I love transferwise, depend on it often. I don't get the rebrand, their old name was descriptive, easy to google, and from all perspectives really good. The rebrand won't change me using it, but I really can't see the positive in this.

Prediction: zero negative will come out of the name change or redesign, and three years from now they'll be bigger than ever. I'm long on them and they haven't even IPO'd yet. Can't wait for them, and Stripe.

Seriously, have you ever seen a rebrand negatively affect a product? Rebrands have to be thought about retrospectively: you need to think whether it would make sense to go from the new to the old. Number26 for example rebranded to N26 and in retrospect it was an utterly obvious move.

Wise to Transferwise would make no sense especially if they are positioning themselves as more than a PayPal alternative. So this is a good rebrand.

And the generic name isn't a problem, any more than it was for Square. It's a shame $WISE is taken though.

> Seriously, have you ever seen a rebrand negatively affect a product?

I think there is an example in Europe. myTaxi has been rebranded to FREE NOW. The change has been dictated to free the brand from just the taxi business connection. But I believe it was unfortunate, at least for their taxi business. I don't have hard numbers, but the new name and logo seems to be random, completely unrelated to taxis, so when you see a car with it, you have no idea that the driver is a taxi driver. It's 2 years now with new name, but they iOS app is still named: FREE NOW (mytaxi). Me and my friends always have to ask someone "how mytaxi is called now?" because the app is no longer under M in the phone.

Worse for the company is that, since myTaxi was extremely catchy, there came a competitor called iTaxi, and many believe it might had take over some of the clients just because people trying to find myTaxi installed iTaxi instead, as FREE NOW looked cryptic and unrelated to taxis for them.

In Ireland the app went from being Hailo to MyTaxi to Free Now. Personally I loved Hailo. It became a verb and it was common to say "I'm going to Hailo now". Now it's "I'm going to FreeNow... now". It just doesn't sound as smooth. I still use it but I really feel like Hailo was the ideal name.

Hailo sounds like an extremely clever name for a taxi app, since (at least in US English) one might "hail" a traditional taxi. FreeNow seems clunkier to use as a verb, plus it doesn't seem to connect to the service at all. (Unless the taxi ride is free now!)

Yeah, it worked well. I guess the problem you have is, once you're international, your clever name loses its impact. It was a common joke at the time Free Now launched that the taxis should be free alright.

I mean yeah, that's not rebranding, that's just brand suicide. I hadn't heard about it, that's a fun story.

But in general, people used to a brand always cry out how rebranding will kill the brand and it truly has zero effect. I remember people saying that gmail's logo changing would kill it. Then it happened like two more times. Google rebranded Hangouts/Chat/Whatever like fifteen times and they still somehow have users. And in fintech I've seen tons of successful rebrands despite users doomsdaying them out. Simple, mentioned downthread, is a good example.

People just hate change. I mean look at some of the replies here… I hope they'll be able to read themselves a year from now.

> It's 2 years now with new name, but they iOS app is still named: FREE NOW (mytaxi)

On Android it's even more confusing. Some time ago it changed from "FREE NOW (mytaxi)" to "FREE NOW (Kapten)". At first I feared that they were undergoing another stupid rebranding (or tried to do one to Kapten and then went back on it and I missed that). Turns out that was a company they acquired from the UK, which I assume 90% of existing users never heard of before.

Worst one I can think of is ConvertKit's rebrand that was so bad they went back on it(kept the new logo, but reverted the name change because it had some religious meaning), then again, it's not as big of a brand as TransferWise.

Wise is obviously a rebrand intended for IPO, along with their talks of being IPO ready. But Stripe? They dont seems to be making IPO preparation at all. I wonder when will it happen or they are happy now as they dont have to deal with the pressure of being a public company.

> Seriously, have you ever seen a rebrand negatively affect a product?

The pandemic coming along masked it, but I think the Realtimeboard to Miro rebrand did. They went from a clearly defined value proposition in the name to a nothing-word. For software that was installed on desktops, so the name and icon changed.

n=1 but I still have to stop and think which app I want to open for a realtime whiteboard.

actually I had problems with package managers when piwik rebranded to mamoto (or matomo?). they renamed all their libraries and it messed up our package proxy server because of that

Completely agree. They are a fantastic service that (as others have suggested they do as well) I use about once a year and recommend to others about twice a year.

I have no idea if I’ll remember the name change a year from now, and as anything related to international money transfer is already sketchy, a rebrand is likely to make me wary.

It's when grounded design decisions become ungrounded. Sure, creating an umbrella company called Wise - where TransferWise is one segment they're targeting would be a good way to do it, and then launch other products under Wise, but they shouldn't rebrand TransferWise to Wise.

> The rebrand won't change me using it, but I really can't see the positive in this.

Anecdotal but I was somewhat reluctant to consider them as a "bank" due to their name (seemed like a service geared towards money transfer). The rebrand is not done for the existing customers, but for more easily capturing new ones.

Definitely agree, akin to when BankSimple rebranded to Simple. It was awesome as is.

Anyway, hope they stick around and eventually turn into a financial OS instead of folks needing a bank, plugging into underlying deposit accounts in the countries you need.

Funny, in my market “SimplePay” rebranded as “Simple” and I just had to double check my “Simple” iPhone app to make sure it wasn’t the former BankSimple.

It wasn’t. So I guess there must be multiple apps called “Simple?”

Yeah, pretty stupid name, if you want to google it. Why they made the change was explained in the blog post: the old name was too specific and describing only one of their services (the one that they have launched with), that is, international transfers. But they already provide foreign bank account numbers (a.k.a. borderless accounts, which I depend on a lot) and you can keep a balance, and convert money and they have a debit card as well. Almost like banking. And I'm pretty sure they want to get into banking.

Not quite the same - but LikeALittle died a quick death when they rebranded to LAL.com - along with changing their amateur-looking Craigslist-simple type site into some overly clean and sharp looking, which didn't fit with the personality of LikeALittle at all; it was the design that killed it, the designers not actually understanding the implications/consequences of the changes they made - so it was luck that their first design went viral, perhaps leadership hired new designers, ignored the initial designer(s) - if they tried to put up a fight at all to the changes, no idea.

Branding matters. The company is evolving from money transfers to more banking services. The fact that so many are resistant to the change because they consider the company to only do transfers is exactly the reason and the proof for why the rebrand makes sense.

Wise might be generic but encapsulates financial services well and fits in with all the other similar brands like Stripe, Square, Simple, Chase, etc.

Another transferwise fan but I can see it being more high status from the marketing point of view. Like in the old days banks had fancy marble buildings to show they had money and now have expensive domain names. See also stripe vs slash dev slash payments.

Random aside - I'm carrying a transferwise card as my main payment card at the moment and just looking it doesn't say "Transferwise" on it, apart from in small print. It says "Hello World" on the front. I'd not actually noticed that till now in spite of having used it at least 100 times.

There is a common pattern where a startup is named after their main product, grows to the point of needing diversification, and starts being limited by their name.

They offer multi-currency accounts - limit their brand to the transfer part is not descriptive at all :) Also they have enough customers to not worry how easy is to search their name on google.

Agreed. I'm a very happy customer of TransferWise, and I have tested many of their competitors which are mostly awful. But this is unnecessary, confusing and irritating.

IMHO, not a good sign for where the company is headed.

Single words are often used when they don't really have much to do with the underlying product (Apple, Amazon, Mint, etc.) because it can be "branded" for that market.

But with Wise, for example there is already a MoneyWise, BudgetWise, etc., so "Wise" by itself may have issues with those other existing businesses.

Trademarks are granted within specific fields, so they won't have any trouble defending it against people providing related goods and service (banking/finance/transfers) using a similar mark. The won't be able to defend against someone else using "Wise" in a different field (say, an education platform) but that is as designed. It is unfortunate that large corporations overzealously "defend" their trademarks against all usage of the trademark even in unrelated fields, that is abuse of the process and not how the law was intended to work, they basically drown you with lawyer fees.

This feels like an incredibly ill-advised rebrand. Everyone I know of who uses TransferWise uses it rarely, like once per year. They won't be slowly eased into the new name. They'll try using the service again for the first time in a while, and everything will have changed to look like a phishing scam. And this is a service where that trust is critical, since the interaction model of the service is so odd. I'm transferring a 5 figure amount of money to a middleman, and hoping to get 99% of it back in a few days. That requires a bit of a leap of faith.

The only way this makes sense is if they're intending to sunset the transfers in a couple of years, and are all in on their "we're not calling it a bank account, so who knows if we're actually regulated like a bank" product.

Funnily enough it costs more in fees for me to use Wise as my daily account so I've kept my traditional bank cards! I do suspect it varies by country. I'm fortunate in New Zealand that banks generally offer fee-free accounts with reasonable terms and conditions.

- daily spending on goods and services

- electronic transfers to ewallets*

- any time someone needs to send me money, I use transferwise virtual account details so from their end it seems like a domestic transfer

- I even bought a motorcycle using Transferwise to do a local bank transfer. Tried it with my regular (foreign) bank first and it failed, tried it with Transferwise and it worked fine.

*my traditional bank doesn't support this. They only know how to deposit to a domestic ewallet, Transferwise can do deposits in ewallets internationally

I use it as my primary spending debit card. I travel a lot, use it in random ATMs and I keep it topped up just enough that I wouldn't be devastated if the account contents were stolen. Also use the money transfer side monthly to pay rent in a foreign country.

I'm sure they will keep transferwise.com and have a big announcement on there showing to tell people about the new name. I don't think that will look too suspicious. Sure, it might give you a moment's pause, but it will be pretty clear that it's legit. Plus, I'm guessing they will send an email or two about it as well.

We use it multiple times a month and seemingly the people that want to be paid this way from us seem very familiar with it. Not sure which of our anecdotes are closer to the actual truth.

Use it monthly. Have salary from foreign country, and simply keep a bank account there, then transfer it to US with (Transfer)Wise. Rebrand won't matter, as I guess I would always Google "Transfer Wise" either way, if nothing comes up for the query "Wise".

They're big win going forward is their business banking product rather than personal banking offering.

Businesses opening accounts with TW get real bank account details, that work in the traditional banking system, for each currency with little hassle, and good exchange rates to boot.

I think it depends,I was transferring for a year my money overseas and then yes rarely used it. I would think they want to capture the people that send money from high income countries to lower income and freelancers. Those are probably the core customers

Big fan of TransferWise, been using them for years as they're the only FX provider I've used who are actually transparent about their fees which are derived from the real-time actual market rate at time of submitting the transfer - which end up being substantially lower (and much faster to deliver) than any other FX service I used to use.

I get why they'd want a rebrand to "wise", similar to "Apple Computer" -> "Apple" when Apple started doing than just computers but IMO it's a bit early as they're still only known for their core Transferring funds services. At the same time having a short company name & domain like `wise.com` does give the impression of a more global trusted brand for anyone who's never heard of them - so I'd say it's a good move for them overall.

“Apple Computer” wasn’t how anyone referred to the company, basically ever. Nobody calls it “Apple Inc.” today (outside of legal stuff, of course). But I doubt anyone called the fintech “Wise” before the rebrand.

I might be one of the rare people who loves Transferwise? I've used them for 5 years, to transfer money from multiple businesses, and personally. I've sent money between businesses, to people internationally, paid for office rent, developers, heck I've done transfers to myself between countries with it.

I ran into KYC, which is only fair. They required proof of funds which included a letter from my accountant. They assigned a named case worker with a phone number, who I could call. 10/10 would do - and have done again, as recently as two weeks ago. I love this company.

I also loves it and I've been using it for 5 years. I regularly transfer money internationally and it works in 24-48 hours for a few dollars per transfer

I used the service for two years and just had the most surreal disastrous experience since the year flipped. I religiously send a the same (about 5k USD) to my home country every month so I can pay my mortgage and other bills I left when moved to NA.

2021 arrives, I start a transfer on January 27, days pass, nothing. I contact support 10 days later (of something that in the past 24 months took 3 days), they say I need to prove I’m the recipient so I ask them to cancel the transfer so I can start it from my personal account instead so both accounts match and no documentation is needed, another 10 days go by, still nothing.

I contact support again and found out that they withheld my deposit because they needed me to give, bear with me, POWER OF ATTORNEY among tons of other more resonable documentation to the destination country bank, so instead of signing my life away I cancel the transfer again: 26 days an counting TransferWise held my money which I will NEVER deal with again and tell this tale whenever I get a chance.

Unfortunately I have come to believe there is no banking service that won't do things like this at some point. For example, I used to swear by N26 until I had a small issue (involving some tiny amount <€50). I told support very politely that I wasn't happy. Their response was full nuclear "pay everything immediately or we're sending your details to a collection agency". I was amazed, I had been a loyal customer for years and this was such a disproportionate response to something tiny. I had been intending to try and work things out,but from that response I simply withdrew all the money from my account and closed it. Now I use Transferwise, and have had no such problems, so far. But I'm under no illusions that I won't have problems in the future.

I would regular have to ask for status updates; email the managing directors and only then would things get progressed.

My issue stemmed from May 2019 right until Mar 2020; when he stopped responding (and according to linkedin, left the firm).

Basically, every support interaction required multiple pulling of teeth. That should not be how a bank interacts with you, especially when they have your money.

I now use another bank in Berlin, just a normal one, and the interactions are about average ( I ask a question; they take a week to get back to me -- but they *tell* me it will take a week).

> are you trying to imply he should continue responding to you after leaving the job?

No, I believe the parent is trying to tell us that they checked the employee's LinkedIn and noticed that the employee had changed jobs, so they arrived at a reasonable assumption: the employee may have stopped responding to their requests because he changed jobs.

In the UK we have the Financial Conduct Authority. For a registered financial institution you have protection of, I think, something like £80,000 in case the bank goes bust and you can also ask them to investigate any complaint.

I have done this once for my own account and a couple of times for others. They really do look into every detail and will award compensation if it's clear the bank was at fault.

Institutions that don't have this protection include Trasferwise and Revolut, both of which I have had issues with in the past.

Same with Klarna or Revolut. I've come to the conclusion that Zawinski's Law for Fintechs goes like: Every Fintechs attempts to expand until it adds customer support.

5k per month is 60k per year. A typical developer makes at least 100k per year in the US; but if you are only support yourself then you can easily live on 40k per year outside of SV and a few other high-rent areas. The math checks out. And sending 60% of your salary back home is something that plenty of people do.

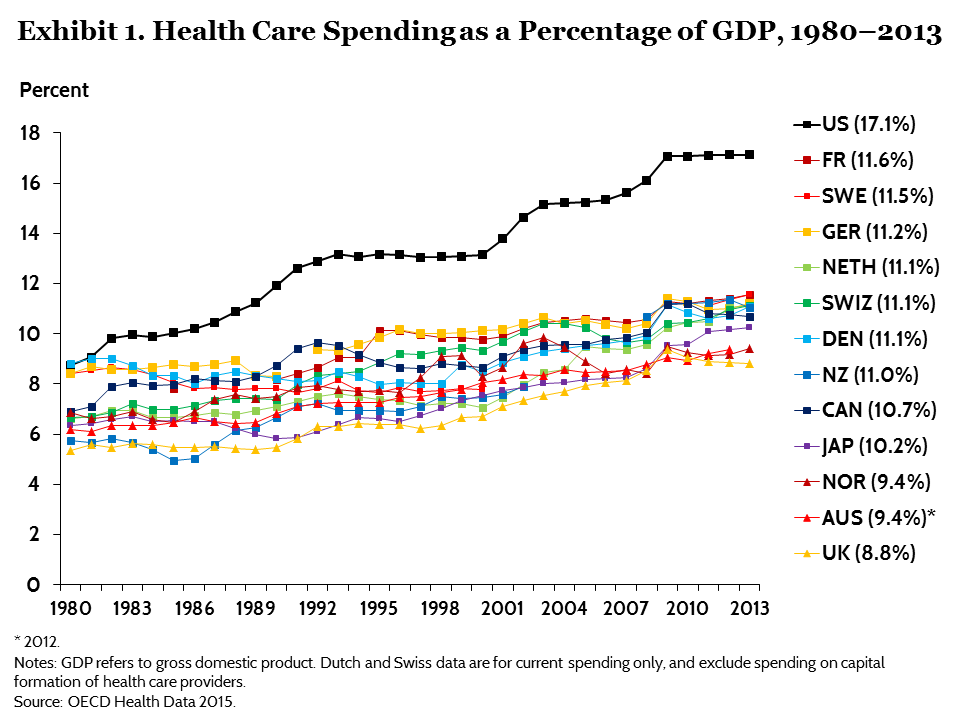

It seems that US citizens already pay more than a typical european country with free health care [1]. So they just getting billed from something they already payed for and they are indoctrinated to think that this is normal.

I actually did compare the retirement/disability payouts to one European country at one point (a Scandinavian country - Norway I think) and the US was comparable. Shocking I know. Sure the US doesn’t have the same extent of programs, but acting like US has nothing is just fake news.

And no, the education doesn’t cost $40k (that was my point) and the higher salary easily offsets the loans for a lot of careers.

And no, there are plenty of good paying jobs in the US, not just tech (I’m not in tech).

I think it pretty much evens out for the average person - not a tech high earner but not someone living on benefits either.

In Europe the average salary is 1695 Euros (2050 USD) a month, while in America it is 2136 Euros (2594 USD).

In Europe we have free healthcare and mostly free* education. So on paper it evens out on the long run.

But in Europe we have diverse countries - the top tier are having it better than the US, while the bottom tier are having it much worse.

For example, Bulgarians earn an average salary of a measly 550 Euros (667 USD).

Yeah, when your government doesn’t take money from your pocket to pay for and give you "free" stuff, you end up with more you can then decide to spend as you need. Who would’ve thought?!

I know it's hard to imagine this if you've never experienced it, but be a little tolerable to the parts of the world where this happens, including where I'm leaving in right now

I actually live in the EU, and I lived in a communist country before so I have enough experience with your "dream". Sooner or later it turns into a nightmare.

As Margaret Thatcher said, the problem with socialism is that eventually you run out of other people's money.

It’s indeed a hard point to get across when you’ve been indoctrinated (we all are about something) that leaving it to the government is a better option. For example, people in Europe obsess about retirement plans, but rarely consider the possibility for creating their own private future financial plan.

Yeah, I have one of those (compulsory) retirement plans. Even if it's tax-free, its yield is incredibly crappy compared to my own (very conservative) investments in broad index ETFs.

I would gladly put ALL my savings into my own retirement plan instead of the government's money hole if I was allowed. But I am robbed of that choice...

Because some people just can't. It's nice and easy when we are closed in our tech bubble, but it's not so good for everyone else.

I'll gladly pay my taxes knowing that the current retired people that didn't have the possibility to save up, can survive today. Also hoping that happens to me in case a horrible thing happens to my financial situation.

It’s not an all or nothing question, I just highlighted where the thinking tends to go towards here in Europe. Not saying eliminate retirement plans, but also take into account your financial future if you can. Have that as a goal.

After experiencing both thought systems as an outsider (I'm neither European nor American) it feels like American system wants to win life and European system wants to live life. I honestly do not want to create my own financial future plans. I find investing and dealing with my own money incredibly stressful and distracting. I do not care for investing nor do I want to care. I want a guarantee that I will have a minimum lifestyle and the time saved can be used to enjoy right now.

People like me, who take stress when it comes to such things, love European system but people who find it trivial to invest in markets and such find the American system better. I wonder how many people think like me and how many like Americans. I have met Americans who don't think like what I just categorized as the American mindset, and European which are opposite to. So I really cant just take the populations and answer my own question.

Well, that's almost enough to match the median household income in the US ($68k) so you probably don't want to extrapolate too far from what they make.

You’d be surprised how rich a society can be with a high IQ demographics, low taxes (I.e. barriers), and free enterprise. In Europe, landlocked no-oil Switzerland is a good example of this.

The average IQ in the U.S.A and the E.U is roughly the same[1][2]. The tax rate is also very similar [3]. Salaries can also vary a lot. If a tech worker in SF can have a salary that dwarf most of its EU colleague, a minimum-wage worker is often going to have a better salary and benefit in the E.U (although it vary a lot per-country basis and the same can be said with states in the U.S.A).

If I didn’t include the intelligence caveat, one could point out lower tax countries with less opportunity, such as how Somalia is the anarcho capitalists dream. Even if the US and Switzerland are more economically free than many other more socialist western nations, intelligent demographics is makes or breaks that effect.

The average American also makes more than the average European - not only in SF. In more economically free European countries this is not the case though, but these are few. Except for the highly regulated (thus inefficient) American Heath insurance market, having a regular job is a better deal there.

The things you mentioned aren't what make Switzerland a rich society.

In my experience living here, it is the strong social security net (70% of your previous wage if unemployed), high minimum wage (up to 25$/hr in some areas), and general workers rights/protections.

None of those are unique to Switzerland but it’s a lot richer than any of its neighbors. The policies you describe don’t cause wealth. They’re things you can afford once you’re wealthy. If Kerala adopted those policies they’d either be widely flouted outside the formal sector (at best) or destroy the economy.

"some areas" is doing a lot of heavy lifting in this sentence of yours. First of all, there is no Federal minimum wage, it is Cantonal. Second of all, the minimum wage of 20CHF only exists in 2 Cantons: Jura and Neuchatel. Third of all, once you PPP adjust that number, it's equivalent to about $10 USD/hour.

Switzerland has the unique advantage of having staid neutral since somewhat 500 years which means their wealth never got plundered or destroyed in one of the way too many wars that have plagued Europe since then. Their neutrality status, combined with a long tradition of utmost banking secrecy, also made Switzerland a perfect "safe harbor" for lots of foreign dark money of all kinds - from kingdoms, warlords and other dictatorships to seemingly "non-profit" corrupt entities such as FIFA, not to mention ordinary European rich wanting to hide their money from the taxman.

tl;dr: Switzerland got rich because of staying neutral and not asking questions about where incoming money originates from, not because of "free enterprise".

By that reason my nation the Swedes should be as rich as the Swiss, or more, since we have minerals and export a lot of wood. Sweden too has been neutral for hundreds of years. The demographics (of native Swedes) are similar in intelligence, a highly inheritable trait, as the Swiss, so that is not the differentiation.

But instead Sweden chose the way of high tax on high income, high capital gains tax (which is zero in Switzerland), and a big “public sector” in order to make a large section of the people dependent on the state. The effect is fewer rich people who can invest in new companies, and more investment done via the state, which is inherently less efficient

Swiss neutrality post dates Napoleon’s fall. It’s barely 200 years old, not 500. And Switzerland would be rich without banking. It wasn’t (much) richer than its neighbors before WW2. Not getting bombed into rubble and banking secrecy gold are great but S Korea, Taiwan, Singapore and Hong Kong show there’s more than one way for a well governed country to get rich, starting from poverty.

I compare CH to Norway - 0.19% wealth tax in Zürich vs 1.8% in Norway, 0% capital gains tax in CH vs 20% in NO, 8% VAT in Zürich vs 25% in NO, zero natural resources in CH, massive amounts of oil in NO. After that, there is a manyfold greater chance for someone in CH to make a better wage and to save up a million $. Economic freedom is lifting the tide on which all boats sail.

Valid point, but Spain is also neutral but isn't exactly bursting at the seams with pots of gold.

They used to be the wealthiest out there, but I guess they took a few bad turns.

Just saying staying neutral doesn't automatically make a country (stay) wealthy.

Singapore also does not have a capital gains tax and much more than other countries respects the natural right to ownership. If you with force go against the natural right to life, liberty, and property, you are punished with inefficiency.

Not quite so severe but I had a problem logging in which resulted in my account being frozen until I could prove my identity. This was a simple matter of providing a selfie whilst holding a photo ID.

Every attempt resulted in a message that the image wasn't clear enough. The delays bewteen messages were also days and weeks apart. Eventually I gave up and I no longer have access to the account. Thankfully, there was no money it.

As someone that had a similar experience with Transferwise (actually also a 5k transfer), I'll give you a piece of advice: sue them.

In the US, you can file a small claims easily and without a lawyer. Some jurisdictions will even let you file 100% online, and the filing fees are very low.

After 2 months of Transferwises' excuses, they wired the full amount + legal fees to my account within a few hours of them receiving the notice.

A relative of mine recently had their account permanently terminated for attempting to do a low six figures transfer. They had been a customer for at least a year and frequently used their TransferWise debit card during that period.

That pain is so huge I just can't forget it. I am a Canadian resident , a dual Canadian-Hungarian citizen, my brother has accounts in Austria and Hungary, my clients are in the USA chiefly but also all over the EU. So international wires are quite a thing.

Here in Canada, the traditional way I could send money was going to a bank branch , fill out a very long form to be able to do a SWIFT transfer and pay through the nose for it.

Then came VBCE online, an FX company which was OK-ish except you needed to ask them to add everyone wiring you beforehands. And they demanded to have an up to date passport on file.

Then came transferwise and the world turned into a happy place.

Many Canadian banks allow sending wire transfers online. For instance, with RBC you can send up to CAD 10K equivalent online for a CAD 15-20 fee. The UI is rather simple and they even have 2FA for transfers. RBC also has the more advanced RBC Express for online banking but I don't know much about it.

However, it's still worse than TransferWise. If a wire transfer is sent via RBC online, the actual amount received by the recipient is frequently $25-27 less which is supposedly due to some random routing fee (it's not possible to specify an intermediary bank in RBC online). As a result, the total cost of a wire transfer ends up being CAD 45-50. In TransferWise a wire transfer costs C$6 to send and the received amount is always the same as the sent. The UI is simple, and the support is helpful (never had problems with them).

I just looked into the (relatively) new CIBC Global Money Transfer and it quotes me 4313 CAD for the other end to receive 1 000 000 HUF while TransferWise quotes 4298.23, a tiny 0.34% difference. However, TransferWise still has the huge, huge advantage of not sending a SWIFT transfer in a lot of countries -- this is the fee you mentioned, the recipient can be charged for receiving a SWIFT wire and you can't know ahead of the time -- when sending a proper wire from the branch you can volunteer as tribute erm accept those charges but the Global Money Transfer doesn't allow for this AFAIK. TransferWise uses local giro wherever they can. It also makes for a smoother experience, I just looked into it and quite a few forums are full of complaints -- SWIFT is old and finicky, no doubt at that. They also offer accounts connected to various giros as well , so you can have a HUF account, a SEPA enabled EU account and so forth.

I'm very happy with TransferWise' low fees, but their 'borderless' account is unfortunately no substitute for a real account in the native currency in a lot of cases.

I'm not sure whether their fees are really that low. For transfers between your own accounts, for anything over very small amounts, I found that their 0.35% variable fee is pretty large compared to adding the funds to a brokerage account and then doing the conversion there (ie. IB charges 0.002% on currency trades, with a min of $2), and transferring back out into the desired currency.

Well, for starters most transfers I and my friends have had to make are not to our own accounts. There's also the time issue - I have an IB account, and love it, but most of the time I'm using Transferwise because I'm in a different country and paying someone, or because I need to move money between my own accounts quickly. Transferwise is literally instant for about half the transfers they do, which is incredible. Meanwhile with IBKR I'm usually out at least three business days for any USD funds to show up in IBKR, plus whatever time to wait on the foreign currency side. Then there's also the UI - sometimes I need someone else to transfer the money, or IBKR's login system is locking me out, etc etc, and in those cases Transferwise always wins. Or if I'm transferring under 25k and I need to do it outside of market hours - in that case my transaction is an odd lot at IBKR, getting me (oftentimes) bad rates, and I might as well use Transferwise.

Don't get me wrong, I like IBKR and I do use it, but Transferwise is definitely more useful 90% of the time.

Yeah, you're definitely paying a premium for them handling smaller quantities, end-to-end, in one easy tool. IBKR requires knowledge of Forex trading, but is hands down the cheapest and fastest solution - for those that are able to work it. To be fair, that describes basically all of IBKR.

It's still mind-blowing to think IBKR charges $20 per million, when the airport Travelex will charge you $20 per hundred lol.

Could you explain how this works, or point me in the right direction on what to read? I'm interested in not using Transferwise as much if this is better.

You'd open up a trading account, deposit funds from one country to it (generally free in EU/UK, can be done with a simple bank transfer, though can take 1-3 business days). Rather than the common use case of a brokerage account to buy stocks/invest, you place an order into their IdealPro order book they run to buy the currency you want (might have to jump through 2 trades, they don't run every single pair). Generally this is tailored at larger investors, so anything under $25k is subject to some additional fees due to being a small size (https://ibkr.info/node/1459), but still significantly less than the 0.35% TransferWise charges. The costs for you are commission (<0.2bps), potentially small size fee (1-2 bps), and crossing the bid/ask spread, which is ~0 for currencies). When that order has been filled you now have the desired currency in your account and you can transfer it back out (potentially to a different country or different account).

It's a free/cheap multi currency account with local bank details in 6+ countries, which give you 90% of the functionality you want, namely the ability to hold and transfer cash.

If you need more functionality you get a local bank account.

> The deal breaker for me is the fee for bank transfers, something I've never paid for before.

You are too young :-).

This also might change. German banks start again to take monthly fees for accounts, so why not for single transactions.

This said, I have to deal with accounts in NZ and Europe. Fees as well as speed for transfers between them is a whole other world when using TW compared to classic banking. These kind of costs have exist forever, SEPA conditions are the exception, not the rule, internationally.

TransferWises multi-currency account is a nice part of the package. I learned here today, this can be done even cheaper by using a Forex broker like IB, but I don't need this on a daily basis.

I guess this is something that might have changed - but I definitely recall being charged for making transfers from Poland to the UK, and same very recently for Switzerland <-> UK transfers. In both, rather insidiously, the outgoing bank cannot tell me what the final fee will be, and I only find out what was charged when less money appears in the recipient account than what I sent.

EU / Switzerland, so I've never experienced this. I thought it was due to SEPA preventing such fees, but that doesn't seem to be the case if I read this section correctly: https://en.wikipedia.org/wiki/Single_Euro_Payments_Area#Char.... I guess healthy competition just killed these fees.

I apparently have to pay €0.28 per transfer in EUR with Transferwise. There are competitors (both in CHF and in EUR) that do this for free. I do something like 8 transfers per month, so that's 8*0.28*12 = €26.88 per year, for no added value. Not convincing.

Often getting an account in another country is a big hurdle - TW makes this incredibly easy.

e.g. I'm opening an account in France at the moment (as a French resident!) and it is taking literal weeks and lots of scanning documents, posting paperwork, phone calls etc. TW opened a Euro account for me in a few clicks.

One in the US is that you cannot use a borderless account for ACH transactions initiated by the counterparty (despite it presenting the details that make it look like you can).

I'm curious to know how you verified this. The help text in the app is explicit that "There's no fee to receive ACH payments, or any other kind of payment that uses your ACH routing number."

I remember the app used to show two sets of US bank details, and that the routing number for receiving wire transfers was different from the one used for receiving ACH transfers. But that seems no longer to be the case.

If you're saying that people can't transfer money into your account via ACH, then that's not true. Being paid by a client is a specific use they describe.

The opposite is what I am describing. I.e I cannot (read: could not last time I tried it, about 2 years ago) pay rent using TransferWise, upon entering the routing code and account number.

"Horror" stories abound in this thread (of course, all is relative; first world problems; etc).

My view is mostly that customer service is broken. Everywhere. A few days ago I wrote and published a "corporate memo" where I make the case that a company such as Stripe could tackle this problem and solve it [0].

I really hope that someone will eventually find a way to provide proper customer service, without resorting to these terrible practices when something gets weird.

I'm not sure if you're directing this comment at TransferWise or at companies in general, but I'll reply from TransferWise's point of view - Disclaimer, I'm an engineer at TransferWise, but this is my own opinion.

TransferWise takes customer support extremely seriously with an in-house team of support reps who are trained in all of our features. On top of that each team may have one or more CS "champions" who are the bridge between product teams and customer support. These champions usually know the product inside-out, and are in slack channels with the dev teams.

So when an issue is not a customer misunderstanding something, and turns out to be an actual bug, the CS rep will work with the engineers to find a workaround, and to get a fix deployed as fast as possible - all while the customer knows exactly what's going on.

Bottomline is that I agree that customer support is hard, and very expensive. But it doesn't have to be broken, and I don't think it is at TransferWise (well, Wise now)

It's interesting to see your take on how things work however from reading around it would appear that Wise is pretty trigger happy to terminate accounts and almost anti crypto.

I applied last year to use their services for my officially registered company based in Canada. They didn’t approve it, and when I asked for the reason, they said it is their algorithms. It was not wise thing to do.

I got married abroad and that often implies needing a service like TransferWise. When I first got married, I actually thought I’d need to use hsbc (who sort of support online wire transfers) but thanks to TransferWise, I’ve never once had to send a wire transfer. TransferWise sends money more quickly to my wife than I can send between my own bank accounts in USA. Very reasonable (but sometimes random) KYC (make sure to maintain your drivers license at a permanent address where you can receive mail in your home country).

I really wish them all the best with the new brand and am excited for the new products! Even when I’m just being a tourist, the debit card and borderless card make working in different currencies a breeze.

My only wish is that the debit card issued to us citizens didn’t default to dollar payments but could intelligently mark itself as the local currency. Remember that when a foreign terminal tries to bill you in USD, the bank the card reader is connected to makes profit from marking up exchange rates.

The reason I am NOT USING TransferWise is that I encountered something strange.

To obtain their debit card, one of the requirements is that I add money to my account. So far so good. When I am on that page where I can enter the amount I want to add, there is always a minimum amount given. This is not in itself a problem. The problem is that - to my surprise - this varies by a LOT, and I have no clue why. Sometimes it is 5 USD, sometimes it is 20 USD. As in, sometimes I can add 5 USD or above, but not less, and sometimes I can only add 20 USD or above, but not less.

By now I went through[1]: 5 USD -> 20 USD -> 1 USD -> 5 USD. Why does this happen?

I do not know the actual values as I was using another currency, but you get the point.

[1] I kept checking only for 2 days, so those values were changing this way within those 48 hours max.

Yeah, it confused the heck out of me, and made me reluctant to use it, because who knows what else they may change. The differences were huge in my currency. :/

I checked just now, it is back to the initial value, the value that I encountered first.

I use transferwise as my main bank. The one thing I need from them now is the possibility to invest my borderless account funds in ETF or other guaranteed capital investment vehicles. I hope this rebrand means they are heading in that direction.

I've literally asked for this in every user satisfaction survey they've sent me for the last 5 years, and like you I hope this is a sign they're heading in this direction.

The competition in this space is large, but there are a ton of trade offs between various services and in many countries (hungary, for one) the local alternatives simply suck.

Apologies, but let me put on my cynical hat for a moment to make a joke.

Nothing could be more representative of modernity than the fact that typing wise into your browser bar will now direct you to a financial services company.

Can someone answer how TransferWise gets away without "reporting this information to HMRC or any other tax authority." aka dream for tax evaders (who get paid in foreign currency)?

Your linked Austrac page refers to cash transactions ("physical currency"). This one[0] however, says that any international funds transfer instruction (of any amount) needs to be reported.

Most likely because they pass that buck to their local partners.

In South Africa for example, they've been partnered with exchange4free (dodgy name but legit) but recently changed to Bidvest. If TW isn't reporting, these third parties are. You have to sign mandate forms once a year explicitly for reporting purposes.

I've had good experience with TWise, sending money can be such a pain. WU was okay but after you exceed some amount start to get blocked/have to prove identity etc... I'm not rich/not sending massive amounts but was still getting flagged early on. TW is working pretty well so far, so is WU after I sent some docs. I tried a few other companies too but yeah settled on TW/WU.

We use it for business regularly and repeat transfers become faster over time. We had freelancers (EUR->GBP) receive their money in 2 days, after a while it was down to hours and we even saw 1 hour transfers. The limit became the receiving back making the funds available to the bank account owner.

I find it interesting that companies often rebrand themselves to a generic word. Would Microsoft, for example gain anything by calling themselves "Micro" or "Soft"?

I also wonder if they tried to rebrand to "Transfer" as that would at least describe themselves and give them some interesting opportunities, e.g. money.transfer, coin.transfer

Hope they stop sending my data to Facebook. I am their customer for a little over an year now and I was very disapointed to find out they send a lot of stuff to Facebook (https://www.facebook.com/off_facebook_activity/).

Someone didn't do their trademark research. Out on the east coast US (like NYC metro) anyone hearing the name Wise isn't going to think 'transfer service', they are going to think potato chips: https://www.wisesnacks.com

I see this like Delta Faucets and Delta Airlines. I've never had any trouble thinking of one when I meant the other, and I suspect the same is true here.

Would it be safe to use this if you're transferring a very large amount of money, for example to buy a house in a foreign country? Anyone have experiences (good or bad) with large transfers they'd like to share?

I have used it to pay a large foreign tax bill, so not quite a house. If the amount is GBP£30000 (might have changed now), you can arrange a longer pay-in time (normally it is 24 hours) and they will let you have the cash sit in your account for up to a week and then find the right rate.

+1 of OFX. I use TransferWise a lot for cross border treasury management, but used OFX when moving $large_sum USD->EUR to buy a flat in the EU because they offered a better conversion rate.

They are not covered by any kind of FDIC equivalent (and in fairness there's not really any good deposit insurance regime for international accounts). They claim to use ringfenced accounts for customer funds but AIUI that's all self-certified (and wasn't there at all when they first started, although I understand they've gotten a bit more professional in various ways). I wouldn't worry too much about making a one-off transfer under normal circumstances - the risk of them going bankrupt in the next week is pretty low - but I'd be a little wary of keeping a substantial balance with them over the long term.

I wish they had the capability to issue virtual card numbers. I don't even need temporary ones, just want the capability to segregate my spending into separate accounts.

Virtual Cards can help you pinpoint which of your service providers got hacked, plus minimise the amount of OTHER services you need to update payment details for, after a card number going AWOL

Although the rebranding is probably unnecessary, it is still a good move if the company has ambition beyond fund transfer --- perhaps into alternative financial services, non-bank assets, or other types of nomadic fund application. I have to agree there are too many geographical restrictions in today's financial systems, and if their strong brand position can help to loosen those grips a little, more power to them.

I just wish they would not inherit the horrible security practices from the incumbents.

Opening a new account, the happy path steers the user to 2FA via SMS (which can't be disabled once enabled). The only other option is via their proprietary iOS or Android app.

Please, please give us at least TOTP, if not FIDO U2F or Webauthn.

SMS is inherently insecure (arguably worse than e-mail) and I'm not going to download your app.

For the kind of service they provide, transfer.com would have been better. (Of course if it all it was possible)

Nonetheless, not a bad idea, as companies grow they all want the shortest possible brandable .com domain. I remember seomoz.com rebranded to moz.com for few million $$.

Ironically not wise. I think Seth Godin will not be pleased. This is against niche philosophy - I was good at something then I wanted to do everything - then I went bankrupt. I like TransferWise but this is ridiculous move.

I was trying to figure out a way to move my GBP from my US based paypal account through TransferWise to avoid the Paypal FX rate, but couldn't figure out how...

{kind=link}

{kind=link}