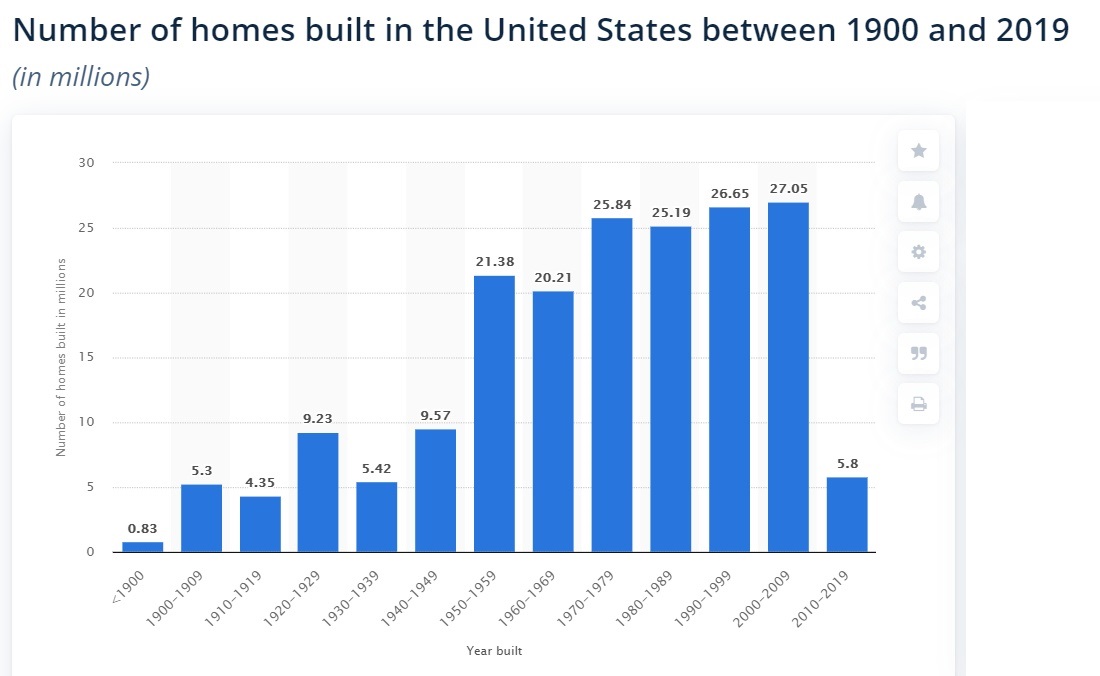

From 1950 to 2008 the USA built ~25 million homes per (edit, not year) decade. From 2008 to 2018 it was about 7 million. In recent years building rates have mostly recovered but there's still that gap in production combined with everything else the last handful of years.

This isn't to discount the shift of ownership from human persons to corporate persons, that's a factor too. But just numbers of available houses versus population plays a role.

If home prices are going up, that means that demand exceeds supply. If home prices are going up everywhere that means demand is exceeding supply everywhere.

If homes are a good monetary investment, that means home prices are going up, which means supply is not keeping pace with demand.

If home prices are going up at a rate faster than wages, then they are becoming more expensive for our children. Not in a round-a-bout way, but in a direct causal relationship way.

Homes can either be affordable or an investment, not both. If homes are to be affordable that means more need to be built.

> If homes are to be affordable that means more need to be built.

Try pricing what it would take to buy a plot of land and build a home on it. In some places there are very expensive local regulations that must be satisfied. However, just the base value of some land with utility access, physical materials, and labor to assemble the home is "unaffordable." If the difference between the cost to produce a home and the sale value of the home was larger than there would be more home builders. If reducing the cost of housing is important to you than you should focus on ways to reduce the cost of producing homes.

In 2019 I purchased land in Mt Washington, about 15mins outside downtown Los Angeles for $200k. My father is a builder back home in Australia so we know more about building that most. Even the after 3+ years, we finally received permits. The city is making us widen the road ($75k), extend a water main 12 feet ($75k), move 3 power poles (can’t get LADWP to tell us what that’s going to cost yet as they have to design it) and install a septic system. We are going to go all electric so we don’t have to run gas lines.

The amount of bureaucracy is insane. Often times we have been the go between for different departments of city that have offices in the same building as each other. They all point the finger at each other. Can’t get answers to the power pole questions from LA DWP without Bureau of Street Lighting, Bureau of street lighting won’t do anything with out LA DWP etc… it’s madness.

House will be 3200sqft, very nice with a pool but lots of value engineering (thanks to my dad). Construction budget is $2m. Will be getting a construction loan. Requires monthly income of $35k combined. Lucky I’m doing this with my twin brother, so we might just be able to afford it, but currently can not due to interest rate rises since we started. Swinging big.

Bank appraised finished project at $3.5m.

My take away from the whole process is that LA infrastructure is terrible, and the city has effectively made it impossible for new construction by family’s. LA DWP single handedly cost us a year in permitting and its incentives are just so not aligned with home owners. My dream is we can go solar and batteries and tell them to get lost. I now have a real respect for what Starlink is doing. Down with the entrenched utilities!!!

You have to be rich to build a house in LA. Renovation is the only real option for individuals. Which just drives up house prices. New houses built is the only way out I think, and the government seems to only be making it harder.

I've looked into building in Portland OR. I don't think we're quite as bad as what you describe (except for the bureaucracy which is spot on), but I came to the conclusion that there'd be about $100k in fees. Just the fees to be allowed to hook up to the city sewer I think came out around $30k if I understand them correctly. (It's possible I'm missing something. I'm not an expert.)

For some people that's probably a bargain, but if you're not wealthy it's a lot of money just for /permission/ to do something.

In my AHJ, if the sewer line passes by your property YOU HAVE TO PAY DISPOSAL/SEWAGE FEES (based on water usage), even if you have your own functional and safe septic system.

A lot of what you are describing is regional issues for costal cities. My specific comment was pointing that {Base land + Materials + Labor} is very expensive, and while addressing these fees and red tape might be important, it's not the whole cake. I was also targeting a more modest experience.

In Texas it might be $40k land (varies by size and location), $250k for construction ($115/sqft * 2250 sqft), and maybe $50k for utilities/landscaping/driveway/permits etc (varies by taste and location). So $350k for a house in a state with a $70k median household income. With a 20% downpayment and a 6.5% interest rate this median family for a median house would spend 1 year salary on the downpayment and over a third of their gross income on the mortgage. If they had a typical amount of debt from cars, credit cards, or student loans their DTI would be too high to qualify.

EDIT: To my original point. Saying "Build more homes" is an oversimplification. Homes are largely priced such that they equal {Land + Building value}, and new homes are largely priced at { Land + Construction costs + reasonable margin for developer }. If you want to build more homes, look at how building can be cheaper. There are some clear low hanging fruit you are describing in your LA experience, but even where the regulatory environment and labor costs are more reasonable the numbers don't crunch well. Let's have conversations about how to reduce the cost of producing housing. Getting cost low enough that the median household income can afford new construction would absolutely drive up the number of homes being built.

I have built a personal house with two brothers — one my own Twin — and wow ya'll are in for an undertaking.

I've built, all-together, about similar budget (for two houses with brothers) and I don't even think I have enough energy to build my own house, now. But gonna try, on some land in a county with minimal regulations.

House Twin and I built was in a Historic District, which was the biggest nightmare of the entire construction. We literally did the rebar and formwork and roof and plumbing and electrical. And they made us re-do windows and other such bullshit to "be in conformity with the neighborhood, but without giving the impression of being historic itself." JFC, make up your minds [worse than any HOA nightmare].

> move 3 power poles

> House will be 3200sqft

> Construction budget is $2m

> impossible for new construction by family’s

Sorry, but this looks like one of the most incredibly out-of-touch rich people comments I've ever read. You're building a freaking castle in the middle of the city, moving roads around, and then you go on to say "families" can't build??

Maybe you're right and even building a modest home in the suburbs is harder than it should, but your project is definitely not proof of that.

Choosing to build a giant home in the LA hills with a budget of $2M just for construction is the out of touch rich people thing, not the additional issues with the city.

I think you missed my point. Our land is super cheap for LA (hence all the infrastructure work). Even if we built a garden shack on it, we’d have spent $600k. How could a working class family ever afford to build a house like this?

If the goal is more houses, make them faster and easier to build. Less red tape, less infrastructure requirements. Otherwise it’s only well of people like me that can (barely) afford them.

Now I’m sure you’ll say “don’t live in a coastal city then”. That where the work is. And it’s also where 40k homeless people live. Connect the dots. We need more houses. There is land to build them, it’s just insane to do that under current rules.

If home prices are going up everywhere that means demand is exceeding supply everywhere.

Only if the houses are selling at the higher price. There are a lot of empty, unsold houses where the owner is refusing to reduce the price. Property economics is weird.

> If home prices are going up, that means that demand exceeds supply. If home prices are going up everywhere that means demand is exceeding supply everywhere.

Misses the fact that homes are bought (most of the time) with borrowed money and leverage.

You can either look at that as increasing the supply of money or lowering the cost of money, and its reflection in housing prices.

Sure, asset bubbles are a known phenomena. Zero-interest rate policy made a lot of big bubbles. That doesn't mean there are enough units built, or that there's no real demand. (It means the opposite, the bubble happened because it is such a good investment.)

Another explanation is that the average new house costs more than it used to. Housebuilders have chosen to build bigger homes at a higher finish level because there's more profit in it. New affordable housing is becoming rarer.

Another factor here is the rising costs and complexity of zoning/permits. In my area it will cost you 6 figures just to put down a foundation with the paperwork. This puts a floor to how cheap a house can be and what is financially viable to build.

Demand for homes may exceed supply but ask what that demand really is.

A big chunk of that demand is for 2nd or 3rd or even 4th properties as investment rental properties. Can’t afford a house in the sf Bay Area, no problem, go buy 4 investment properties in the Midwest! I know people who’ve done that.

Also look what houses are built, they aren’t starter homes in many areas. They are “luxury” (luxury per home marketers, sq ft, and price, I won’t go down the rabbit hole of what I personally think).

That makes zero sense. Do you think those rental units disappear off the market? There isnone unified housing market, rent and buy. People can still rent if they can’t buy.

Building more will inevitably fix the housing market, even if one investor owns every single new house.

Question: Adding out of state investors to the demand pool ( that additionally can out bid locals) will likely

A. Increase house prices

B. Decrease house prices

Question 2: adding rent seeking middlemen between people and housing is likely going to

a. reduce costs for housing

B. Increase cost for housing

So there’s a finite supply of house, investors from out of state are now competing, increasing demand but also have deeper pockets. Now the locals who would hav bought are forced to rent, increasing demand for rentals. They investors aren’t going to take a loss so they’ll rent at the rate that gives them the expected return, which they get because of the high demand they helped create, with rental prices justified relative to the sales price that they themselves jacked up

When investors build with the intention of renting, they typically build at higher density. The only real barrier producing artificially high demand are policies preventing high density building. This is also the thing which makes housing an attractive investment option in the first place. Improved policy will fix both of these problems.

> If homes are to be affordable that means more need to be built.

I'm not convinced it's that simple. Houses aren't widgets that you can flood the market with an unlimited supply to drop the price as much as desired. Homes cost a lot to build and use limited resources, which means at a certain point building more increases the cost.

Picture a city that is building only 1000 homes a year and then they decide to start building 10,000 a year. Will the prices drop? If the prices were very high due to excess demand, probably not because there is enough demand to absorb those 10k units without meeting all the demand, so prices won't drop.

Ok then, let's go all out and build a million units (let's imagine that land is somehow available for that in this thought exercise). Will prices go down? No, prices will go up! Ask anyone trying to build a home in a tight market, labor prices are extremely high because there is so much demand for a limited supply of labor. If this hypotetical city tried to build a million units, labor costs will skyrocket and so will the price per unit.

There are no efficiencies of scale left in a mature industry like house builing. Building more doesn't make the per unit cost cheaper, it actually makes it higher due to labor availability.

Housing is still a very conservative industry, productivity is very low, because any transformative technology only works at scale, but the US is super big and even the population centers are low-density, in many jurisdictions, zoning basically mandated labor intensive low density housing for decades, etc.

Land is available. What's not is infrastructure, and economic surplus to maintain all the required new homes and infrastructure (roads, pipes, power grid, etc).

Housing suffers from the same curse as the transit infrastructure, or the nuclear industry, enormous economic and political inertia keeping/prefering the status quo, any new projects are small, low-efficiency, lack economies of scale, lack innovation (because copy-paste building just one more is the lowest risk thing).

Look at the recent California zoning remedy program, so few real estate developers are taking it, because it turns out that those small local markets are basically incompetitive cronyist distopias, and it makes no sense for them to get into a fight with the zoning/approval board.

> If the prices were very high due to excess demand, probably not because there is enough demand to absorb those 10k units without meeting all the demand, so prices won't drop.

Supply and demand aren't quantities, they're functions. You may be trying to say that demand is inelastic around the present point, but I suspect it actually isn't.

So in those 7 decades there has been build 175 million houses. Population of usa is around 350 million. Most people probsbly also not living alone and some houses that were build before 1950 probsbly still are in use just maybe modernized.

Not familiar with USA market but wondering: Are current houses just more fragile and fell apart within 50 years?

>Are current houses just more fragile and fell apart within 50 years?

Obsolescence gets overlooked but it is important. Not only are houses often poorly constructed, but many are simply no longer desirable. For example in my area, anything pre-1960 is likely very small, possibly without a garage, and may only have one bathroom. The modern homeowner wants something better. Houses in the 1970s were frankly, weird. They don't fit modern tastes at all. Many houses built in the 1990s are falling down already because they were so poorly built. So my point is, you have to take into account not only the top end inventory number, but also that lack of desirability is a real thing that drags down actual available inventory.

Dude - I work in real estate, I know exactly what I’m talking about. I can take you to housing developments in my area built maybe 25 years ago that are falling the fuck apart. Hell - my ex-wife lives in a rental house less than ten years old that already needs real work. Are standards for electrical, insulation, etc higher? Absolutely yes. But don’t you go telling me I don’t know what I’m talking asking about, especially when you are misconstruing what I wrote.

Don't forget that houses get torn down and rebuilt. It doesn't happen often but it happens.

In the US, modern houses tend to be larger, have better insulation (from what I've experienced), but can be cheap in some aspects (e.g. interior doors tend to be hollow, whereas older houses typically had solid doors). Overall though, I'm not sure if new or older homes were better built. I know some really well built old homes, but some very poor built ones too, and this goes for modern homes as well. Most should last 50 years though.

Modern homes have much better insulation and energy efficiency (like LED bulbs), etc. But I think it's also true that a lot of builders can get away with cutting corners, and the materials that go into homebuilding are also often of lesser quality (like wallboard from China that outgasses toxic sulfur fumes). Modern plumbing is mostly snap-fit plastic tubing rather than copper pipes. It's a LOT cheaper to install. Supposedly lasts as long or longer, but it's still shitty plastic.

Shitty wildcat builders throwing down entire subdivisions of deeply defective homes is a serious problem in the Phoenix area, I know that for a fact.

This is not new. My 1954 bay area house: the builders mixed scrap wood in to the foundation concrete to make up for undersizing the order, broken roof boards were patched with coffee cans and other garbage (coffee can had a 1940s date, it was there since built). These are just the most obvious examples.

You're making too many assumptions from such broad data. No, houses don't generally fall apart within 50 years. But most houses built 50+ years ago are small by modern standards, and many have been torn down and redeveloped since then. For the ultimate peek into this phenomenon look at Tokyo, where the lifespan of a house is short and any given plot of land is rebuilt several times per century.

Also, of course, one should keep in mind demographic shifts. There are many small towns (and even some city suburbs) with cheap empty houses that many people would never willingly occupy because there are no jobs there.

Also areas like East Cleveland that have a notorious reputation. Even if in that particular case the city was built by John D. Rockefeller, he is even buried there.

Ah yes, East Cleveland. One night I was biking home, one of the locals took note of my weakened position with a flat tire and that my skin color denoted I was not from the neighborhood, and they put a gun to my head. If you buy there, I recommend availing yourself of Ohio's constitutional carry provisions.

There are a lot of old abandoned homes. I would never live in a home built before 1978. Almost certainly that home is full of lead-based paint and asbestos.

You don’t have a choice in some areas, like the south SF bay (unless you are a multimillionaire). The sources of asbestos are well known and they can be removed cleanly and safely, and lead paint should have been painted over by now with more than a few coats of modern paint — which you can safely touch and lick, if you like.

You never remodel or have to repair holes in the walls of your home? In my experience, we would have lead based paint particles floating all around the house from all the projects and fixes we do.

Presumably you’d baby proof your home and would address any spots where the paint is flaking or chipping off the wall. Especially if you knew it was an older home.

Honestly unless the lead paint is the topmost layer, or they put so many coats of regular paint on that it’s falling off the wall, the actual risk of a toddler encountering and then consuming the paint chips is shockingly low.

>I would never live in a home built before 1978. Almost certainly that home is full of lead-based paint and asbestos.

We're closing in on 50 years past the 1979 lead-based paint cutoff - the vast majority of homes in my area, and I extrapolate that likely most areas, have been remediated. With asbestos - probably the worst issue in my area is that if you have asbestos shingles you want to remove they are stinking heavy and so cost a lot to dump. I live in a 1915 home that is a great example of houses in my area - has gone through multiple renovations in that time such that the guts are fundamentally new. Probably the biggest issue with these older homes is insulation, as unless you truly take them down to the studs, they are never going to be as airtight as modern homes.

Even here in Czechia, where we mostly build out of brick/stone/concrete (and not wood), ordinary 1950s and older homes are pretty undesirable unless thoroughly modernized. (Luxury homes are a different story.)

One of my colleagues lived in such a multi-apartment block where there was a common toilet for the entire floor, so four households. In freezing weather, the toilet was bitterly cold.

Yes, Americans build everything of wood, rather than cement or bricks, like in the civilized world. Remember the tale about 3 little pigs? After 50-70 years it falls apart and needs to be teared down.

So someone who gets their construction knowledge from a children's fable confidently asserts that an entire country, really an entire continent, just doesn't know how to properly build houses.

Americans use wood because they have wood, it's an excellent building material. The parts of the world where they don't use wood, it's because they don't have wood, they've used it all up. America is covered in forests, Canada even more.

The cost of the frame today is a very low percentage of the total house cost, the issue is more cultural: that there are few people in America who know how to build from any other material, there are few cement or brick factories etc.

I don’t think the solution should be homes aka a scale out solution. It should be to go vertical for higher density. Apartments serve the most people and the barriers to entry are much lower than a mortgage.

I hear your point, and I wonder what the stats are on livability of these vacant homes. Cause I bet the other side of the spectrum is true too: luxury units that just sit there because the price point is so high.

But beyond that, housing as investment property alienates people from the natural reward of caring for housing. We ought to be leaving into and communicating peoples' natural desire to make home livable. Instead we rip people from it, we punish people by forcing them to switch apartments when they're perfectly happy.

So many people effectively live in in slow motion life long exile.

Taking a mentally ill fentanyl addict from San Francisco and dropping them in a condemned house in Scranton PA is not actually going to solve the problems you think it will.

There’s actually a philosophy called “housing first” that says you cannot solve those other problems without housing those people.

99 percent invisible did a podcast series on the reality and nuance of homelessness. It is the best take I’ve seen and really opened my eyes on a number of things. Episode 3 covers housing first, but I would recommend going through the whole thing.

Exactly! It often does solve those problems when combined with other necessary resources like mental health care and help finding community and meaningful ways to occupy time, like getting a job or going back to school.

Housing first is evidence based too. And cheaper than emergency services. And when done right much more dignified.

Yet here we have this society full of punitive know it all skeptics who don't actually seem care about the evidence quite as much as they care about dominating social structures that help them feel better about their insecurities.

In a lot of cases they wouldn't have become mentally ill or a fentanyl addict if they weren't homeless. Yes, addiction drives tons of people into homelessness, but homelessness can also cause addiction since a homeless life kinda sucks.

It would save a lot of money on demolition though. The plumbing, cabinets, appliances, doors, ducting, and everything not fixed to the frame would get removed for free and it would be very easy to bulldoze after the house catches fire from people trying to stay warm inside without paying a utility bill.

Some of the school districts near-ish me are so desperate for teachers that they will up and just give teachers a house and a car. It's not prime real estate and not a new car, but you get the gist.

There are hardly any takers.

As has always been true in real estate: location, location, location

Hmmm it might not have anything with to do with the massive money printing and forced low interest rates of the last decades...?

Its not only the us dealing with this.

In many Western countries a large part of the population has been incentivised by both tax cuts and monetary policy to own property that it's become very hard for governments to change those policies to again make houses affordable without huge cuts of the wealth of their middle-class.

We don't know if that is the primary cause though. The US population was growing at a quicker rate for much of it's history, and that population was more rural, and a number of other reasons we can't rely solely on historical data for our predictions of current behavior. With a closer to zero population growth rate and a more urbanized population we would expect there to be fewer houses built.

Additionally, the pure supply and demand argument is insufficient because it does not explain why we have failed to create the additional supply to meet the demand. In a pure sandboxed supply/demand analysis with no other factors, we would expect to see supply increase as demand increases since in theory it means building homes is more profitable. The high school version of supply/demand is that they balance eachother eventually and the timeframe over which that happens is influenced by the elasticity in price of the good in question. Something about how the housing market functions has changed in some locations.

location, location, location. Much of the housing price increase has occurred in areas that are doing well economically, but have more or less maxed out the building density currently legally allowed by zoning. today you could build so many houses in Detroit and yet that wouldn't really ease the housing crisis in a place like the Bay.

there is also, at least anecdotally, a shortage of skilled tradespeople across construction in general. post-2007 basically reduced the incoming pipeline to zero, and so now there is this missing labor cohort that would be really useful right now.

Yep I agree that a large contributing factor in all of this has to do with location.

The shortage of skilled labor is another instance where we need to ask why supply is not meeting demand. I think in the case of the supply of skilled construction workers it is not difficult to come up with a plausible explanation that doesn't require any malicious actors.

Anyway, I'm not really trying to make a political point or give everybody my own pet theories as to how this happened. I'm mostly just trying to make the point that the way this issue is generally discussed in the media is economically illiterate at a pretty fundamental level.The observation in the media that supply is not meeting demand is worthless on account of that not being a meaningful statement.

Wages for construction workers have not kept up with inflation, much like other fields. Unless you're a Master - tier specialist in your field, you will probably be making at best $15/hr to $25/hr with minimal (if any) benefits.

There's simply few reasons to enter the field and risk long term health issues when you can make the same amount, or better doing paperwork in an office.

we also had a whole new category of job (gig economy) and a massive increase in a related category (delivery) show up for unskilled work. In general there seems to be a labor mismatch now, and existing regulations certainly don't help (e.g. you need to not have smoked weed in the last six months to hold a CDL to drive a truck around, and these days that probably eliminates a good chunk of that skill segment)

Additional supply did come on, and has dropped recently in response to rates.

It's really not more than high school supply/demand. There are just a good number of factors which make up each at each location, and at least one of them is large and unpredictable (interest rates). There is always a lag on the supply side because only so many houses can be built at any time. It's the same for many commodities like oil and gas.

Actually computing a good supply or demand curve has always been the difficult part, not the theory. But supply lag and interest rates make up a big component of property supply and demand.

I think that's what the person above you meant as well, that prices being high due to a lack of supply is not controversial nor is it very interesting.

Yes and with supply not meeting demand at least here in York county pa and Baltimore county md.. bidding wars just started to be the norm again and prices are increasing. I bid on a 200k home (a real fixer upper to flip in two years after living in it & remodeling it) last weekend it had 20 bids and I lost out to an all cash offer(supposedly per my real estate agent). That same weekend a 40 year old log cabin ($430k) had an open house where 30 showed up and it was sold within 8 hours.

Up until this month prices in this market were declining and homes sitting on the market for weeks to a month or more with lots of price drops.

It's weird spring comes around with interest rates just as high and we are back to bidding war frenzy that was 2021/half of 2022.

Would be interesting to see how different the costs and difficulties compare to the prior building boom. The red tape involved in building today is off the charts - prior generations had a much easier time building houses.

This article is missing perhaps the most important graph, which is median income to some common monthly payment metric (e.g. average monthly payment for a 30 year mortgage with 20% down).

Reason being that the article mentions interest rates, but then just shows graphs comparing to sales price. Ironically, showing a metric that took interest rates into consideration would probably highlight why the current situation is even worse, because rates have skyrocketed but prices have only come down a little bit. Of course, as others have mentioned, that is because overall sales numbers have collapsed. Owners won't sell at a loss if they don't have to, and overall employment numbers are still high. But over time people are forced to sell for various reasons, so in 5 years prices will either go way down or stay flat as wage inflation catches up.

I think these days, proportion of cash buyers in the last several years was highest in history - inequality did it's job and most people who can afford buying a house, can afford buying it on cash. And before, prices were much lower so most certainly won't fall down back again, forcing banks to invoke foreclosures. So i don't even think rising rates or falling prices may cause a snowballing collapse like they did in 2008. It's permanent - inequality and urban concentration locked next generations out of affordable housing and there's likely nothing that can be done about it.

But in Europe, we lived like that for at least two generations now. This is what a stable state, fully urbanised society looks like. Here, it's typical for someone with a mid-level management position in a bank or an IT company, with million dollar net worth and managing dozens of employees, ride a train to job an hour each day, because they can't afford to rent in the city. And people who live in the city are simply those who's families bought pre-WWI. Or those with a regulated rent contract passed down generations from the 1950s, being an overwhelming portion of the family's effective net worth.

"Cache buyers" does not really mean people buy houses with their disposable funds. It means only that the deal does not involve a mortgage contract. The deal can still be financed through a loan, just not a mortgage. During the highly competitive market in 2021 people had been takin such loans to make cache offers and beat competition [1]. Also we had massive emigration from the states with high RE prices such as CA and NY to TX and FL, with much lower prices. These emigrants might have had enough equity in their old houses to buy a whole house in the new place too.

But it would really be great if your assertion had been true, in 2021 alone 6M houses had been sold so there would be at least several million people so rich that they buy houses like groceries.

People do eventually sell due to life events, even at a loss, in fact I'd say that is probably the primary cause of sales rather than anything financial in nature. At least anecdotally, I've sold twice and both times I would have had to do it even if it was at a loss.

However, you are correct that the price is pretty sticky at the moment.

In my area, friend groups are organizing into LLPs and buying up houses for investments. Individual people home shopping have to deal with this kind of competition. Houses are bid out of their price range and become airbnbs.

Yep. Why live in a house when you can charge someone $1200/nt to stay there and a $600 cleaning fee? (Basically every house that can sleep more than 6 people in the northeast)

When I first looked at this graph, I did not have much emotional reaction.

When you look closer, each unit on the axis represents 1 year of a person's income. Each line on that graph represents 2000 hours of life toiling for a basic living necessity.

The forces that drove prices are over. Low interest rates, and low productivity due to COVID-19. As interest rates rise people will no be able to afford their mortgages. Prices will fall in response.

Less than 10% of mortgages are variable rate. And why would anybody sell their house with a 2% mortgage? They’d need to be paid a significant premium to justify this.

Anyone who is capable of getting a second mortgage will consider holding it and renting it out if they can. The yield is very likely to be higher than the payments these days.

But now that the second mortgage is so much more expensive, fewer people will be able to do it right? More specifically, previously you could borrow against the increasing value of your home, at a low interest rate, to fund the next purchase. This is what everyone on the investment side was doing. With neither of those factors true any longer, it seems this scenario will be less common.

At a higher level, I think this is what the transfer of wealth looked like for the past decade.

> As interest rates rise people will no be able to afford their mortgages

I really wonder how many people in the last 10 years actually felt like buying a variable rate mortgage was a good idea? People on fixed rate mortgages are staying put, and watching inflation deflate the value of their debt.

People might be scared to let go of a house they already bought.

- They might consider going on paying in the hope that rates drop

- They might not be able to buy another house

- They might find rents will shoot up with mortgage, so somehow manage to pay mortgage.

Also, many houses are bought by investors and companies.

They might be able to show higher mortgage as additional expense when filing Taxes. ( Not sure, but that's how I think they do it - someone can explain better )

If a large number of people are unable to afford their mortgage.

Then we have a real crisis coming.

Not meaningfully. Prices are up 60% in 2 years. No chance there is that level of correction when 99% of mortgages have rates cheaper than the current market rate.

Most people finance homes. Prices are overwhelmingly a function of affordability based on lending criteria. See financial engineering, thus see the Fed and real estate financing/banking legislation.

Unless, the very thin chance

1. Owners don't need or want to sell

2. No inventory is added through building

3. People somehow pay cash and support the prices

...or some combinations.

This is to be expected. Sellers are always reluctant to be reasonable when they are on the wrong side of a peak. The raising of interest rates means prices have to adjust. But after so many years of increasing prices sellers are not yet rational.

And yes, some more inventory would help. That said, as the population ages, who is going to buy all the McMansions? Price not only need to adjust to interest rate but demographics.

Prices actually have adjusted and have fallen somewhat.

What life event would cause someone who currently owns a home at a <3% rate to sell?

It’s a once in a generation type of rate. You’d have to be a complete fool or have some kind of crazy life circumstance to sell.

Over 30% of employers in the US exclusively hire remote employees. Post-pandemic it’s hard for me to imagine someone in the home ownership socioeconomic class giving up that kind of leverage advantage to move for a job.

This seems a bit extreme. If you can afford to move, does interest rate really factor in? If rates get worse you’ve still locked a better rate, if rates get better you refinance. Besides, there’s plenty of reasons to move besides for a job (and not everyone can work remotely or get a remote job with comparable compensation).

Yeah, you’re going to pay some more interest if you get a new mortgage, but don’t you just adjust your monthly finances and eat it? As long as you can hit your long-term financial goals, the “once in a generation” rate doesn’t seem so important.

Yeah I think the HN crowd is vastly overestimating how much people care about rates. Most people are not perfect financial optimizers - they’ll just pay whatever they can maximally afford per month for a house that most closely matches what they need for their present life. Few people are coldly rate rational.

You only have to look at what people pay for car loans to confirm this.

They care about what they can afford each month. They indirectly care about the rate. The sign on the starter home neighborhood near me was $719/mo when I moved here in 2020. It crept up to 850, 970, 1100, and then they changed the sign to not have that information. Same houses.

Hopefully only sane mortgage products continue to be used so it doesn’t end up like automobile loans. Aren’t most car loans 72 months now? That’s what is required to get the monthly note affordable for most buyers.

It’s not about optimizing it’s about cash flow. If you get a 500k mortgage today at the current rate of ~7% your monthly payment is about 3500/mo. That same mortgage financed 2 years ago around ~2% is a monthly payment of 1800. For the SAME house you are paying basically double the amount per month.

This isn’t optimizing a few bucks per month it’s about not being able to afford the same house.

Every homeowner knows this and if they’ve ever had the incling to move int rh last year theyve done the math and realize it simply doesn’t make sense. People won’t move right now unless life forces them to.

And I think this type of opinion goes too far in the other direction and essentially accuses the common person of being a complete ignoramus.

> they’ll just pay whatever they can maximally afford per month for a house that most closely matches what they need for their present life

Right, and if you ditch a 3% mortgage in favor of a 6% mortgage your monthly spend goes way less far. You're looking at a loan payment that increases by about 40%.

Right, and further not being perfectly financially rational is quite fine! Finances aren’t the only factor in any decision, nor do they need to be the primary factor.

Divorces, deaths in the family, growth in the family, people move to be close to certain hospitals / schools etc. Maybe one half of a marriage gets a remote role but the other doesn’t.

With remote roles you no longer need two income households. Raise your kids yourself. That statement will get me downvoted, but if even one person is inspired to think that through it’s plenty worthwhile.

Funny thing about that, COVID has removed a lot of people from the workforce and will continue to do so for the next few years. The billionaires at the top of all the tech companies will live to regret allowing the activist investors to spur them into laying off people.

This is what people said about Levittown (https://en.wikipedia.org/wiki/Levittown), the archetype for postwar suburban housing developments in the USA. They did wear out, but the owners fixed them. If the housing is still needed, it will be maintained and repaired and improved.

> Despite the US's deficit in housing ever since, many millions of houses houses have in fact been abandoned. Please explain.

Sure. No one wants to live in those areas where the houses are being abandoned, or government regulation makes bringing them up to code financially non-viable.

Not based on the one I’m living in. It’s the definition of lipstick on a pig. Serious fundamental problems with a nice looking exterior. It’s been nothing but problems for the last 8 years.

Every bathroom was finished with normal drywall instead of the water resistant stuff. The vents in the upstairs bathrooms just vented into the attic space leading to moisture issues in up there. There must also be an issue with either the framing or the foundation because we have the ceiling separating from the drywall in almost every room in the house in addition to cracks developing in the drywall. I know some amount of settling over time and cracks are sometimes normal, but I’ve never seen them this frequently. Our floors are also uneven and you can feel them moving as you walk across them.

In the bathrooms they also picked the cheapest bathroom fixtures imaginable. They looked decent at first, but it was also quickly corroded and the lights literally fell apart. We have one of those fancy three head shower setups and we discovered that the main shower head corroded and broke off inside the wall when our youngest innocently asked us why it was raining in the dining room. We also have water hammering issues when running the washing machine because they didn’t bother to put in a flow arrester.

On the exterior, our driveway and sidewalks were all laid with insufficiently packed base material. These gaps and buckles are reaching the point where we have to fix them or risk liability when the mailman trips over them. Our gutters were incorrectly installed and they have been slowly leaking down one corner of our house and we’ve found water damage in the basement due to this. The foundation in the garage also has done some settling because the stone work at the base has large cracks developed in it. In addition, our windows and doors are really just polite suggestions for the wind to stay outside because they picked such cheap options. You can literally feel a breeze through most of our windows.

I’m sure there were other minor things which I’m not thinking of, but the quality between our first house which cost 1/3rd of this house is night and day. The only thing the inspector found was the the cracks in the garage brick walls but those are a facade and the inspector told us it was cosmetic damage and the sidewalk was easily fixable via mud jacking. Those were issues we were willing to take on. There’s no way we would have bought the house if we’d known that there were so many issues. As we’ve been trying to address the issues we’ve been finding, we always seem to uncover another problem that needs to be fixed. Feels like a race we are losing.

Thanks for sharing, I'm sorry to hear about all the problems you're having.

I think a major issue is just water being the root of all evil for house problems and the bigger your house is, the more recent it was built, the more corners were cut. It's all compounded by contractors wanting to overcharge you if you're in an expensive neighborhood and not give you the time of day otherwise.

It's like you could just say, "let's just get rid of all this extra furniture and stuff and live within our means. The kids don't need that many toys." But then the argument falls on deaf ears and you wind up with the neverending complexities of redecorating, contractors, insurance claims and stress.

Agreed. But I'd like to perhaps interpret it a slightly different way. What if house construction was "branded". That is, aside from (possibly uninforced) local standards a company built homes AND committed to their quality.

Given how sloppy new home construction has become, perhaps buyers would trade less home for say 10 years of peace of mind? I realize long term guarantees are tough. Obviously. Nonetheless, the current shit-show seems to be begging for alternatives.

Home warranties were fairly common when purchasing. They are meant to cover things you don't find right away during the inspection. Unfortunately market forces, especially lately, have made these less available for purchasers as competition for houses is too high.

Sounds like it's a race to the bottom. No one can differentiate with better quality goods and work because no one is willing and able to do it.

The lower the price the better. Regardless how it'll cost you later, affect long term value, etc.

If anything it makes the argument to not buy new. Instead go for something in the 10 to 15 yr range that's had the structural bugs worked out but might need updated appliances.

While I understand social expectations run in cycles, families are smaller, costs higher, etc. McMansions had a moment. Unless there are reasonable ways to divide them (e.g., family w/ an apartment for older parent(s)) to me it seems unlikely that moment will happen again soon.

ENTIRE vinyl villages of McMansions will be unlivable. They aren't even built to last the standard 30y mortgage because the builders know the initial buyers will sell and move on. Cheapest possible 2x4's with worst insulation ever known, all covered up in plastic siding. But hey, it's 10k sq ft right?

That's a bit hyperbolic. Inspections are a thing, and modern houses are generally built just fine. And nobody uses plastic siding on a brand new house (well, almost nobody, you can probably find rare examples). A modern house uses hardieplank fibercement siding probably 99% of the time. These days vinyl siding is mostly a retrofit choice, not new construction.

The cheap 2x4s are the most significant point of failure. The houses will twist and warp to many extremes during their lifetimes. The first symptom of doors that won't open/shut properly usually shows in the first 10 years of these houses. In a 1920s home built with domestic timber, that process would take a lifetime. After 30 years, this contributes to all sorts of creaks and leaks. Repairs are questionable and don't last as long because the frame of the structure is unstable.

I had a suspicion you would be downvoted for telling the truth here :-). It's an unfortunate choice between being truthful and being popular..

As I understand it, part of the difference between US and Europe is that US has massive access to cheap lumber, which makes it very cost-effective to build with balloon framing, which is not much used in Europe. US saves a lot on construction this way, but it has consequences for durability.

Lots of "luxury" housing is made with crap materials by unskilled freelancers. There is a ton of skimping on hidden details like missing flashing around doors and windows. You can't trust any home built within the last 25 years.

In my case, the insulation was mostly just air. There is zero insulation at all in my garage in a place with harsh winters and there is no insulation between my garage and the house. My attic also did not have insulation, but that one was cheaper and easier to resolve than all the wall cavities.

Unfortunately we aren’t the first owners. I know some of the issues we are seeing is from shitty diy or contracting from the previous owner, but most of them are from the original construction. One example of shitty DIY is the hardwood floor on the main level that we are currently replacing. The newly installed floors were a bit lower than the original floors so they just covered all the gaps with corner round all around the baseboards. Looks super tacky. But is a fairly minor issue all things considered. We are replacing that with another layer of sub flooring and engineered wood floors to try to reduce the amount of movement you can feel in the floors.

Also, with the american quality level of construction for houses, by then those houses will require major investments and renovations to continue to stand.

Lots of people sitting on 2-3% fixed rate 30 year mortgages are suddenly deciding maybe staying in their current home isn't a bad idea after all. If you need a mortgage to buy a house, what you can afford just got a lot more modest.

Sales will pick up a little; some people will need to move for reasons they cannot avoid. Some people who don't have fixed rate mortgages will have to sell because they can no longer afford the payment. But right now, sales are pretty low.

If you have a second home at 3% that means your first home is paid off. You wouldn’t get that rate for an income property.

There are several good reasons for selling it, mostly emergency or retirement reasons. I would keep it and rent it. Inflation is more than double that 3%, “officially”.

What a great problem to have.

Anecdotal data, regarding value drops. I’m in a 30 fixed at 3% in Arkansas. Houses I was looking at in a new subdivision were around $410 when I was looking, this time 2020. They are now in the $700s, and that’s with the current interest rate. So 3 years of mortgage payments, down payments, you’re looking at an outstanding balance on the loan of… around $300k?

The value drop people think needs to happen probably won’t ever happen. Especially since the USD is turning into Monopoly money due to terrible fiscal policy.

Personally I don't give a shit if people can sit on their house forever at -5% real interest rates or whatever. Just let me build a shack out of chicken wire, 2x4s, and tin roof. If you get to rig the game to get a house the least you can do is let me build something with whatever scraps are left in the financial system.

It's all just a game looking at the charts until the real estate "investment" companies are invaded by thousands of homeless people and the CEOs executed. Are people just supposed to not live anywhere? How long will this last? Just learn from history.

That wouldn't do anything, as there's still a shortage of houses. They'd need to collectively invade and stop all the people involved in preventing housing construction, which is a LOT of people!

We have learned from histories, and we know exactly how to prevent populist land reform. It simply requires convincing half the lower class to fight the other half.

Don't fall for the socialism anti-landlord brainrot.

People have plenty of places to live. This is more about the fact that people want to have the same financial opportunity to own a house. It sucks that the older generation had an opportunity to buy a house that has risen in value, with an area that got gentrified with more stuff around them, and were able to refinance during Covid at like 2-3%, while the younger generation is SOL. This is a very valid reason to address, but has nothing to do with homelessness.

That shortage has nothing to do with landlords, though, and everything to do with shitty zoning and with constructing new homes being incredibly slow and burdensome in most big US cities.

These things happen in high COL areas. Of course the rents are going to rise when people are willing to pay more. This is supply demand. In a lot of cases, property taxes are assessed based on the value, and the people renting and paying the higher rent are actually making more money than the landlord. Also you don't blame companies for charging you for a product that you like the price they do, considering that it takes much, much less to actually make it - are those companies being greedy?

People get displaced, move outside of the area, and find places to live. In some cases, they buy houses in rural areas for a lower cost, and then 5-6 years later the gentrification radius grows and their house goes up in value. Look at Northern Virginia for example of this.

The main that is missing is good public transport system (or government level investment in autonomous driving). In Europe, its natural to commute about an hour or so to work, often from a different town to a bigger city. In US this happens as well, the difference though is that you have to sit in traffic in a car.

Property taxes went up, materials and labor for maintenance went up, and if you bought your rental property during that time, prices were going up, each increasing the costs for many landlords.

What about the landlords that bought property twenty years ago, when prices weren't going up? What's their excuse?

---

Their excuse is that they, as landlords, will charge as much for rent as they get away with, regardless of what their expenses may or may not be. Two identical apartments, owned by two different landlords, one of which costs its owner ~$1000/month, and the other ~$1,500/month will both be rented out for essentially the same price.

There's no need to spill ink on moralizing and justifying why rent's going up. It's going up because you (or someone else) has the money to pay for it to go up, and because you have limited alternatives.

Isn't this a business opportunity for construction companies? Or is the price of building homes increasing at the same pace? Maybe that's a graph that is missing there?

There's a lot of noise about supply, demand, investment cycles, AirBnB, but the elephant in the room is that USA housing is a casino and the banks are the "house", which always wins.

The banks only care that housing prices remain astronomical--the mechanics are not important--so that mortgages must be taken out.

And, as recent history shows, the mortgage casino is "too big to fail" because of the globally-systemic role of mortgage-backed securities.

It’s pretty unusual that we have people approach residential real estate in this hyper-financialized way. It’s a weird 1930s way to inject liquidity, and we have better tools now.

An individual is fucked if something happens to crater the price of their house. Nobody hedges, really. It’s a toxic system.

It’s weird that the insurance industry hasn’t capitalized on this. Make people pay for covering the risk that their house will drop in value, and make money on the fact that the vast majority of houses will rise in value.

in 2007-2009 home prices in the US declined by $6T, plus commercial real estate declined $2t. Insurance companies simply don't have that kind of money. AIG tried to insure only very tiny percentage of that market, and lost.

Almost everywhere in the world, yes. There may be some localized falls, but those are temporary and as long as there's people having to live in a place, prices will keep going up, the whole system is built for making that happen.

Not really. If new suppy growth outpaces demand then prices will drop. Recent advances in robotics may make construction much less labor intensive, crashing prices in many areas.

Where is there a place where prices have gone down (and stayed down) in practice for a long time? I've been waiting for 20 years to get a "bargain" and except for a small area in the US and some very short lived downs elsewhere, that just never happens.

> An individual is fucked if something happens to crater the price of their house.

If they've already paid off the house and they want to sell it without buying another house, sure.

If they have a mortgage on the house, someone gets screwed, and that someone is the bank that issued the mortgage. The mortgage is secured by the house. You can just let them take it.

> If they have a mortgage on the house, someone gets screwed, and that someone is the bank that issued the mortgage. The mortgage is secured by the house. You can just let them take it.

If you have 25% equity in the house, and something happens that knocks down the value by 30%... the person getting screwed is you.

OK, you have a $750,000 mortgage on a $1,000,000 house, plus $250,000 in equity.

Then the price declines and you have a $750,000 mortgage on a $700,000 house, plus $175,000 in meaningless equity.

You can sell the house and pay the bank $50,000, screwing the bank, or you can deliver the house to the bank and pay them $0, screwing the bank much harder.

Meanwhile, you've lost... the opportunity to take out a second mortgage against the equity you had in your house? What was the equity doing for you?

That equity was only useful to you if you had the option to sell your house. If it was your only house, the equity concept wasn't all that meaningful, as applied to you, to begin with.

Try changing the numbers. You have 100% equity in your house and the price falls by 120%. (What happened?) Are you getting screwed? How?

You have 70% equity in your house and the price falls by 100%. Are you getting screwed?

> You can sell the house and pay the bank $50,000, screwing the bank

Prepayment doesn't really screw the bank.

> or you can deliver the house to the bank and pay them $0, screwing the bank much harder.

And wreck your credit in the process-- and perhaps even owe the money, depending on whether your mortgage is non-recourse.

> Meanwhile, you've lost... the opportunity to take out a second mortgage against the equity you had in your house? What was the equity doing for you?

Meanwhile you've lost your entire down payment and your ability to purchase another house now. You either have to take a credit hit walking away and forfeit the down payment, or just stay stuck where you are now overpaying for a house vs. current values.

The hedge is that everybody is in this predicament and that is what makes it too big to fail, that the state will always support the bank's to prevent a total collapse. It's a collective hedge.

that's good old fashioned predujice, short-termism, close-mindedness.

they just don't want to live next to anything (which I get), they don't like change (sure, I get that too, buy that's how you get historical landromats) then they realize they can't get that (as you would have to buy the land to keep it from being used), so the next best thing is to make it as similar to theirs as possible... (which ironically makes their house worth a bit less, because of increased low-quality supply leads to slightly lower price locally)

increasing density leads to having higher-quality services around, which would increase value

It’s TBTF because it’s the source of the vast majority of household wealth. We turned housing into a retirement program, stealing from future generations.

Home prices are going up because there are few 2 bedroom starter homes being built. Everything in this area is 4-5 bedrooms with 3-4 bathrooms. They really are quiet massive

Interest rates jumping from 1.2% to 4.5% had zero cooling effect on house prices in my area. Probably quite a few people are still on existing fixed mortgages.

Prices have jumped, as a double whammy.

It’s all about supply: there is very very little and it’s a desirable area.

Even if rates stay at around 4-5% in a few years when all of the low-rate fixed mortgages have ended, prices will have risen, and I would guess all that would happen is a slight abatement of rises, not a reduction.

When the interest rate goes up that fast existing homeowners are less inclined to sell because their monthly payments will go way up buying a comparable house elsewhere. So you end up reducing supply when it happens so fast and so much.

Part of the problem is that governments erode savings through inflation. They can't raise taxes much more, but insist on printing more money. The only way things balance is through inflation.

Houses have been a safe place for people to put their life savings into. So think of it as a house + plus a savings account in one.

We the HN community are engineers, how can we find a solution to fix this? My thinking is we need a portal to advertise affordable housing or starter homes. Housing is the basis of the family.

Averages are misleading. Maybe one end of the market is driving the average up or down, but the other parts are a lot more in line with more recent historical norms.

Do not despair! The best thing we did was to find a good realtor, who knew a good lender, and they gave us the truth about exactly what we needed to do to qualify for an FHA loan. A down payment is no longer necessary; for US citizens.

{kind=link}

This isn't to discount the shift of ownership from human persons to corporate persons, that's a factor too. But just numbers of available houses versus population plays a role.