, at a speed relatively close to dram.Leaving aside the huge impact on the storage market - Intel even did an exeriment[1] , taking a 8GB Dram computer and comparing it to a 256Mbte Dram(as cache) + 3DXpoint sitting on the main bus - and they performed equally.

If that's true(and 3DXpoint has the reliability for such usecase) - this means Intel could possible own the mobile market - and own the full stack of computing.

Was 3DXpoint released as an actual product in the past 5+ years? I think the post you replied to just talked about progress in actual, released-to-market products, not future R&D that we don't even have a release date for yet.

Intel's client computing chips plateaued, but server platforms have kept improving. The volumes might be lower, but the high margins more than make up for it.

So AMD bought ATI for 5.4B only a year later wrote down 2.65B of it, valuing ATI at 2.75B in 2007. Currently AMD is worth 3B, valuing the AMD part of the company roughly zero provided ATI had at least 1% growth in each of the past nine years. Licensing out what a bit ago would've been the crown jewels for $.3B makes a lot of sense in these circumstances.

Really. In 1971, AMD was selling 4.6M, Intel 9.4M. In 1978 AMD had $100M in total sales and Intel had 400M. https://books.google.ca/books?id=GTwEAAAAMBAJ&pg=PT51&lpg=PT... this page has both '84 and '90 with Intel outselling and outprofiting AMD several times over. So when was that mysterious year if it was not in the seventies or the eighties?

I was thinking around 1980 or 1985, back before IBM PC and clones became popular. Turns out I was wrong, Intel was about 2x to 4x larger than AMD in those days.

I went back and got some hard figures. I had to average yearly high/low stock price to compute historical market cap. All values in $millions:

AMD has been keeping real Zen info much closer to their chest than Bulldozer info ever was, fueling speculation that they might have another flop on their hands, especially since Jim Keller left right after it taped out. Their future at this point all rides on if they can survive the next 1.5-2 years with little cash while getting Zen to the marketplace and hoping it is competitive with whatever Intel is putting out in the meantime.

That being said, I think Zen is entering in a much better position to succeed than Bulldozer was - They're entering with a leading-edge 14nm process from Glofo, which has been producing for a year at this point, at good performance and yields by all accounts. Glofo's 32nm process that Bulldozer is on was less than stellar and never really achieved good power consumption. What we do know about Zen's architecture also seems much more conventional and "fat and wide" than Bulldozer, a design which Intel and AMD previous to Bulldozer were pulling off successfully for years. Bulldozer's module design might have been good in theory, but single-threaded performance suffered too much compared to the fat and wide design.

If they can match Intel performance at even slightly lower price points, which seems likely given the above, I think they will easily survive the near to medium term, and if they are somehow able to do even better than that, we might be in another 2003-2007 era for Intel where they struggle to play catch up for the next few years. Seems unlikely, but you never know.

I've got my hands on some analyst reports about AMD about an hour ago (a little too late sadly) from a very respectable tech analyst (one of those wall street people with a 8 figure salary) which I can't share unfortunately.

I have to say that you hit very close to base - makes me wonder if you've also read the report or are the said analyst :) They speculate that Zen is actually a lot further ahead than AMD are willing to admit publicly.

Insiders are allowed to trade the stock of the company they work for. They just can't make a trade which is motivated by non-public insider knowledge. For example, if the company was going to have another bad quarter the insiders can't dump their stock in advance of the public release date. Most of the time, insiders will have a schedule set up and announced well ahead of time for when they want to sell stock, to avoid being accused of selling in reaction to some negative event for the company.

Insider trading as in: Reading the SEC reports that insider parties have to submit in order for them to be able to trade the stocks.

This is pretty common, for example I've found a site that uses the same reports I read to trade with a strategy http://www.smarteranalyst.com/daily-insider , I know a guy who works there and he eats his own dogfood (invests with the strategy) and so far he's claiming good profits.

Personally I don't really buy into it yet but we'll see.

After looking at all those links, I couldn't see anything that would have predicted the deals they're expecting with console vendors. That's the main reason their revenue shot up.

This I suspect is more to do with the deal with China made today and times with the announcement as far as I can see as far as stock price climb. Would love to see a global hotspot map of share buying for this, might be Chinese investment, might be many things but certainly event driven.

Yeah, I bought some AMD stock when I thought it was undervalued at like $8. It just proceeded to fall a few bucks over the next year or two.

It is cheap enough now to buy a few dozen shares and get an easy return if it rises, without hurting too much if it falls again. And it's not like AMD is going out of business anytime soon. Certainly the value of their IP and assets would justify a floor in the stock price.

Intel Skylake on a Linux laptop is basically unusable (terrible power management driver issues kill battery life and may even lead to premature failure). See https://news.ycombinator.com/item?id=11492070

Just one of the many ways Intel seems to be dropping the ball lately.

The issue at hand affects only mobile Skylakes. Skylakes targeting desktop use are not affected.

The caveat Intel published re: Skylakes is the same caveat it has published for the previous two generation of CPU's.

What we seem to be lacking is actual evidence -- numbers -- that Linux users running on those units have seen more failures than users not running Linux.

Hell, Intel Haswell in Apple hardware (15" rMBP, mid-2015) rips through the battery, even on stock OS X.

I've been at home, on AC power, starting around 9-10% battery, where it tells me 12+ hours until full charge. This laptop is 4 months old, and that scenario was only iTerm and Chrome open... :'(

One factor may be that they expect 1.5 billion in revenue from 3 devices (Playstation 4.5, Nintendo NX, Microsoft Xbox One.5???) [1]

But the chinese deal is probably the main reason

They slightly beat expectations, but that can't be the whole story. Might be something to do with Intel's recent weakness and restructuring (moving away from the PC market), perhaps the PS4.5 rumors...

I worked for AMD in the x86 64bit multicore expansion days (2006ish) There really has been much since then except the ATI acquisition. Selling to Chinese manufacturers sound like a last ditch effort unfortunately.

I have a slightly different take on AMD these days, in that I don't think they were undervalued, at least not too much, but rather I think they saw the direction the future held and jumped at it, thinking they would be ahead of intel, mostly in their understanding of the merging of cpu and gpu. I simply think they did it a bit too fast and left their other offerings with too little resources, but now that they are using the 14nm and 16nm manufacturing process, Zen is poised to be a much heavier hitter than I think most people understand yet.

So they werent undervalued too much, but they are now, and so I think you are probably correct about more radical upwards corrections.

I am especially excited to see their server cpus with zen. My favorite machine I have ever built is actually an AMD machine, and I built it fairly recently because there are some models in which they excel. (Its a quad opteron 6380 system for a total of 64 cores at 2.5ghz, and I did it for less than 5k$ Something I theorycrafted while in bioinformatics, though I didnt get to buld it until I was no longer in that industry.)

Also, I'll say that I have been looking at building a new system for my gamedev purposes, and I have concluded that I am going to wait for Zen. If they miss the q4 2016 release though they may lose the mindshare momentum they are bulding up.

The ATI acquisition was very forward looking, the problem is the hardware and software stack required to make APUs successful was nowhere close to ready at the time. We are just now seeing small enough process nodes that can support real GPU performance on the same die as a decent CPU, though the software isn't there yet still it is much closer. If Zen can match/beat Intel and it scales well enough down to APUs I think they might finally find their market, and Zen on the server should be a killer as well if that is the case, as AMD has always done really well at shoving lots of cores in small packages.

> Its a quad opteron 6380 system for a total of 64 cores at 2.5ghz

That sounds good. Unfortunately, in my experience, the real-world performance of the low-end chips in cheap laptops has been absolutely dire for about a decade. And those low-end chips are the ones most of us experience....

I was just thinking these past few days how AMD is highly undervalued and would likely see a big boost from the launch of Zen. Since Zen is still not launched yet, I think there's opportunity for the stock to grow even up to 100% or more from where it was.

As a little side note, I think it's fantastic that AMD is replacing its E-series APUs that used Atom-like CPU cores in low-end notebooks, at a time when Intel is doing the exact opposite by replacing the Core micro-architecture in Celerons and Pentiums with Atom, so it can sell what are essentially $30-$40 chips for $107-$160.

Intel did this because it thought AMD is no real competition technically, but more importantly from a brand point of view (Intel thought people will keep buying its chips at the same price points even if it replaces them with a much weaker core with many fewer hardware features). With Zen in general (thank you Jim Keller! [1]), but also with Zen in the low-end of the market, AMD just called Intel's bluff - and I think it will win this one while Intel is stuck with Atom in Celerons and Pentiums for the next few years.

The dual-core Zen CPUs in the E-series should absolutely trash the Atom-based Celerons and Pentiums, and likely the scammy $280 Core M chip as well. APUs like the A4 and A6 were already destroying Atom-based Celerons in terms of price/performance.

Looking forward to the quad-core/8 thread Zen APUs that will compete against the dual-core/4-thread Core i3 and Core i5 as well, and may even beat them on single-thread performance, if the price is equalized. From some calculations I've seen Zen may come within 10% of Intel's IPC at the same clock speed, even for Kaby Lake. But you may be able to get say an AMD chip that has the same performance as Core i3 in single-thread, almost twice the performance in multi-thread, and still cost 10% less.

As another side note, I really hope Qualcomm ends up buying AMD, though it probably should've done it last year, and it may have done it, too, if it wasn't for their own Snapdragon 810 blunder, which almost got its board to sell the chip division (a huge mistake, which I'm glad they eventually rejected).

Now the price is going to increase by 2x or more. Hopefully AMD's shareholders won't get greedy and sell for cheap, because AMD needs an infusion of cash as well, so it can adopt the latest process nodes as quickly as they are available, and so it can develop and launch multiple lines of products at the same time. That's how it can become much more competitive.

I think Qualcomm would be a good steward of AMD (it already bought the mobile GPU division from AMD a decade ago, and has taken full advantage of it). It has the commitment and incentive to want to beat Intel and go after its profits in the PC and server markets, while operating on much lower cost structures (Innovator's Dilemma and all that). But it can't do that with ARM chips alone, in part because Windows' universal apps are still a no-show for now, and in part because ARM's entrance into the server market is going to be a very slow and long process. Qualcomm's entrance into those markets would be much accelerated through an AMD acquisition (as long as it's not bank-breaking one that starves Qualcomm out of resources to invest).

Another decent buyer would be Samsung, but I only hope they do it if they are truly committed to being a chip powerhouse and to compete against Intel toe-to-toe, no matter how much it costs them to do it, otherwise it's better to stay out of it.

Just a small tip if you think mtgx is right and want to bet on the Zen making it big to wait a few days until the stock settles from the jump its just made. There's sort of a springy-ness that follows a big jump as speculators and long term investors sort out the value of the stock with this new info, and usually that means the stock will drop a few % below the peak over the few days after it.

This is just for if you want to isolate your bet on the Zen from the jump in stock that it's just made (assuming that was not Zen related). Not a prediction that it will actually go down. (If you bought now, and it would go up the coming few days you might feel like you made a good decision, but it was actually due to effects that were outside your expectations, so basically luck which is something I feel should be as small as a factor in your investments as possible)

I sure hope AMD can compete on both price and performance with Zen but:

As you say it is not released yet, let's hope they really achieve a 2016 rollout.

Is there really any money in the lowend notebook market for CPU vendors?

I think what Intel realizes is that no one really wants a fan in a notebook. Not consumers (noise), not manufacturers (less parts, cheaper). For some the performance is worth the noise, but that is only at the high end, and will Zen be able to compete there?

Who will buy Zen? What is the market? Lowend is mobile + RPi3 etc. Mid doesn't exist anymore, and highend they will still not be able to compete?

<15W TDP is enough for just about any notebook. Any 5W "fat core" CPU is mostly a scam at this point, and they aren't really viable until at least 10nm. They throttle too much (in the ultra-slim devices in which they are put), but Intel wanted to sell them anyway (Broadwell Core M was a complete dud because of this). And Core M is also eating a big chunk out of manufacturers' profits. It's more expensive than a Core i5.

Zen will be competitive at all levels in terms of performance, price and power, not just the low-end. Now, if Intel makes the highest-end Core i7 Extreme Ultra Edition chip for say $800, and AMD only makes a highest end chip one that costs $600, then yes, I would imagine Intel would still be the "winner" in "peak performance" in the PC market. But that's an out of context comparison.

The price metric should always be included in the context. What I want to know is if I have to spend $200 on a chip and for a TDP of 15W, which one has the best CPU at that price point? AMD or Intel? What about at the $300 price point and a 30W TDP? If it's AMD, then I don't care that Intel can make a 5% faster one for $350.

I only said the Zen-based E-series, which will go into things such as $200-$300 Chromebooks, will destroy Intel. And I'm not sure what you mean by "there's no mid-range". The average price for a notebook is around $500.

Schools in the developed world are doing massive notebook-sized buildout. Power consumption is the driving force in data-center buildouts. The big data center buyers have a major incentive to make sure they have more than one supplier.

No one can predict the market, but 52% is a massive jump for single trading day. For a stock that has been declining/underwater for so long, it wouldn't be unusual for some people to cut their losses and move on.

I reason about jumps like this in terms of two components. A 'real' component and an 'emotional' component. When a stock moves it moves R% + E%, for real and emotional. The real component in this case seems to be the 200MM+ deal they struck that. R and E are of course unknown, the big investors make their money calculating these values as best they can.

Calculating R is hard to do precisely for an amateur (such as me), but E has a nice predictable effect. E mostly consists of the uncertainty of the big investors, and the opportunism of the speculative traders.

I mostly do reactive investments based on stock that has just moved in some significant way that companies that I have a lot of fundamental knowledge in (mostly IT industry companies).

The way it works is I make a bet on whether the cause for the stock move has any fundamental effect on the future of the company. If I feel I can make that bet more accurately than guys reading the news sitting in cubicles analyzing graphs and industry summaries then I assume I can make a ~5%+ profit on a trade (with a chance of a similar loss of course).

For example: The launch of the Kindle Fire by Amazon was a complete flop. This was widely anticipated, I felt very confident in that it would flop. The AMZN stock dropped as people lost confidence (E) in the Fire and I bought when I felt it was pretty much solid that everyone agreed that the Fire had flopped. Unfortunately I was naieve, and a few weeks later Amazon released its earnings report that undeniably confirmed the flop, and E was eliminated, and R adjusted causing another drop. At this point I was in the negative, so there was a lesson for me there. Anyway, my bet was that the Fire was just some largely irrelevant side strategy for Amazon. Sure they invested too much, and their chance for rivalling Apples iPad or whatever insane plan they had was ill conceived, but it was just something they had to try. The big plan of Amazon however did not suffer from this failure. They were still on track to becoming the force of nature they want to be so the lack of confidence (negative E) of the daytraders was in my opinion unjustified. A few months later this showed, the dip of the Fire was gone, and if I sold then I would've made a cool ~10%.

I didn't sell though as I thought Amazon was a cool company to hold stock in for the long term, so the bet was just a gimmick to get some long term stock for cheap. I ended up making a lot more money on AMZN than I expected as for some reason the fact that Amazon makes a lot of money on AWS was big news to the financial world and slapped a big markup on the stock after which I sold, because I don't pretend to actually know what an Amazon stock should really be worth.

Sometimes brokers don't allow you to margin (borrow against or sell short) stocks below $5.

Sometimes funds have covenants on not buying stocks below $5 because they are considered penny stocks and funds want to claim they focus on quality.

Surprisingly, couldn't immediately find a good academic research paper on behavior of low-priced stocks. A priori -

- very expensive stocks might be a little cheaper than they otherwise would be, high cost makes them harder to buy for individuals and low cost funds.

(e.g. if Berkshire Hathaway stock is $200,000, an individual with a $100,000 portfolio can't buy it, and even a pretty big portfolio can't fine-tune exposure with a lot of granularity. Hence, some enterprising fellows started funds that would just own Berkshire and sell shares in smaller increments, and Buffett got annoyed at that and launched Berkshire B, which sells for $146).

- very low priced stocks might be more volatile and show interesting behavior at certain thresholds, penny stocks below $1 might be overpriced since it's a hotbed of speculation, stocks that cross $5 might experience some excess selling so they might be underpriced, on the other hand they might experience some short covering as they become unmarginable for some.

But anyway, companies usually aim for a stock price in the $10-100 order of magnitude because that's the area where even relatively small investors wouldn't have a problem fine tuning their exposure.

Price < $5 is usually an indication it's well off its high.

A stock is just an arbitrary fraction of the capital stock, therefore the price in absolute value of a single stock is completely irrelevant. Suppose a company has a market value of $1,000. The company can divide its stock into 1,000 one-dollar shares, or into 500 two-dollar shares. Either way in makes no difference as far as the total worth of the company goes.

Thank you for the elementary school lecture. You are completely right: This is why companies are so eager to do a stock split at $6. It's all just arithmetic!

Which comments? You do realise that the order of comments is influenced by votes and how recentley they were created? Either give us a proper explanation or a link to the comment you are refering to.

Stock splits are only about convenience. Imagine if all we had are $100 bills. Buying groceries will be quite a hassle. The government then decides to do a split and let everyone exchange their $100 bills with 10 $10 bills. Everyone still has the same amount of cash but it's now easier for the average consumer to buy their groceries.

How would the existence of a $10 bill mean the economy is in trouble?

This is a too simple analogy. Some exchanges wont list a stock if it's under $1. Some brokers wont let you short under $5. If grocery stores took no bill smaller than $1 , would you really want to cash your $10 bill into pennies?

Price per share is irrelevant. Going from 2 to $4 is that same 50 to 100. Typically however, companies like to keep their stock price higher as it seems more attractive and a low share price seems less valuable than I.e. $100/share. Market cap is completely separate, all depending on number of outstanding shares.

There are more important practical reasons for slightly higher share prices than appearances. A lot of major brokers (eg Fidelity, Scottrade, TradeKing, TD Ameritrade) won't allow any margin on stock prices below $2 or $3, and often brokers adjust the margin requirements based on price brackets (eg $5 to $3, X% capital requirement; sub $3, no margin allowed). That can cause a margin crunch on investors if the stock falls below $3.

There are also important practical reasons for low share prices - there are high fees and commissions for trading shares in lots smaller than 100.

This makes stocks at low prices attractive for small investors, unlike the Berkshire of old with a price of 100k...

A 32 core zen would be extremely interesting, assuming it is affordable for mere mortals. It would be a great base for experimenting with developing multi-core algorithms.

{kind=link}

- problems with scalable 10nm, 14nm might be the next 28nm for a while and all manufacturers will catch up, obliterating Intel's major advantage

- Zen might be sufficiently competitive with older Core chips on performance, power and price, better on GPU side (hopefully not another Barcelona)

- all major consoles run on AMD

- Polaris vs Pascal

- they might survive until 2017 and have cash to produce new chips